What Is DSCR In Real Estate And Why It Matters For Investors

Discover what is DSCR in real estate, how to calculate it, and why this crucial metric determines your investment property financing and profitability.

If you've ever looked into financing an investment property, you've probably heard the term DSCR. But what exactly is it?

Think of the Debt Service Coverage Ratio (DSCR) as a financial stress test for a property. It's a straightforward metric that answers one critical question for both you and your lender: does this property make enough money to pay its own mortgage?

It’s the first thing a bank looks at to gauge whether an investment is a solid bet or a potential money pit.

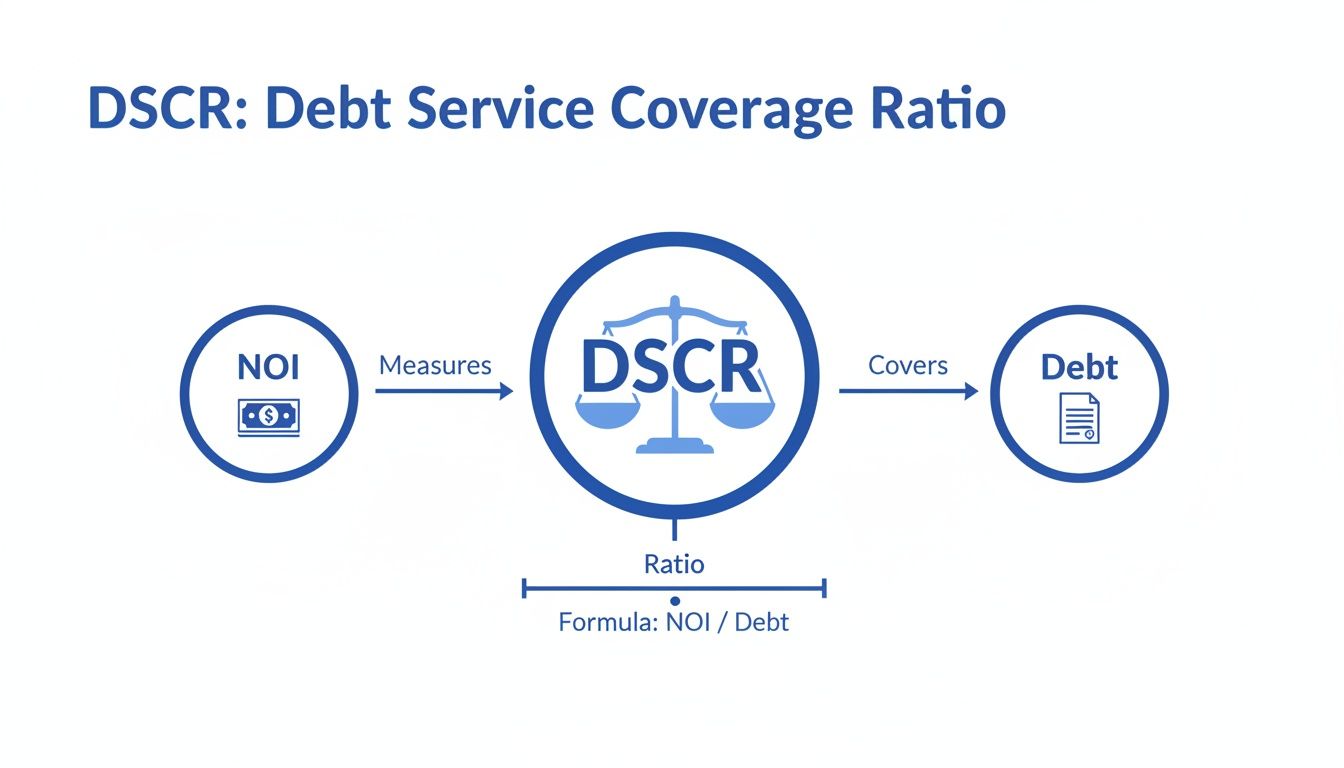

What Is The DSCR Formula And Why Does It Matter?

At its core, DSCR is a simple ratio that compares a property's income to its debt payments. A DSCR greater than 1.0 means the property is generating enough income to cover the mortgage. Anything less than 1.0 is a major red flag, signaling that you'd have to dip into your own pocket just to keep the lights on.

But here’s the thing: just breaking even isn’t good enough for most lenders. They want to see a safety buffer.

