How to Find an Investment Property and Build Real Wealth

Learn how to find an investment property that generates returns. This guide covers market analysis, deal sourcing, financial modeling, and closing strategies.

Before you even think about scrolling through property listings, the real work begins. The secret to finding a great investment property isn't about luck; it's about creating a personal investment thesis before you start the hunt.

You need to get crystal clear on your financial goals, pick an investment strategy like buy-and-hold or BRRRR, and lock in a firm budget that includes plenty of cash reserves. This initial groundwork is your filter—it makes sure you only spend time on deals that actually get you closer to where you want to go.

Building Your Investment Thesis Before You Browse

The most important part of your property search happens right at your kitchen table, not on a property tour. A successful hunt is driven by a clear, intentional strategy—not by emotion or a hot tip from a friend. This foundational plan is your investment thesis, and it's the playbook that will guide every single decision you make from here on out.

Without this compass, you'll end up chasing deals that don't actually fit your financial life. It's a classic rookie mistake that wastes countless hours analyzing properties that were never a good match in the first place.

Define Your Primary Goal

First things first: what are you trying to accomplish? The answer completely dictates the kind of property you'll be looking for. Most investors fall into one of two camps: cash flow or appreciation. They often lead to very different investments.

- Cash Flow Focus: Your main objective is to generate consistent monthly income that more than covers your expenses (mortgage, taxes, insurance, maintenance). This is a great path for supplementing your income or building a passive revenue stream for retirement.

- Appreciation Focus: You're betting on the property's value shooting up over time. This is a long-term play where the big payday comes when you eventually sell for a hefty profit.

Of course, everyone wants a bit of both. But deciding on your primary focus is key. A cash flow investor might be looking at a fully rented triplex in a stable Midwest market. On the other hand, an appreciation investor might snap up a single-family home in an up-and-coming neighborhood near a new tech campus.

Choose Your Investment Strategy

Once you know your goal, you can pick the right vehicle to get you there. It's a good idea to dig into some proven strategies for investing in rental property to see what resonates with your goals and resources.

I see it all the time: new investors failing to match their strategy to their resources. And I don't just mean money—I mean their available time and expertise. A hands-on BRRRR deal requires a totally different skill set than buying a passive, turnkey rental.

Here are a few of the most common strategies:

- Buy and Hold: The classic. You purchase a property and rent it out for years, benefiting from both long-term cash flow and appreciation.

- BRRRR (Buy, Rehab, Rent, Refinance, Repeat): This is a value-add strategy. You find a distressed property, fix it up to force the appreciation, and then refinance to pull your initial capital back out to do it all over again.

- House Hacking: You buy a multi-unit property (like a duplex or triplex), live in one unit, and have the tenants in the other units pay down your mortgage.

Establish Your All-In Budget

Finally, it's time to get brutally honest with your numbers. Your budget is so much more than just what you can put down. A realistic financial plan has to account for three key components:

- Down Payment: For an investment property, you can’t get away with 3% down. Lenders are going to require 20-25%.

- Closing Costs: Plan on an extra 2-5% of the purchase price to cover all the lender fees, appraisals, and title insurance.

- Cash Reserves: This is non-negotiable. I tell every investor to have 3-6 months of the property’s total expenses (PITI, plus a vacancy factor) sitting in a separate account. This is your safety net for when the A/C unit dies or a tenant moves out unexpectedly.

With your goals, strategy, and budget nailed down, you’ve built a powerful filter. You're no longer just browsing properties—you're strategically hunting for a specific asset that fits your personal investment thesis perfectly.

Pinpointing Markets with Untapped Potential

Alright, you’ve got a solid investment thesis. Now comes the fun part: finding a market where that strategy can actually thrive. We’ve all heard "location, location, location" a million times, but a truly great investment market is so much more than a zip code with nice curb appeal. It’s an economic engine.

To do this right, you need to start thinking more like an economist and less like a typical homebuyer. We’re hunting for places with strong fundamentals that point to a growing, sustained demand for housing. Skipping this step is like planting a prize-winning seed in barren soil—it just won't work, no matter how good your intentions are.

Look for Strong Job Growth

The number one driver of rental demand, without question, is a healthy job market. When companies expand or relocate, they bring people—and those people need a place to live. It’s a simple cause-and-effect that boosts the entire local economy, making it a fantastic place for a long-term investment.

Don't just look for any jobs, though. Dig a little deeper.

- Diversity is Key: A town built on a single factory is a house of cards. Look for a mix of industries like healthcare, tech, education, and logistics. This creates resilience.

