The Ultimate Fix and Flip Calculator for Smarter Investments

Discover how a fix and flip calculator can transform your real estate deals. Get actionable insights to accurately forecast costs, ARV, and maximize your ROI.

At its core, a fix and flip calculator is your financial co-pilot for any house flipping project. It’s a specialized tool—often a spreadsheet or software—that lets you systematically crunch all the numbers involved, taking you from a rough idea to a clear projection of your potential profit or loss. This isn't about guesswork; it's about making decisions backed by cold, hard data.

Why a Calculator Is Your Most Important Flipping Tool

Before you even think about swinging a sledgehammer or picking out new kitchen cabinets, your first move should always be to fire up a reliable fix and flip calculator. I’ve seen it time and again: successful flipping is a game of razor-thin margins. A single miscalculation can be the difference between a big payday and a costly mistake.

While your gut instinct might help you spot a diamond in the rough, it's the numbers that tell you if that diamond is actually worth polishing. A calculator serves as a reality check, forcing you to confront every single cost and variable before you commit a dollar.

From Chaos to Clarity

A good calculator brings order to the financial chaos of a flip. It prompts you to think beyond the obvious big-ticket items like the purchase price and the main rehab budget. Instead, it guides you to account for all the little things that can silently eat away at your profit.

Before you can get a clear picture of profitability, you'll need to gather some essential data. Think of these as the core ingredients for your financial analysis.

Core Inputs for Your Fix and Flip Analysis

Here’s a quick overview of the essential data points you need to gather for an accurate profitability projection.

| Data Point | What It Represents | Why It Is Essential |

|---|---|---|

| Purchase Price | The initial cost to acquire the property. | The starting point for all calculations; your largest upfront expense. |

| Rehab Costs | A detailed breakdown of all renovation expenses. | Accuracy here is critical. Underestimating this can doom a project. |

| Holding Costs | Ongoing expenses during the flip (e.g., taxes, insurance, utilities). | These "soft costs" add up every month you own the property. |

| Financing Costs | All loan-related fees (e.g., origination points, interest). | Determines the true cost of borrowing money for the project. |

| Closing & Selling Costs | Fees on both the purchase and sale (e.g., agent commissions). | These can easily represent 5-10% of the final sale price. |

By plugging these figures into a calculator, you transform a messy collection of estimates into a clean, predictable financial forecast.

A common mistake for new flippers is underestimating the sheer number of small costs that add up. A calculator doesn't let you forget about things like property insurance or monthly utility bills, which can easily total thousands over a six-month project.

Introducing Foundational Flipping Concepts

Working with a fix and flip calculator naturally introduces you to the core principles that guide professional investors. Two of the most important are the After-Repair Value (ARV) and the 70% Rule.

The ARV is simply an educated estimate of what the property will be worth after you've completed all the renovations. You determine this by analyzing recent sales of similar, updated homes in the area, often called "comps."

From there, you can apply the 70% Rule, a classic rule of thumb that helps investors quickly gauge a deal's potential. The rule states that you should aim to pay no more than 70% of the property's ARV, minus the total repair costs. This simple formula builds in a buffer for your profit and unforeseen expenses.

Even in Q1 2025, when the fix-and-flip market accounted for 8.3% of all home sales, this rule remained a vital guideline for investors. To get a better sense of how market conditions influence your numbers, you can explore more insights into recent fix-and-flip market trends.

Gathering the Numbers That Actually Matter

A fix-and-flip calculator is a powerful tool, but it's only as good as the numbers you put into it. Garbage in, garbage out, as they say. To get a realistic financial forecast, you need to fuel it with accurate, well-researched data—not ballpark estimates or wishful thinking.

Let's walk through how to pin down the critical inputs that will make or break your deal analysis.

The success of your entire project hinges on one number: the After-Repair Value (ARV). This isn’t a wild guess; it’s a data-backed prediction of what your property will be worth after you’ve put in all the work. Getting this wrong is the fastest way I've seen investors lose money on a flip.

To nail down a defensible ARV, you have to get deep into comparable sales, or "comps." These are recently sold properties in the immediate area that look a lot like your property will after the renovation is complete.