Most banks and lenders for commercial loans for investment property will require a DSCR of at least 1.20 or 1.25. This "magic number" gives them confidence that the property has a 20-25% cash flow cushion to handle unexpected vacancies, surprise repairs, or other bumps in the road without missing a loan payment.

The formula itself is simple, built on two key numbers from your property analysis:

- Net Operating Income (NOI): This is all your rental income minus all your operating expenses (think property taxes, insurance, maintenance, management fees). Critically, NOI does not include your mortgage payment.

- Total Debt Service: This is the total of all principal and interest payments you'll make on the loan over the course of one year.

As the diagram shows, your NOI is the engine that has to power the debt payments. The DSCR simply measures how much bigger that engine is compared to the load it has to carry. Getting these numbers right is a fundamental part of any solid real estate investment property analysis.

DSCR At A Glance: What The Numbers Mean

To make it even clearer, let's break down what different DSCR values really signal to everyone involved in a deal.

| DSCR Value | Meaning | Lender's Perspective |

|---|---|---|

| Below 1.0 | Negative Cash Flow. The property doesn't earn enough to cover its mortgage payment. | Extremely High Risk. Loan application will almost certainly be rejected. |

| Exactly 1.0 | Break-Even Point. Income is just enough to cover the debt, with zero room for error. | Very High Risk. Still too risky. A single unexpected expense leads to default. |

| 1.01 - 1.19 | Minimal Positive Cash Flow. The property is technically profitable, but the margin is razor-thin. | High Risk. Most lenders will pass. Not enough cushion for vacancies or repairs. |

| 1.20 - 1.25 | Acceptable Cushion. The property generates a healthy buffer above its debt obligations. | Meets Minimum Requirement. This is the sweet spot and the typical minimum for most lenders. |

| Above 1.25 | Strong Positive Cash Flow. The property is a strong performer with a significant safety margin. | Low Risk. This is a strong, desirable deal. You may even qualify for better loan terms. |

Ultimately, the higher the DSCR, the healthier the investment and the more attractive it becomes to a lender. A strong DSCR doesn't just get you approved; it demonstrates that your deal is built to last.

Calculating DSCR Step By Step With Real Examples

Knowing the formula for the Debt Service Coverage Ratio is one thing, but running the numbers on a real deal is when the lightbulb really goes on. The math itself isn't complicated; it boils down to just two key figures that tell you everything you need to know about a property's financial health.

Let's walk through the process before jumping into some examples.

First, you need to figure out your Net Operating Income (NOI). Think of this as your property's total annual profit before you pay the mortgage. You get there by taking all your income (mostly rent) and subtracting all the costs of running the place—things like property taxes, insurance, maintenance, and management fees. The key here is that NOI does not include the mortgage payment.

Next, you need your Total Debt Service. This one is simple: it's the grand total of all your mortgage principal and interest payments for the entire year. Just take your monthly mortgage payment and multiply it by 12.

Once you have those two numbers, the formula is a piece of cake:

DSCR = Net Operating Income (NOI) / Total Debt Service

This little ratio is a cornerstone of real estate investing and a critical part of how lenders see your deal. It's just one of many financial metrics, and if you want to go deeper, it's worth understanding the principles of ratio analysis more broadly.

Example 1: Single-Family Rental

Let's get practical and run the numbers on a classic single-family rental. Imagine you've found a solid house in a decent neighborhood.

- Annual Gross Rental Income: $2,400/month x 12 = $28,800

- Annual Operating Expenses: (Taxes, insurance, maintenance, etc.) = $9,200

- Annual Mortgage Payment: $1,400/month x 12 = $16,800

Here’s how we plug it all in:

- Calculate NOI: $28,800 (Income) - $9,200 (Expenses) = $19,600

- Find Total Debt Service: Your annual mortgage cost is $16,800.

- Calculate DSCR: $19,600 (NOI) / $16,800 (Debt Service) = 1.17 DSCR

A DSCR of 1.17 means the property’s income covers its debt payments 1.17 times over, leaving a 17% cushion. While it's profitable, most lenders want to see a minimum of 1.25. So, this deal might be a bit too tight for them without some changes.

Example 2: Duplex Investment

Now, let's see what happens with a small multifamily property, like a duplex. With two streams of rent, the income side of the equation looks a lot stronger.