- Follow the Growth: A rising job market almost always comes before rising rents and property values. It’s the leading indicator I watch most closely.

Follow Population Trends

People vote with their feet. A market with a steadily climbing population is a massive green flag, signaling that people want to be there. This directly fuels housing demand and puts upward pressure on both rental rates and home prices.

But don’t just look at the total number. The demographics tell the real story. Are young professionals moving in for tech jobs? Is it a hotspot for families or a growing retirement community? Knowing who is moving there helps you tailor your property type to your future tenants.

Analyze Rental Demand and Vacancy Rates

Here’s a hard lesson many new investors learn: a great market for flipping is not always a great market for renting. You have to confirm there's strong, unmet demand specifically for rentals. High demand means low vacancy, and low vacancy is the cornerstone of consistent cash flow.

The metric you need to obsess over is the vacancy rate. A low rate, typically below 5%, signals a tight market where you’ll have your pick of qualified tenants. On the flip side, a high or climbing vacancy rate is a major red flag that could mean oversupply or a weak local economy.

A classic rookie mistake is chasing a "hot" market with soaring home prices but terrible rental yields. You need both appreciation potential and cash flow. A city with 3% population growth and 12% rent growth is a far stronger bet than one with 1% population growth and 15% price growth. Focus on what supports tenants.

Understanding the Bigger Economic Picture

Zooming out, the broader real estate market gives us crucial clues. After a recent correction, global private real estate values are showing renewed strength. Transaction volumes in major markets have climbed to $739 billion over the past year—a 19% year-over-year jump that signals returning confidence.

For us in the U.S., this means we need to dive into MLS data to find pockets of strength. Look for regions with positive property index returns, especially in high-yield niches like manufactured housing. Getting a handle on these global trends helps you understand the larger forces shaping your local investment.

This data-first approach helps you sidestep markets built on hype and zero in on those with real, sustainable growth. For a deeper dive, check out our guide on the best cities to invest in rental property, where we break down specific locations using these exact principles.

Using Modern Tools for Market Analysis

Trying to gather all this data manually—sifting through census reports, economic statements, and local news—is a Herculean effort. It’s just not practical anymore. This is where modern investment platforms change the game.

Tools like Property Scout 360 pull in data from over 800 MLS regions, letting you screen and compare entire markets based on the criteria that actually matter. You can instantly find cities with that perfect blend of job growth, population trends, and favorable price-to-rent ratios. What used to take weeks of painstaking research can now be done in minutes, allowing you to make decisions based on hard data, not just a gut feeling.

Finding Deals Before They Hit the Market

Let's be honest: the best investment properties rarely have a "For Sale" sign in the yard. While everyone else is scrolling through Zillow and the MLS, the truly profitable deals are happening behind the scenes. If you want to find properties that generate real returns, you have to get out of the mainstream and go where the competition isn't—off-market.

This means you stop passively waiting for deals to appear and start actively building a system that brings them to you. It's about forging relationships and using proven tactics to find opportunities before they're public knowledge. This is what separates the pros from the hobbyists.

Build Your Local Deal Network

Your first step is to assemble a team of local experts—the people who hear the whispers and rumors long before a property is officially listed. They are your eyes and ears on the ground.

You absolutely need these people in your corner:

- Investor-Friendly Real Estate Agents: You're not looking for just any agent. You need one who lives and breathes investment properties. They understand cap rates, know the local rental market inside and out, and often have a pocket full of listings they haven't put on the market yet.

- Wholesalers: These are the hustlers of the real estate world. They specialize in finding beat-up, undervalued properties, getting them under contract, and then passing that contract on to an investor like you for a fee. Getting on a few good wholesalers' buyers lists can feel like striking gold.

- Property Managers: Who knows more about tired landlords than their property manager? These folks are on the front lines, dealing with maintenance headaches and tenant issues. They know exactly which of their clients are fed up and ready to sell.

Building these relationships doesn't happen overnight. You have to prove you're a serious buyer. Give them your exact criteria and be ready to act decisively when they bring you a deal that fits. Soon, you'll be the first person they call. For a deep dive on this, check out our guide on creating a consistent real estate deal flow.

Proactive Sourcing Methods

Networking is crucial, but you can also take matters into your own hands. One of the most classic and effective tactics is "driving for dollars." It’s exactly what it sounds like. You get in your car and drive through neighborhoods you're targeting, looking for properties that scream "neglect."

