Real estate investment property analysis: Quick Guide to Evaluation

Master real estate investment property analysis with actionable steps to evaluate cash flow, ROIs, and risks using real-world examples.

When you're looking at a potential investment property, the analysis is where the rubber meets the road. It's the process of running the numbers to see if a deal actually makes sense—forecasting income, digging into all the expenses, and figuring out what your real return will be.

Getting this right is the difference between building a profitable portfolio and buying a financial headache. It’s all about making a decision based on hard data, not a gut feeling.

Building Your Analysis Foundation

Before you even think about opening a spreadsheet, you need the right mindset. Seasoned investors don't just look at a property; they see a small business. Every potential deal needs to be treated like a standalone enterprise with its own profit and loss statement.

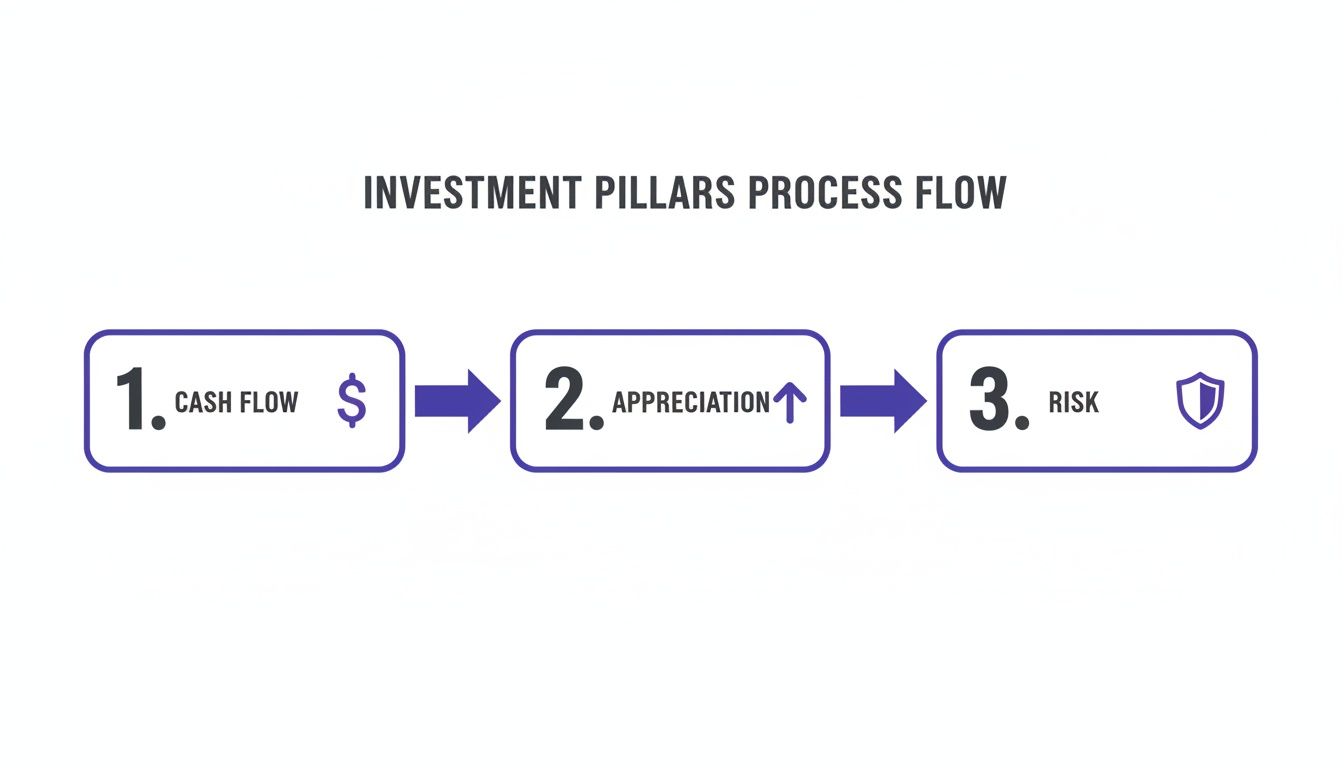

Adopting this business-first approach keeps you focused on what truly matters: the three pillars that hold up any successful real estate investment.