- Annual Gross Rental Income: ($1,600/unit x 2 units) x 12 = $38,400

- Annual Operating Expenses: (Higher taxes, more maintenance, etc.) = $12,500

- Annual Mortgage Payment: $1,900/month x 12 = $22,800

Let's run the numbers for this one:

- Calculate NOI: $38,400 (Income) - $12,500 (Expenses) = $25,900

- Find Total Debt Service: The annual mortgage here is $22,800.

- Calculate DSCR: $25,900 (NOI) / $22,800 (Debt Service) = 1.14 DSCR

This is a great lesson. Even though the duplex brings in way more money, the bigger mortgage results in an even lower DSCR of 1.14. It's a perfect example of why you can't just guess; you have to run the numbers on every single deal.

By the way, that NOI figure is also the starting point you need to calculate cash flow on a rental property, which is the other make-or-break metric for any investor. These examples prove that assumptions can get you into trouble—only the cold, hard math reveals whether a deal is a winner or a dud.

Why 1.25 Is The Magic Number For Lenders

If you spend any time looking at investment properties, you'll see one number pop up again and again in lender requirements: 1.25 DSCR. This isn't some random figure. It’s the gold standard that, for most banks, separates a deal worth funding from one that’s too risky.

Think of it as a financial safety net. A 1.25 DSCR means the property generates $1.25 in net operating income for every $1.00 it owes in annual mortgage payments. That extra $0.25 isn't just pocket money; it's a 25% cash flow cushion designed to absorb the inevitable bumps in the road that come with owning property.

This buffer is what protects both you and the lender when things don't go exactly as planned. And let's be honest, they rarely do.

- Sudden Vacancies: A tenant moves out with little notice, leaving you with an empty unit for a month or two.

- Unexpected Repairs: The HVAC unit dies in the middle of July, or a plumbing leak appears out of nowhere.

- Rising Expenses: Property taxes go up, or your insurance premium jumps unexpectedly at renewal.

With that 25% cushion, your property's cash flow can handle these temporary hits without putting you in a position where you might miss a mortgage payment. It’s why lenders are so firm on this number. It ensures the property can weather the common 5-10% vacancy rates in the U.S. multifamily market without spiraling toward default. You can find a more detailed breakdown of debt service requirements and see just how central this metric is to their decision-making.

The Rewards Of Exceeding The Minimum

Getting to 1.25 gets your foot in the door, but pushing beyond it is where the real advantages kick in. A higher DSCR sends a clear message to a lender: this deal isn't just viable, it's a rock-solid investment.

A DSCR of 1.50 or higher doesn't just meet the minimum; it screams financial health. This makes your loan application jump to the top of the pile and gives you serious negotiating power.

When you bring a lender a deal with a robust DSCR, you're not just asking for money—you're offering them a low-risk opportunity. This often translates into very real, tangible benefits that can supercharge your returns. Lenders want the safest deals, and a high DSCR puts you in the driver's seat to secure:

- Lower Interest Rates: Less risk for the bank means a better rate for you. A lower rate flows directly to your bottom line, boosting monthly cash flow.

- More Favorable Loan Terms: You might qualify for a smaller down payment or get a longer amortization period, which lowers your monthly payments and lets you keep more capital for your next deal.

- A Faster, Smoother Approval Process: A deal with a strong DSCR is easy for an underwriter to approve. There are fewer questions and less back-and-forth because the numbers speak for themselves.

In the end, a strong DSCR is about much more than just pleasing a lender. It's the foundation for building a resilient, profitable, and scalable real estate portfolio.

How a Strong DSCR Unlocks Better Investment Deals

A solid Debt Service Coverage Ratio isn't just about getting a lender to say "yes." It's the key that unlocks a more profitable and resilient real estate portfolio. While a 1.25 DSCR might be the minimum to get your foot in the door, aiming higher is what separates investors who are just getting by from those who are truly thriving. It’s the difference between just covering your bills and building real, sustainable wealth.

When you see a healthy ratio, say 1.80 or higher, you're looking at incredibly robust cash flow. This isn't just a small surplus; it’s a powerful stream of income you can put to work. You can reinvest it into other properties, build a serious cash reserve for a rainy day, or fund major value-add projects that force your property’s equity to grow.