Keep an eye out for signs like:

- Lawns that look more like a jungle

- Boarded-up windows or peeling paint

- Mail and newspapers piling up on the porch

- An overall look of abandonment

These are visual cues that often point to a distressed or absentee owner—someone who might be very motivated to sell quickly and without hassle. Once you find a property, a quick search of public records can give you the owner's details so you can reach out directly. It’s a powerful way to unearth opportunities no one else even knows exist.

Off-market sourcing isn't just about finding properties; it's about finding motivation. A seller who isn't under pressure is going to hold out for top dollar. But a seller facing foreclosure, dealing with a difficult inheritance, or just plain tired of being a landlord is often willing to negotiate.

Create a Rapid Screening System

As leads start coming in, you'll drown if you try to do a deep analysis on every single one. You need a quick, back-of-the-napkin system to weed out the duds in five minutes or less.

A great starting point is the 1% Rule. This is a simple gut check: does the gross monthly rent equal at least 1% of the purchase price? So, for a $250,000 house, you'd need to see it bringing in at least $2,500 a month in rent.

If a property clears that low bar, maybe you do a quick cash-on-cash return estimate. This kind of rapid screening is your best defense against "analysis paralysis." It keeps you focused on the deals that actually have a shot at hitting your numbers.

Running the Numbers with Confidence

A property can look perfect on paper, but if the math doesn't hold up under a microscope, it can quickly turn into a financial nightmare. This is the moment you switch from the art of finding a deal to the science of proving it's a good one. Seriously, running the numbers isn't just a suggestion—it's the single most important step you'll take to protect your capital. It's how you know you're buying a real asset, not just inheriting someone else's problems.

We're going to build a financial model from the ground up. This isn't about using a simple calculator; it's about creating a repeatable process to confirm an investment's true potential. It’s how you stop guessing and start making decisions with certainty.

Mastering the Core Financial Metrics

Before digging into a specific deal, you have to get comfortable with the three pillars of rental property analysis. Think of these metrics as the vital signs that tell you the story of a property's financial health.

- Net Operating Income (NOI): This is simply your property's total income minus all its operating expenses. NOI is huge because it shows you how much profit the property generates on its own, before you even factor in your mortgage payment.

- Capitalization Rate (Cap Rate): You get this by dividing the NOI by the property's purchase price. The cap rate gives you the unleveraged rate of return, making it the perfect tool for comparing the relative value of different properties in the same market.

- Cash-on-Cash Return: Now, this is the one that really hits home. It measures the annual cash flow you pocket divided by the total cash you actually invested (your down payment, closing costs, and initial repairs). It answers the most critical question: "How hard is my own money working for me?"

For a complete walkthrough of these calculations, check out our detailed guide on how to perform a thorough real estate investment property analysis.