- Proximity is king: Stick to comps within a half-mile radius if you can. The closer, the better.

- Time is of the essence: Only look at homes sold in the last three to six months. Markets can turn on a dime.

- Compare apples to apples: Your comps should closely match key features like square footage, bed/bath count, lot size, and architectural style.

A huge part of this is mastering the art of accurately pricing a home for sale to figure out its potential ARV. For a deeper dive, our article on finding and analyzing free real estate comps has more strategies you can use.

Building Your Renovation Budget

Once your ARV is locked in, the next big piece of the puzzle is your total renovation cost. This is where a lot of new investors get into trouble by underestimating expenses. A vague figure like "$40,000 for everything" isn't a budget; it's a gamble.

What you need is a detailed, line-item budget. That means getting on the phone and getting real quotes from contractors for the big-ticket items—roofing, HVAC, plumbing, and electrical. For cosmetic stuff, you can start with price-per-square-foot estimates, but firm quotes are always the goal. For instance, in many markets, a good-looking cosmetic rehab might run you $30–$40 per square foot.

Investor Insight: Never, ever forget your contingency fund. I set aside at least 10-15% of my total rehab budget for every single project. This isn't "extra" cash; it’s a non-negotiable line item for the inevitable surprises, like hidden water damage, permit headaches, or a sudden jump in material costs. A $50,000 rehab budget needs a $5,000 to $7,500 contingency, period.

Your detailed scope of work should cover everything, from the major systems down to the small details:

- Labor Costs: Hard quotes from your electrician, plumber, roofer, painters, and GC.

- Material Costs: Flooring, cabinets, countertops, light fixtures, paint, and landscaping supplies.

- Permits and Fees: Don't forget what the city will charge you; these can vary wildly.

- Contingency Fund: Your mandatory cushion for when things go wrong.

When you get this granular, your rehab estimate transforms from a guess into a solid financial plan.

The calculator above shows exactly why this detail matters. It forces you to think about each cost category separately—from the purchase price to specific rehab items—so nothing critical gets overlooked.

Accounting for Hidden Costs

Heads up: your expenses don't stop when the last nail is hammered in. You'll keep bleeding cash for as long as you own the property. These are your "holding costs" or "soft costs," and they can eat into your profit in a big way if you don't account for them in your calculator.

Remember, these costs are a ticking clock—the longer the project drags on, the more you pay.

- Property Taxes: Based on the property's assessed value.

- Insurance: You'll need a builder's risk or vacant property policy, which isn't cheap.

- Utilities: Even an empty house needs power, water, and maybe gas to keep things running for your crew.

- Loan Interest: If you're using financing, this is probably your biggest monthly holding cost.

- HOA Fees: If there's an HOA, they'll want their money every month, occupied or not.

Finally, don't forget the costs to buy the property and then sell it. These transaction costs can easily add up to 5-10% of the property’s value. This includes agent commissions (typically 5-6% of the final sale price), title insurance, escrow fees, transfer taxes, and any seller concessions you might need to offer the buyer. Plugging these numbers in accurately is the only way to get a net profit figure you can actually take to the bank.

Understanding the Math Behind Your Profit

A fix-and-flip calculator isn't some black box spitting out random numbers. It’s an engine running on straightforward, battle-tested formulas. Honestly, getting a handle on this math is what separates the investors who consistently make money from those just hoping for the best.