The Real-World Impact of a Higher DSCR

Let's look at two identical properties. Both have the same debt service of $20,000 per year. The only thing that's different is their Net Operating Income, which completely changes their DSCR and, more importantly, the cash that ends up in your pocket.

| Metric | Property A (Meets Minimum) | Property B (Strong Performer) |

|---|---|---|

| Net Operating Income (NOI) | $25,000 | $36,000 |

| Annual Debt Service | $20,000 | $20,000 |

| DSCR | 1.25 | 1.80 |

| Annual Cash Flow (NOI - Debt) | $5,000 | $16,000 |

The numbers speak for themselves. Property B doesn't just generate a little more cash; it produces over 300% more free cash flow than Property A. That massive difference gives you a huge financial cushion, making your portfolio far more resilient to economic downturns, unexpected vacancies, or a sudden roof replacement. For example, a property with a DSCR of 1.82 has 82% in extra income to absorb shocks—a level of financial security that smart investors chase in major U.S. markets. Discover more insights about DSCR benchmarks on Offermarket.us.

Accessing a Powerful Financing Tool

Beyond just strengthening your portfolio, a high DSCR opens the door to a game-changing financing option: the DSCR loan. This type of non-QM loan has become a go-to for serious investors looking to scale their holdings quickly.

A DSCR loan lets you qualify for a mortgage based on the property's income potential, not your personal W-2 or tax returns. If the property's DSCR is strong enough, the lender sees the deal as self-sustaining.

This is a huge deal for investors for a few key reasons:

- Faster Scaling: You can buy more properties without getting bogged down by your personal debt-to-income ratio.

- Simpler Underwriting: The loan application is all about the deal's numbers, not an invasive deep dive into your personal financial history.

- Closing in an LLC: DSCR loans are built for investors, which means you can purchase properties under a business entity for liability protection from day one.

At the end of the day, when you focus on deals with a strong DSCR, you're doing more than just securing a loan. You're building a portfolio that spits out significant cash, weathers market storms, and gives you access to the kind of financing that can seriously speed up your journey to financial freedom.

Practical Strategies To Improve Your Property's DSCR

So you've found a promising property, run the numbers, and the DSCR is just shy of what a lender wants to see. Don't walk away just yet. Think of the DSCR formula—NOI / Total Debt Service—as a set of levers you can pull. With a few smart adjustments, you can often nudge that ratio into the green and turn a borderline deal into a great investment.

The game plan is simple: either make the property earn more money or make the loan cost you less. Both paths lead to a healthier DSCR that will get your lender excited and put more cash in your pocket.

Boost Your Net Operating Income (NOI)

The most direct way to beef up your DSCR is by increasing the property's Net Operating Income. This isn't just about qualifying for a loan; it's about fundamentally increasing the value and performance of your asset. You can tackle this from two angles.

First, make some value-add improvements that justify higher rents. We're not talking about a full gut job. Strategic upgrades—like modernizing a kitchen with fresh countertops and stainless steel appliances, updating a tired bathroom, or swapping old carpet for durable LVP flooring—can command a much higher rent. That new rent goes straight to your top line.

Second, get creative and add new income streams. Think beyond the monthly rent check. Is there an unused common area perfect for a coin-operated or app-based laundry setup? Could you charge a premium for a few designated parking spots? Even small things, like renting out storage space in a basement, can add hundreds of dollars a month to your income and give your NOI a serious lift.

Key Takeaway: Every dollar you add to your NOI directly strengthens your DSCR. Small, consistent income bumps can have a surprisingly big impact on your ability to get the financing you want.

Reduce Your Total Debt Service

While boosting income is the ideal long-term play, don't forget you can also work on the other side of the equation: your loan payments. Lowering your annual debt service has an immediate, dollar-for-dollar impact on your DSCR.

Negotiating the right financing terms is everything here. The most obvious tactic is to lock in a lower interest rate. Even a quarter-point reduction can save you a significant amount of cash each month, making your debt service much more manageable.

Another powerful move is to increase your down payment. Putting more skin in the game reduces the total amount you need to borrow, which shrinks your monthly payment. It also signals to the lender that you're a serious, lower-risk borrower, which can help you secure better terms overall.

Finally, you can often extend the loan's amortization period. Spreading the loan out over a longer term, say from 20 years to 30 years, will result in smaller monthly payments. While you'll pay more in total interest over the life of the loan, it's a fantastic tool for improving your DSCR and making the deal work right now.