As you can see, a solid deal has to deliver on cash flow, have potential for appreciation, and include a smart plan for managing risk. Neglecting any one of these can turn a promising investment sour.

The Three Pillars Of A Solid Investment

Here's a closer look at what each pillar means in the real world.

Cash Flow: This is the money left in your pocket each month after you’ve collected rent and paid all the bills—mortgage, taxes, insurance, repairs, you name it. Positive cash flow is your immediate profit and your financial cushion for when things go wrong.

Appreciation: This is the long game. Appreciation is how much the property’s value increases over time. It’s driven by the market and less predictable than cash flow, but it's often where real wealth is made.

Risk Management: Every investment has risks. You could get a terrible tenant, face a long vacancy, or suddenly need a new HVAC system. Good analysis means planning for these things by setting aside cash reserves and being brutally honest with your expense estimates.

The goal isn’t to max out one of these pillars at the expense of the others. A high-appreciation property with negative cash flow is a gamble, not an investment. Likewise, a high cash-flow property in a neighborhood that's going downhill is a ticking time bomb.

Finding this balance is more important than ever. As of Q2 2025, global private real estate values have seen five straight quarters of growth. This comeback is driven by more stable property values and solid rental growth, especially in hot sectors like logistics and multifamily housing.

Ultimately, your analysis needs to tell you a clear story about the property's financial future. To get started on the right foot, it helps to understand the foundational things to consider before getting into real estate investing.

A great way to keep your numbers organized is with a purpose-built tool. You can find our top recommendation in this guide to the best real estate investment analysis spreadsheet. This structured approach is what moves you from guessing to strategically building long-term wealth.

Getting the Numbers Right: The Foundation of Any Good Deal

Any real estate analysis is only as good as the numbers you plug into it. If you feed it overly optimistic figures, you’re just building a fantasy, not a solid financial model. This is where the rubber meets the road—we're going to build a checklist for gathering the data that actually drives your returns and keeps your projections firmly planted in reality.

We'll start with the obvious stuff like the purchase price, but then we’ll dig into the nuanced expenses that often catch new investors off guard. Getting these details right is what separates a profitable investment from a financial headache.

Nailing Down Your Income Projections

Your most important number is potential rental income. You absolutely cannot guess here. The goal is to find solid rental "comps"—recently rented properties that are genuinely similar to yours in location, size, and condition.

This takes a bit more effort than a quick search on Zillow. While rental listings give you a starting point, you need to find out what places are actually renting for, not just what landlords are asking. Your best bet is to talk to local property managers or real estate agents. They're on the ground and know the market intimately. To get a more structured look, you can dive into finding free real estate comps to really sharpen your estimates.

Pro Tip: When you're looking at comps, make sure you're comparing apples to apples. A three-bedroom with a two-car garage and a fenced-in yard will pull in more rent than one on the same street without those perks. Adjust your numbers accordingly.

Projecting Your Operating Expenses Accurately

This is where so many new investors stumble. They completely underestimate what it costs to own a rental property, and their cash flow projections pay the price. Operating expenses cover everything needed to run the property, excluding your mortgage.

Here are the costs you absolutely must account for:

- Property Taxes: Never assume the current owner's tax bill will be yours. A sale often triggers a reassessment by the county. Check the local assessor's website, find the correct tax rate, and apply it to your purchase price.

- Property Insurance: Don't just guess. Call an insurance agent and get a real quote for a landlord policy. The cost can swing wildly depending on the property's location (is it in a flood zone?), age, and even the type of construction.

- Vacancy: No property stays rented 100% of the time. It's just not realistic. A conservative vacancy rate is typically 5-8% of your gross annual rent. This basically means you're budgeting for the property to be empty for about one month a year.

- Property Management: Thinking of managing it yourself? Great, but you should still budget for this cost. Professional managers typically charge 8-12% of the monthly rent. Factoring this in makes your analysis more bulletproof and gives you the flexibility to hire help down the road.

Why the 1% Rule for Maintenance Isn't Enough

You’ve probably heard of the "1% Rule" for maintenance—budgeting 1% of the purchase price per year for repairs. On a $300,000 house, that’s $3,000 a year, or $250 a month. It’s a decent starting point for a quick gut check, but it's far too simplistic for a serious analysis.