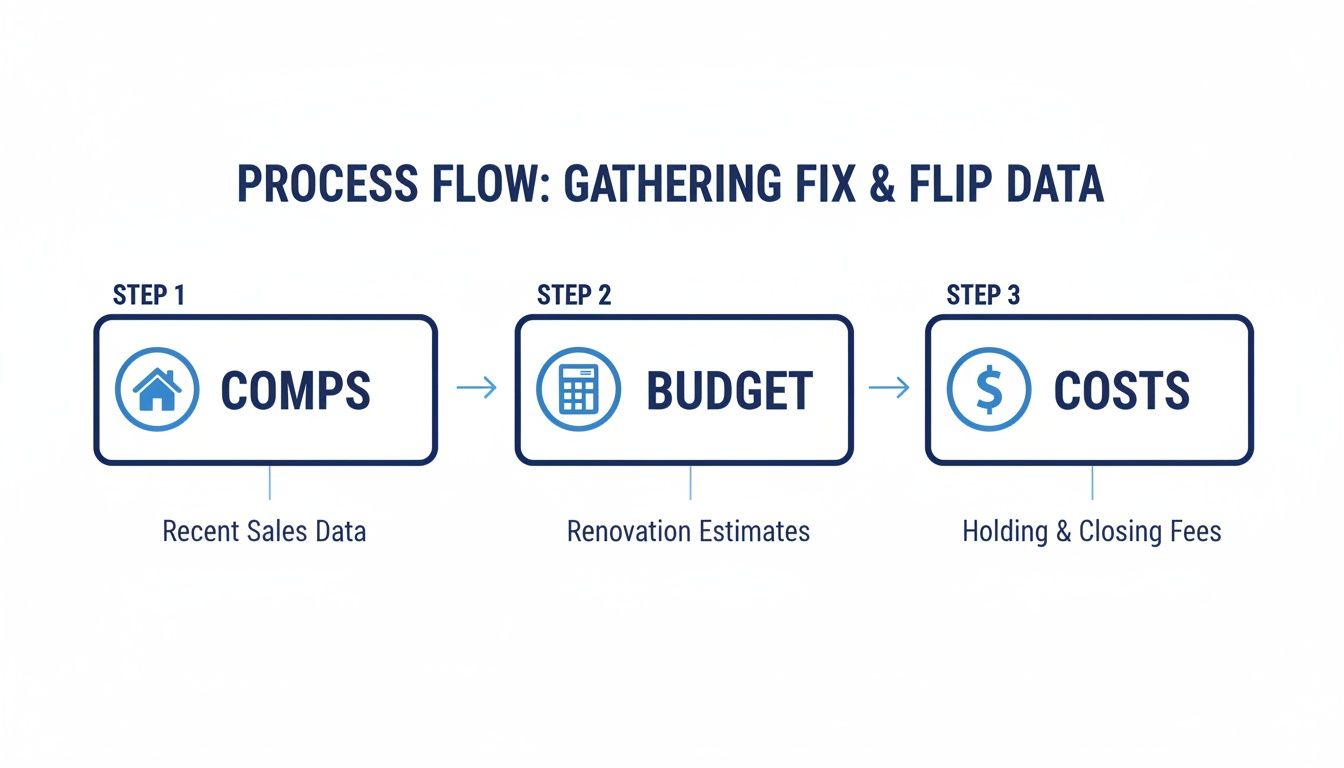

Let's pull back the curtain and see exactly how your deal's potential gets calculated, number by number.

This whole process really boils down to three key stages: finding solid comps, building a realistic rehab budget, and accounting for every single cost along the way.

As you can see, a profitable flip always starts with solid data. It’s all about nailing that ARV, locking down your budget, and then tracking all the other costs that inevitably pop up.

The Cornerstone Formula: ARV and Total Project Cost

Everything hinges on the After-Repair Value (ARV). This is your best estimate of what the house will be worth on the market after you’ve worked your magic. Your entire financial projection is built on this one critical number.

Once you have a defensible ARV backed by solid comps, you can figure out your Total Project Cost. And I don’t just mean the purchase price plus the renovation budget. It’s the all-in number, covering every dollar you'll spend from the day you buy to the day you sell.

Total Project Cost = Purchase Price + All Rehab Costs + All Holding & Closing Costs

Getting this formula right means you've accounted for everything, from the down payment and loan fees to the final real estate agent commissions. A good calculator forces you to think through every variable, which is how you avoid those nasty, profit-killing surprises.

From Gross Profit to Net Profit

With your ARV and Total Project Cost nailed down, figuring out your profit is just simple subtraction. The first number you’ll get is your Gross Profit, which is what’s left after selling the house and paying for its purchase and renovation.

Gross Profit = After-Repair Value (ARV) - Total Project Cost

But gross profit isn't the whole story. To find your Net Profit—the actual cash that hits your bank account—you have to subtract all your financing costs. This includes things like loan origination fees, points, and all the interest you paid while you held the property.