Strategies For Boosting Your Property's DSCR

When you need to get your DSCR over the finish line, it helps to see all your options laid out. The table below compares a few common strategies, showing how they work and what kind of effort they typically require.

| Strategy | How It Improves DSCR | Effort & Capital Needed |

|---|---|---|

| Light Renovations | Increases Gross Rental Income, which boosts NOI. | Medium effort, Moderate capital |

| Add Amenity Income | Adds new revenue streams (laundry, parking), boosting NOI. | Low-to-Medium effort, Low capital |

| Increase Down Payment | Reduces the total loan amount, lowering debt service. | Low effort, High capital |

| Extend Amortization | Spreads payments over a longer period, lowering debt service. | Low effort, No additional capital |

| Secure a Lower Rate | Reduces the interest portion of your payment, lowering debt service. | Medium effort, No additional capital |

Ultimately, a combination of these tactics often works best. A small rent bump from new appliances, paired with a slightly larger down payment, can easily turn a "no" from a lender into a "yes." By understanding these levers, you gain far more control over the viability and profitability of your next real estate deal.

Analyze Deals Instantly With Property Scout 360

Knowing how to calculate the Debt Service Coverage Ratio by hand is crucial for grasping a deal's core mechanics. But let's be honest—when you're sifting through dozens of potential properties, plugging numbers into a spreadsheet gets old fast. It's a major bottleneck that can lead to missed opportunities or, worse, costly mistakes.

This is where a good analysis tool doesn't just help; it completely changes the game.

Instead of spending your time digging for comps and double-checking formulas, platforms like Property Scout 360 do the heavy lifting for you. The software plugs directly into real-time MLS data, calculating DSCR in seconds with accurate, market-based numbers for rent, taxes, and insurance. This pulls you out of the weeds of manual data entry and kills the guesswork.

Model Scenarios On The Fly

The real magic happens when you start playing with the numbers. You can instantly tweak the down payment, adjust the interest rate, or change the loan term and see exactly how it impacts your DSCR, cash flow, and overall return. It’s an interactive way to see all the concepts we’ve talked about come to life, turning theory into something you can actually use.

A clear dashboard gives you a visual snapshot of an investment's financial health.

This makes it incredibly easy to line up multiple deals next to each other and immediately spot the one with the sturdiest financial legs and best profit potential.

When the complex math is handled for you, your job shifts from being a number-cruncher to a strategic decision-maker. You can instantly see if a property will clear a lender's hurdles and if it truly fits your own investment strategy.

This kind of speed is a massive advantage in a hot market where the best deals are gone in a flash. You can vet a property in minutes, not hours. It lets you move quickly and confidently, backed by solid data, to lock down the deals that others miss.

If you're ready to ditch the spreadsheets for good, our guide on getting started with Property Scout 360 walks you through how to put your analysis on autopilot.

Common Questions About DSCR In Real Estate

Once you get the hang of the basic DSCR calculation, you'll inevitably run into more nuanced, real-world questions. Let's dig into a few of the most common ones that come up for investors.

What Is A Good DSCR For A Rental Property?

You’ll hear the number 1.25 thrown around a lot, and for good reason—it’s the typical minimum most lenders require to even consider a loan. All that ratio really tells them is that the property has a 25% cash flow cushion above its mortgage payment.

But is that good? That really depends on your goals.

If you’re hunting for properties that generate strong monthly cash flow and want to qualify for the most favorable loan terms, you should be aiming higher. A DSCR of 1.50 or more sends a powerful signal to lenders that your deal is a low-risk, high-performing asset.

Can I Get A Loan With A DSCR Below 1.25?

It’s tough, but not entirely impossible. Trying to get a conventional loan with a DSCR under that 1.25 threshold is an uphill battle. You might find some niche lenders or private money sources willing to take on the risk, but they'll almost certainly ask for a much larger down payment to protect their position.

Honestly, though, a low DSCR is a flashing red light. It means your property is skating on thin ice, with almost no room to absorb unexpected vacancies or repairs. You'd have to be absolutely certain about your strategy before moving forward.

Key Insight: Even if you're a cash buyer and don't need a loan, you should still run the DSCR. It’s a clean, objective test of the property's financial health and its raw ability to generate profit on its own.

How Do I Estimate DSCR For A Vacant Property?

Great question. With no tenants, you obviously can't use current income. This is where a pro-forma comes into play. You’ll need to create a financial projection using fair market rents from similar, nearby properties.

Just know that a lender won’t simply take your word for it. They'll order their own appraisal, which will always include a detailed rental analysis to confirm your numbers are realistic for the local market.

Stop drowning in spreadsheets. Property Scout 360 automates your deal analysis, calculating DSCR, cash flow, and ROI in seconds so you can find profitable deals faster. Discover how it works at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.