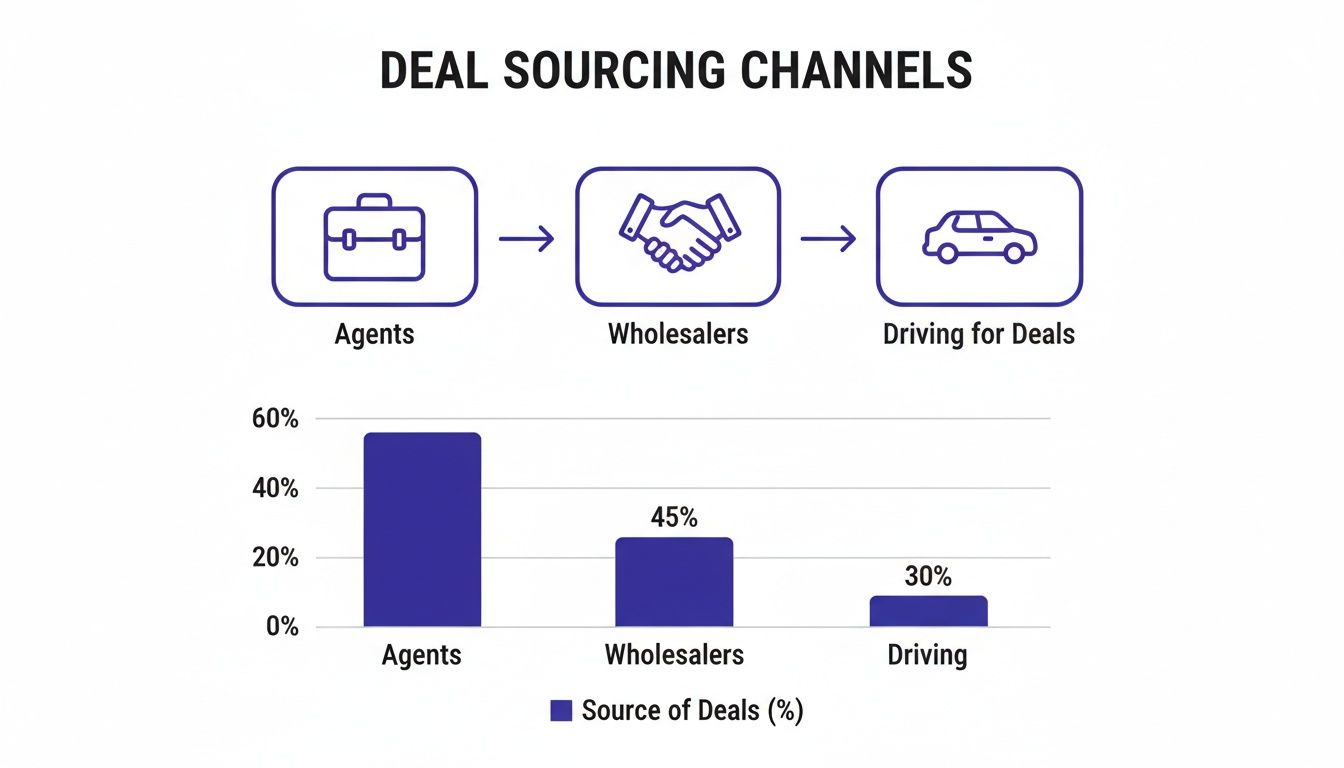

Of course, before you can even run the numbers, you have to find the deal. The chart below shows where most investors are finding their properties.

As you can see, a balanced approach that combines agent relationships with more proactive methods tends to create the most consistent deal flow.

Building a Realistic Financial Model

Alright, let's get practical and analyze a sample deal: a $300,000 single-family home. The single biggest mistake I see new investors make is underestimating expenses. Your analysis absolutely must account for the hidden costs that will inevitably eat into your profits.

A property's true performance is revealed in its expenses. Forgetting to budget for capital expenditures like a new roof or HVAC system is the single fastest way to turn a cash-flowing property into a money pit. Always buffer your numbers.

Let's break down the real income and expenses for our example property:

- Gross Rental Income: We'll assume $2,500/month, which is $30,000/year.

- Vacancy (5%): Budget $1,500/year for the inevitable gaps between tenants.

- Property Taxes: Let's say $3,600/year.

- Insurance: A standard policy might run $1,200/year.

- Repairs & Maintenance (8%): Set aside $2,400/year for the small stuff.

- Capital Expenditures (5%): Budget another $1,500/year for the big-ticket items.

- Property Management (10%): Account for $3,000/year, even if you plan to self-manage at first. Your time is valuable.

With this detailed breakdown, we have a much clearer, more realistic picture of the property's financial standing.

The Power of Financing Scenarios

Your loan is the most powerful lever you can pull to change an investment's outcome. The terms of your financing—the down payment, interest rate, and loan duration—can dramatically alter your monthly cash flow and overall return. This is truer than ever in today's market.

To confidently run the numbers on a potential investment property, mastering Net Present Value (NPV) calculations is a critical skill for evaluating long-term profitability.

Let’s see how different financing options impact our $300,000 property.

Financing Impact on a $300,000 Investment Property

This table shows just how much your loan structure can affect your bottom line. We'll compare a few common scenarios, assuming closing costs are around $9,000 and the interest rate is 6.5%.

| Metric | Scenario A 20% Down 30-Yr Fixed | Scenario B 25% Down 30-Yr Fixed | Scenario C 25% Down 15-Yr Fixed |

|---|---|---|---|

| Down Payment | $60,000 | $75,000 | $75,000 |

| Loan Amount | $240,000 | $225,000 | $225,000 |

| Monthly P&I (@6.5%) | $1,517 | $1,422 | $2,087 |

| Annual Cash Flow | $1,596 | $2,736 | -$5,144 |

| Total Cash Invested | $69,000 | $84,000 | $84,000 |

| Cash-on-Cash Return | 2.31% | 3.26% | -6.12% |

The numbers don't lie. Scenario B clearly provides the best balance of positive monthly cash flow and a solid return on the cash you invested.