Net Profit = Gross Profit - Total Financing Costs

This is your true bottom line. If you just need a quick look at a deal's potential, a specialized Flip Profit Estimator can give you a rapid assessment to see if it's even worth a deeper dive.

Measuring Success: Key Performance Metrics

While net profit is the end goal, seasoned investors use more sophisticated metrics to compare deals. Two of the most important are Return on Investment (ROI) and Cash-on-Cash Return (CoC). Each one tells you something different but equally important about your deal's performance.

Return on Investment (ROI) gives you the big-picture view, measuring the efficiency of all the money in the project, including what you borrowed.

- Formula: ROI = (Net Profit / Total Project Cost) x 100

- What it tells you: For every single dollar invested in the entire project, what percentage did you get back as profit?

Cash-on-Cash Return (CoC) is more personal. It zeroes in on the return you got specifically on the cash you pulled out of your own pocket.

- Formula: CoC Return = (Net Profit / Total Cash Invested) x 100

- What it tells you: How hard did your own money actually work for you? This is a huge deal for investors using loans to fund their projects.

For instance, say you clear a $30,000 net profit on a flip where you only had to put in $60,000 of your own cash. Your Cash-on-Cash Return is a fantastic 50%. This is the metric that really shows you the power of your capital.

While these are the go-to metrics for flipping, other calculations can offer even deeper financial insights. For a more advanced look, our guide on using an Internal Rate of Return calculator for real estate can add another powerful layer to your analysis.

Discipline is what separates the amateurs from the pros. It's no accident that professional flippers see success rates as high as 85%; they stick to proven formulas, like the famous 70% Rule (Maximum Purchase Price = ARV x 0.70 - Repairs).

This discipline, supercharged by a reliable calculator, is how you thrive. It lets you navigate a market where 64% of investors expect conditions to stay flat or even weaken, turning solid data into profitable deals by removing emotion from the equation.

Using Your Calculator to Stress-Test a Deal

Your first analysis of any potential flip is almost always optimistic. It's easy to get excited when you run the numbers for a perfect project where everything goes right.

But here’s the thing—in real estate, perfection is a myth. This is where a good fix and flip calculator becomes more than just a profit estimator; it turns into your most important risk management tool.

Stress-testing a deal means asking the tough "what if" questions and letting the numbers give you brutally honest answers. It’s how you find a deal’s breaking point before you put any money down, protecting your capital and ensuring you stay in the game for the long haul.

Modeling Your Best, Likely, and Worst-Case Scenarios

The goal isn't just to see how much you can make, but to understand the full range of possible outcomes. A smart investor has a plan for rainy days, not just sunny ones. Let's walk through an example to see how this plays out.

Imagine you've found a property. Your initial analysis—the "likely case"—looks like this:

- Purchase Price: $200,000

- Rehab Budget: $50,000

- After-Repair Value (ARV): $330,000

- Holding & Selling Costs: $25,000

- Project Timeline: 6 months

When you plug these figures into your calculator, you see a projected net profit of $55,000. That looks fantastic on paper. But what happens when reality decides to show up? While you can perform a similar analysis for buy-and-hold properties with a dedicated rental property calculator xls, flipping numbers are far more sensitive to budget and timeline creep.

Scenario Two: The Inevitable Budget Overrun

Now, let's model a "worst-case" scenario. This is where things get real. The single most common issue on a flip is the renovation budget getting out of hand. Let's say your contractor opens a wall and finds some nasty electrical problems, and on top of that, your lumber costs just jumped.

Your rehab budget suddenly swells by 20%, tacking on an extra $10,000.

- New Rehab Budget: $60,000 ($50,000 + $10,000)

- New Total Cost: $285,000

- New Net Profit: $45,000

Just like that, your profit nosedives by nearly 18%. The deal is still in the black, but your cushion for any other mistakes just got a lot thinner. This is crucial information to have.

Scenario Three: The Slow-Moving Market

Here's another headache every flipper faces eventually. The renovation is perfect, but the local market cools off. Your beautiful, finished house just sits there for an extra 90 days (3 months) before you get a serious offer.