A much smarter approach is to look at the property's actual condition.

| Property Factor | Maintenance Budget Consideration |

|---|---|

| Age of Roof | A roof that's over 20 years old means you need to be socking away more cash, sooner. |

| HVAC System | If the furnace or AC unit is over 15 years old, a replacement is on the horizon. |

| Plumbing/Electrical | Older, outdated systems can mean more frequent (and expensive) service calls. |

| Property Type | A single-family home has different needs than a condo where an HOA covers the exterior. |

Instead of relying on a generic rule of thumb, get a professional home inspection. That report isn't just a list of problems; it's a roadmap to your future expenses. It allows you to build a maintenance budget that reflects reality. This detailed, honest data collection is the absolute bedrock of a reliable real estate investment property analysis—it turns your spreadsheet from a guess into a powerful decision-making tool.

Crunching the Numbers That Really Matter

Once you’ve got your income and expense figures nailed down, it's time to translate that raw data into actual intelligence. This is where the magic happens in any real estate analysis—we're about to calculate the metrics that tell you if a deal is a goldmine or a money pit. These numbers cut through the emotion and gut feelings to reveal the property's true financial story.

We'll start with the bedrock of all other calculations: Net Operating Income (NOI). This figure tells you how much profit the property itself can generate, completely separate from how you choose to finance it.

Finding Your Net Operating Income (NOI)

Think of NOI as the property's annual profit before you've paid the mortgage. It’s a pure measure of the asset's performance. The formula itself is refreshingly simple:

Gross Operating Income (GOI) - Operating Expenses = Net Operating Income (NOI)

Your Gross Operating Income is just your total potential rent for the year, minus whatever you set aside for vacancies. The operating expenses are all those costs we just covered—taxes, insurance, maintenance, property management, and so on.

Here’s the critical part: your mortgage payment (principal and interest) is NOT included here.

Let's run through a quick example:

- Annual Gross Potential Rent: $30,000

- Vacancy Allowance (5%): $1,500

- Gross Operating Income (GOI): $28,500

- Total Annual Operating Expenses: $11,400

In this scenario, your NOI would be $28,500 - $11,400 = $17,100. This $17,100 is the engine of your investment. It's the money the property generates each year to pay down your loan and deliver your profit.

Using the Cap Rate to Compare Deals Quickly

With the NOI in hand, you can now figure out the capitalization rate, or Cap Rate. This is one of the most common metrics investors use to quickly size up different properties, no matter how they’re financed. It essentially shows you the rate of return if you were to buy the property with all cash.

The formula is: NOI / Purchase Price = Cap Rate

Using our example property with a $17,100 NOI and a $300,000 purchase price:

$17,100 / $300,000 = 0.057, or a 5.7% Cap Rate.

What this means is that if you paid cash, you’d be looking at a 5.7% annual return on your investment. The Cap Rate is so powerful because it lets you make an apples-to-apples comparison between different deals in the same market. A higher Cap Rate often points to higher potential returns, but it can also signal higher risk.

This image from Investopedia gives a great visual breakdown of how the Cap Rate formula works.

The key takeaway is that the Cap Rate directly connects a property's income-generating ability (NOI) to its market value, giving you a standardized benchmark for your analysis.

Finding Your True Profit With Cash Flow

Okay, now let's get to the number that really hits your bank account every month: Cash Flow. This is the actual money left in your pocket after you’ve paid every single bill associated with the property, mortgage included.

The calculation couldn't be simpler: NOI - Debt Service = Annual Cash Flow

"Debt Service" is just a formal term for your total mortgage payments (both principal and interest) over the year. Let's assume your annual mortgage payments on that $300,000 property come out to $14,500.

$17,100 (NOI) - $14,500 (Debt Service) = $2,600 Annual Cash Flow

This means after everything is said and done, the property adds an extra $2,600 to your bottom line each year, which breaks down to about $217 per month. That positive cash flow is your profit and your financial cushion.

A property with negative cash flow means you are feeding it money from your own pocket every month just to keep it afloat. This is a trap nearly every investor, especially those just starting, should avoid at all costs.

The Power of Cash-on-Cash Return

While cash flow tells you how much money you're making, Cash-on-Cash (CoC) Return tells you how hard your invested capital is actually working for you. It measures your annual profit against the total amount of cash you personally put into the deal.

Here’s the formula: Annual Cash Flow / Total Cash Invested = Cash-on-Cash Return

Your "Total Cash Invested" is everything you paid out-of-pocket: your down payment, all your closing costs, and any upfront repair costs. For our example, let's say you put 20% down ($60,000) and paid $7,000 in closing costs, for a total of $67,000 cash invested.

$2,600 / $67,000 = 0.0388, or a 3.9% Cash-on-Cash Return.

This number is incredibly useful because it isolates the performance of your actual cash investment. You can directly compare this 3.9% return to what you might earn from other investments, like the stock market.

Seeing the full picture of your potential return is critical. For a deeper look, check out our complete guide on how to calculate ROI on a rental property, which explores these ideas in even more detail. Getting a firm grip on these calculations is the single most important part of any real estate investment property analysis—it's what empowers you to make smart, data-driven decisions.

How Financing and Market Trends Shape Your Deal

An analysis spreadsheet is a great starting point, but your deal doesn't exist in a vacuum. The numbers you've calculated are constantly being pushed and pulled by two massive outside forces: the financing you get and the health of the market you're buying into. If you get either of these wrong, a deal that looks like a home run on paper can quickly turn into a real-world strikeout.

Think about it: the right loan can supercharge your returns, but the wrong one can bleed your cash flow dry and torpedo the entire investment. In the same way, a fantastic property in a market that's bleeding jobs is an uphill battle you don't want to fight. A truly thorough real estate investment property analysis has to stress-test your numbers against these variables to see the complete picture.

Modeling Different Financing Scenarios

Leverage—using the bank's money to buy a property—is the classic double-edged sword. It can seriously magnify your returns, but it also dials up your risk. That’s why it's absolutely critical to compare different financing options side-by-side to see how they really impact your bottom line.

Let's take a $300,000 property as an example. You might be surprised how much of a difference a slightly larger down payment can make.

| Metric | Scenario A (20% Down) | Scenario B (25% Down) |

|---|---|---|

| Down Payment | $60,000 | $75,000 |

| Loan Amount | $240,000 | $225,000 |

| Monthly P&I | ~$1,719 (at 7%) | ~$1,614 (at 7%) |

| Monthly Cash Flow | $181 | $286 |

Look at that. By putting down just 5% more upfront, the monthly cash flow skyrockets by over 57%. That extra cash isn't just a number; it's a real buffer against a surprise HVAC repair or an unexpected vacancy, making your entire investment more durable. Your initial cash-on-cash return might dip slightly with the larger down payment, but the trade-off for improved stability is often well worth it.

Key Takeaway: Never, ever just accept the first loan quote you get. You need to model out different down payments, interest rates, and loan terms. This is where tools like Property Scout 360 become invaluable, letting you run these comparisons in seconds to see exactly how each lever affects your cash flow and long-term wealth.

Reading the Broader Market Signals

A property-level analysis is only one half of the equation. You could find a deal with absolutely killer numbers, but if it's located in a city with a shrinking job market and people moving away, you're essentially betting against the tide. Vetting the market is just as vital as vetting the property itself.

You have to become a student of the big-picture trends. Look for positive signs that point to a healthy, growing environment where your investment can thrive.

- Job Growth: Are big companies moving in or expanding? A strong, diverse job market is the engine that fuels housing demand.

- Population Trends: Is the metro area gaining new residents year after year? Consistent population growth is a powerful driver for both rental demand and property values.

- Local Regulations: Is the city considered landlord-friendly? Get familiar with the local rules on things like rent control, eviction processes, and property taxes. These can have a huge impact on your actual profits.

These macro factors are creating some serious tailwinds for investors right now. A global housing affordability crisis, for example, is causing a huge shift toward renting. In many developed economies, over 80% of households are leaning toward renting instead of owning as of 2025. This is largely driven by a massive housing shortage, with some estimates showing a deficit of 6.5 million units in certain markets. You can dig deeper into these trends by exploring the insights on global housing and rental demand.