Remember, every single day a property sits unsold, it's costing you money in holding costs—taxes, insurance, utilities, and loan interest.

Assuming your monthly holding costs are $2,000, that delay adds a painful $6,000 to your expenses.

- New Holding & Selling Costs: $31,000 ($25,000 + $6,000)

- New Total Cost: $281,000

- New Net Profit: $49,000

While less severe than the major budget overrun, a slow sale still takes a significant bite out of your bottom line.

Investor Insight: The real danger is when these problems stack up. What if your budget runs 20% over and the house sits on the market for an extra 90 days? Your total surprise costs hit $16,000, dropping your profit from $55,000 to a mere $39,000. That's a 29% profit haircut. Knowing this risk upfront gives you the leverage to negotiate a lower purchase price and build a bigger safety net into the deal.

Building Your Margin of Safety

Running these different scenarios isn't about being pessimistic; it's about being strategic. You're building a margin of safety. Your fix and flip calculator helps you identify the break-even point—the line where unexpected costs completely erase your profit.

Here’s how you can lay out your stress test:

| Scenario | Key Variable Changed | New Net Profit | Profit Change |

|---|---|---|---|

| Likely Case | Baseline Projection | $55,000 | - |

| Best Case | Sell for $10k over ARV | $65,000 | +$10,000 |

| Worst Case 1 | Rehab is 20% over budget | $45,000 | -$10,000 |

| Worst Case 2 | Sits on market 90 extra days | $49,000 | -$6,000 |

| Worst Case 3 | Both problems combined | $39,000 | -$16,000 |

This simple table, easily generated from your calculator inputs, gives you a clear, unflinching look at the deal's durability. It tells you exactly how much pressure the project can handle before it cracks. If a minor 10% budget overrun or a short delay pushes your deal into the red, it’s a clear sign to walk away. This is how you make smarter, more resilient investment decisions.

Common Calculator Mistakes That Cost Investors Money

Even the best fix and flip calculator is only as good as the numbers you put into it. The tool itself is just a machine for math; the real danger lies in the data. The most expensive errors don't come from a broken formula, but from flawed inputs that can doom a project before you even close on the property.

These mistakes aren't just minor miscalculations—they're the silent killers of your profit margin. I've seen investors spend weeks hunting down a great deal, only to watch their expected payday evaporate because of a simple oversight made on day one.

Let's walk through the most common pitfalls so you can make sure your projections are grounded in reality, not fantasy.

Underestimating the Renovation Budget

The single biggest mistake I see, time and time again, is being way too optimistic about renovation costs. A vague guess of "$50,000 for everything" isn't a budget; it's a bet, and a bad one at that. This is where a promising deal can completely fall apart before the first sledgehammer swings.

Seasoned investors know that a realistic budget is built item by item, not with a broad brushstroke. Critically, it always includes a contingency fund.

- The Contingency Rule: You absolutely must set aside 10% to 15% of your total renovation budget as a dedicated contingency. This isn't just "extra" money; it's a non-negotiable line item for the things you will inevitably find—hidden water damage, faulty wiring you didn't see, or unexpected permit delays.

- The "Dollar-for-Dollar" Guideline: A great rule of thumb, especially for newer flippers, is to aim for a net profit that’s at least equal to your renovation spend. If your rehab budget is $40,000, you should be targeting $40,000 or more in net profit. This builds in a natural buffer for risk.

Forgetting this buffer is like going to sea without a life raft. When something goes wrong—and trust me, it almost always does—your profit is the first thing to go overboard.

Using an Inflated After-Repair Value

The second deadly sin is falling in love with a property's potential and fudging the After-Repair Value (ARV) to make the deal work on paper. This is just wishful thinking, plain and simple. Your ARV has to be based on hard, recent, and hyper-local comparable sales ("comps"), not on what you hope the house will be worth.

One of my guiding principles is to never, ever assume a property will sell for more than the highest recent comp in the immediate area. The moment you project an ARV higher than what has already been proven, you've stopped investing and started gambling. Stay conservative; it’s what keeps you in the game long-term.