When you understand these larger forces, you can invest with much more confidence, knowing the market is working with you, not against you. Your analysis becomes far more robust when you can connect your property-specific numbers to the economic heartbeat of the entire area.

Validating Your Numbers with Due Diligence

Your spreadsheet might look perfect, showing great cash flow and a solid ROI, but right now, it's just a hypothesis. The real test begins now. This is the due diligence phase—your chance to get on the ground, verify every single number, and make sure your investment is built on a foundation of fact, not hope.

This isn’t about being pessimistic; it's about being a professional. A deal has to work in the real world, not just on paper. Let's dig in and confirm what you've projected.

The Physical Inspection Checklist

First up is the property itself. Yes, you'll hire a professional home inspector, but you need to walk through it with an investor's mindset. Your inspector is checking for code violations and safety issues. You’re hunting for the budget-killers.

Bring a checklist and zero in on the big-ticket systems. These are the things that can drain your reserves in a heartbeat if they fail.

- Roof and Foundation: Are there missing shingles? Water stains on the ceiling? Any visible cracks in the foundation? These are massive red flags that need a specialist to evaluate, period.

- HVAC System: Find out the age of the furnace and AC units. Anything over 15 years old is on borrowed time, and you should be planning for its replacement in your numbers.

- Plumbing and Electrical: Turn on the faucets, look under every sink. Open the electrical panel. An old fuse box instead of a modern breaker system is a sign of a costly—and potentially uninsurable—upgrade on the horizon.

An inspection report isn’t a pass/fail document. Think of it as your future capital expenditure plan. Every problem you find is a bargaining chip you can use to negotiate a lower price or ask for seller credits.

Soft Due Diligence for Occupied Properties

If the property comes with tenants, your job gets a lot more complex. You aren't just buying a building; you're taking over a running business, complete with contracts and customers. This "soft" due diligence is critical for understanding the true financial health of the asset.

You absolutely must get your hands on and review these documents:

- Tenant Leases: Scrutinize every lease. Do the rent amounts and expiration dates match what the seller advertised? Are there any odd clauses or concessions you need to know about?

- Payment History: A rent roll showing the last 12 months of payment history is non-negotiable. A history of late payments is a huge warning sign, pointing to future management headaches and costly evictions.

- Tenant Estoppel Certificates: This is a crucial legal document. Each tenant signs it to confirm the core facts of their lease (rent amount, security deposit, etc.). This prevents them from coming back to you later and claiming the terms were different.

Skipping this step is a rookie mistake that can turn a great deal into a nightmare overnight. It’s how you confirm the income you’ve so carefully modeled is real and collectible.

As market conditions evolve, this kind of rigorous validation is more important than ever. While investor sentiment is looking cautiously optimistic for 2025 with transaction volumes expected to rebound from 2024 lows, you can't rely on market momentum alone. For a deeper dive into what experts are seeing, check out the Emerging Trends in Real Estate report from ULI and PwC. A thorough due diligence process ensures your deal is grounded in proven facts, not just optimistic projections.

A Real-World Property Analysis Case Study

Let's put all this theory into practice. I find the best way to really grasp these concepts is to walk through a deal from start to finish, just as you would in the real world. This gives you a repeatable blueprint for analyzing your own potential investments.

Imagine we're looking at a three-bedroom, two-bathroom single-family home. It’s in a decent, growing suburban neighborhood and the seller is asking $325,000.

Assembling the Key Inputs

First things first, we need to get our basic numbers down. You can't analyze anything without knowing your initial costs and potential income.

- Purchase Price: $325,000

- Down Payment: 20% ($65,000)

- Closing Costs: I usually budget around 3% for this, so that’s $9,750.

- Total Cash Needed: $65,000 + $9,750 = $74,750

With the "out-of-pocket" cost clear, we turn to income. After a quick look at rental comps in the area and a chat with a local property manager, a conservative estimate for monthly rent is $2,400. That gives us an annual Gross Potential Income of $28,800.