An overly optimistic ARV creates a domino effect. It tricks you into overpaying for the property, taking on too much debt, and sinking money into a renovation the market simply won't pay for. It’s a recipe for financial loss.

Forgetting About Soft Costs

Finally, a lot of investors get tunnel vision on the big numbers—the purchase price and the rehab budget. In the process, they completely forget about the "soft costs." These are the quiet, relentless expenses that bleed your profits dry every single day you own the property.

These costs are almost always missed in a quick "back-of-the-napkin" analysis, but they are essential inputs for any serious fix and flip calculator.

- Holding Costs: Think property taxes, insurance, utilities (power, water, gas), and of course, your loan interest payments. On a six-month project, these can easily add up to thousands of dollars you didn't account for.

- Transaction Costs: When you sell, the expenses come fast. Agent commissions (typically 5-6% of the sale price), title insurance, escrow fees, and transfer taxes can take a massive bite out of your gross profit. As a quick rule, I estimate these at around 10% of the ARV for a conservative, all-in projection.

By deliberately planning for these often-forgotten expenses, your calculator will show you the true picture of your potential net profit—which is the only number that really matters.

Frequently Asked Questions

Even with the best tools, you're going to have questions—especially when your hard-earned money is on the line. Let's tackle some of the most common things investors ask about using a fix and flip calculator.

How Accurate Is a Fix and Flip Calculator?

A calculator is only as smart as the numbers you feed it. Its accuracy is a direct reflection of your own due diligence.

The old saying "garbage in, garbage out" couldn't be more true here. If you put in a well-researched ARV based on solid comps, detailed contractor bids, and a complete list of all your costs, the numbers it spits out will be a reliable forecast. The calculator itself just does the math; it's your research that makes it a powerful tool.

What Is the 70 Percent Rule in House Flipping?

The 70% Rule is a classic back-of-the-napkin test investors use to quickly vet a potential deal. It states that you should pay no more than 70% of the property's After-Repair Value (ARV), minus the estimated rehab costs.

The formula looks like this: Maximum Offer = (ARV x 0.70) - Rehab Costs.

That remaining 30% isn't all profit. It's a buffer designed to cover your holding costs, financing, selling expenses, and your final profit margin. It's a fantastic starting point, but remember it's just a guideline—hot markets might force you to adjust that percentage.

Can I Just Use a Spreadsheet Instead of a Special Tool?

Of course. Plenty of veteran investors live and die by their custom-built spreadsheets in Excel or Google Sheets. Going this route gives you total control to tweak formulas and layouts to match your exact strategy.

But for most flippers, especially when you're starting out, a dedicated online calculator has some real advantages.

- You Won't Forget Anything: They come pre-loaded with every possible expense category, so you don't overlook crucial costs like title insurance or transfer taxes.

- Quick Scenario Planning: It's much easier to instantly see how a different sales price or a bigger rehab budget impacts your bottom line, without worrying about breaking a formula.

- Built-in Data: Some advanced calculators can pull in live market data, saving you hours of manual research on comps and local costs.

How Much Should I Really Budget for Contingencies?

Your contingency fund is what saves your profit from the inevitable surprises. A solid rule of thumb is to set aside 10% to 20% of your total estimated renovation budget. This isn't optional—it's a non-negotiable line item that protects your entire investment.

So, how do you know if you need 10% or 20%?

- Lean towards 15-20% if: You're new to flipping, the house is a gut job with major unknowns (think foundation or electrical issues), or you don't have firm bids from your contractors yet.

- Stick closer to 10% if: The project is mostly cosmetic, you have locked-in bids from a team you trust, and you've done similar flips dozens of times.

Think of it as the safety net for your capital. Experienced flippers will tell you the contingency fund is what lets them sleep at night, because every single renovation project has surprises.

Stop drowning in spreadsheets and start making smarter, faster investment decisions. The Property Scout 360 platform streamlines every calculation we've discussed, from ARV analysis to cash-on-cash return, giving you the clarity and confidence to find your next profitable deal in minutes, not weeks. Learn more about Property Scout 360.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.