Modeling Expenses and Calculating Metrics

Now for the less glamorous but equally critical part: the expenses. I always use percentages for things like vacancy and repairs because it builds in a realistic buffer.

| Expense Category | Annual Cost | Calculation |

|---|---|---|

| Property Taxes | $4,225 | (1.3% of purchase price) |

| Insurance | $1,500 | (Quote from local agent) |

| Vacancy (5%) | $1,440 | (5% of Gross Income) |

| Repairs (5%) | $1,440 | (5% of Gross Income) |

| Management (8%) | $2,304 | (8% of Gross Income) |

| Total Expenses | $10,909 |

After subtracting our total expenses from our gross income, we get a Net Operating Income (NOI) of $17,891 ($28,800 - $10,909). This gives us a 5.5% Cap Rate, which feels pretty solid for this kind of property.

But here's where the rubber meets the road. Let's say our mortgage payment comes out to $1,738 per month, or $20,856 a year. That leaves us with a final monthly cash flow of -$247.

That negative cash flow is a deal-breaker. It means I'd be feeding the property money out of my own pocket every single month. Based on these numbers, it’s an immediate "no."

This is exactly why we run the numbers. The house might look great and the neighborhood might be perfect, but the investment simply doesn't support itself with this financing. It’s a perfect example of how a disciplined, data-driven process saves you from making an expensive, emotional mistake.

For more examples of how this plays out in different situations, looking at a variety of real estate investment case studies can be incredibly helpful for seeing how different deals pencil out.

Got Questions About Property Analysis? We've Got Answers

Even with the best framework in hand, running the numbers on a potential investment property always brings up a few questions. It happens to everyone, from first-timers to seasoned pros. Let's dig into some of the most common questions that pop up, because getting these right is key to building confidence and avoiding those classic, costly mistakes.

What's the Single Most Important Metric to Watch?

This is a trick question. There isn’t just one magic number. The real power comes from seeing how they all work together to paint the full picture of a deal. Too many new investors latch onto one metric, usually the Cap Rate, and that's a classic rookie move.

- Cap Rate is fantastic for a quick, apples-to-apples comparison of properties in the same neighborhood, completely ignoring the financing side of things. Think of it as a measure of the property's raw, unleveraged earning potential.

- Cash-on-Cash Return makes it personal. This number tells you exactly how hard your cash—the money you actually pull out of your pocket for the down payment and closing—is working for you.

- Cash Flow is the ultimate reality check. It’s what’s left in the bank account each month. This determines whether the property pays for itself or if you'll constantly be dipping into your own funds to keep it afloat.

Remember, a sky-high Cap Rate means nothing if your loan terms leave you with negative cash flow every single month. You really need to look at all of them to get a balanced perspective.

The "best" metric is whichever one lines up with your goals. If you need income to live on right now, Cash Flow is king. If you're betting on a hot market and playing the long game, Cap Rate and appreciation potential might be more your focus. Your strategy is what matters.

How Can I Realistically Budget for Surprise Repairs?

Let's be clear: unexpected expenses aren't a possibility, they're a certainty. The old "1% rule" (budgeting 1% of the home's value for annual maintenance) is a decent starting point, but honestly, it’s often not enough, especially if you're looking at an older building.

A much better approach is to build a dedicated Capital Expenditures (CapEx) fund.

Start by getting a real sense of the age and condition of the big-ticket items—the roof, the HVAC system, plumbing, and the water heater. If the roof is already 20 years old, you know a five-figure bill is coming your way sooner rather than later.

A good, conservative practice is to set aside 5-10% of your gross monthly rent just for these big, predictable-but-infrequent repairs. This is totally separate from your day-to-day maintenance budget for leaky faucets and running toilets.

What Happens if My Projections Are Way Off?

They will be. Maybe not way off, but they'll never be perfect. No one has a crystal ball.

The secret is to stress-test your numbers from the very beginning. Always be conservative. If you think the vacancy rate in the area is 5%, run your numbers at 8%. Pad your repair budget. Use rental comps that are realistic, not the absolute highest rent ever achieved in the zip code. This builds a buffer, a margin of safety, right into your analysis.

If a deal still looks good with your more pessimistic numbers, you've probably found a winner. But if it only works in a perfect, best-case scenario? That’s a sign that the deal is way too fragile and you should probably walk away.

Stop drowning in spreadsheets and start making confident investment decisions. Property Scout 360 gives you instant, comprehensive property analysis, from cash flow to ROI, so you can evaluate deals in minutes, not weeks. Find your next profitable investment at Property Scout 360.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.