While the 15-year mortgage in Scenario C builds equity much faster, it kills your cash flow, putting you in the red every single month. For a buy-and-hold investor, that's a risky game to play. By modeling these scenarios, you've just transformed a hopeful guess into a calculated business decision.

Protecting Your Investment with Due Diligence

So, the numbers look good on paper, the neighborhood checks out, and you're starting to feel like you've found a winner. This is the moment where the real work begins. This final stage—due diligence—is your last and most important line of defense before you sign on the dotted line. Think of it as the investigative phase that separates a smart, calculated investment from a costly mistake.

This is far more than just kicking the tires. It's a deep dive into the property's physical condition and financial history, designed to uncover any expensive surprises hiding in plain sight. I’ve seen countless investors get burned by skipping this step, turning a promising asset into a money pit.

The Physical Inspection Checklist

A professional home inspection is non-negotiable, period. But your job isn't just to hire someone; you need to be an active part of the process. Show up, walk the property with the inspector, ask a ton of questions, and make sure you understand what their findings actually mean for your bottom line.

Your main goal here is to sniff out major capital expenditures that could wreck your budget. Pay close attention to the big-ticket items:

- The Roof: How many years does it have left? Are there curled shingles, dark spots from water damage, or soft spots underfoot? A new roof can easily run you $10,000-$20,000, which is a gut punch of an expense if you weren't expecting it.

- The Foundation: Walk the perimeter and the basement. Look for significant cracks (especially horizontal ones), signs of water intrusion, or doors and windows that stick. Foundation problems are some of the scariest and most expensive repairs you can face.

- HVAC System: Check the manufacturing date on the furnace and AC unit. A typical system lasts about 15-20 years. Knowing where it is in that lifecycle is critical for planning future replacement costs.

- Electrical and Plumbing: Outdated wiring like knob-and-tube or old galvanized plumbing can be more than just a repair bill; they can make it difficult or expensive to get insurance.

These core systems are the heart of the property. A sudden failure in any of them can instantly wipe out years of your hard-earned cash flow.

Due diligence is where you verify the story the seller is telling you. If the proforma says the deal is a home run but the inspection reveals a crumbling foundation, you have to trust what you see, not what you hoped for. Remember, walking away from a bad deal is a win.

The Financial and Legal Audit

Once you have a clear picture of the property's physical health, it's time to put its finances under the microscope. You need to verify every single number the seller has given you to make sure the income and expenses are real.

This audit means digging into the paperwork:

- Scrutinize Lease Agreements: Get a copy of every lease. Confirm the rental rates, lease end dates, and security deposit amounts. Are the tenants paying what the seller claims? Look for patterns of late payments—this is a huge red flag.

- Verify Expense Reports: Don't just take their word for it. Ask for the last 12-24 months of actual utility bills, property tax statements, and insurance policies. Compare the real costs to what was advertised to find any "optimistic" numbers.

- Review Tax Records: Pull the public tax records to confirm the assessed value and the annual tax bill. You also want to check for any pending tax appeals or special assessments that could jack up your holding costs.

- Perform a Title Search: Your title company will handle this, but it’s absolutely essential. This process ensures the seller actually has the legal right to sell the property and that there are no hidden liens or claims from contractors, ex-spouses, or anyone else.

The motto here is "trust, but verify." You're making sure the asset you’re buying performs exactly as advertised. If a seller is hesitant to hand over these documents, you should be very, very suspicious.

Navigating Negotiations and the Market Climate

The discoveries you make during due diligence aren't just a pass/fail test—they are your most powerful negotiation leverage. Finding out the property needs a $15,000 new roof doesn't automatically kill the deal. It gives you a concrete reason to go back to the seller and ask for a price reduction or a credit at closing.

Of course, your negotiating power depends on the current market. Recent reports point to a real estate cycle that's at a turning point, with prices stabilizing and interest rates easing up. For investors, this shift means sellers might be standing firmer on their prices. As investment activity in the Americas is projected to increase, the competition is heating up, which makes your due diligence even more critical for landing a solid deal. You can get a better sense of the current commercial real estate outlook from Deloitte.

Be strategic with your requests. Focus on the big, unexpected issues, not minor cosmetic things you can fix yourself. The goal is to land on a fair price that reflects the property's true condition, ensuring the deal still works for you after you account for the necessary repairs.

And if the seller won't negotiate on major problems? Be prepared to walk. The best deal you'll ever make is the bad one you didn't buy.

Answering the Tough Questions

Even the most well-thought-out strategy runs into real-world questions. When you're in the trenches looking for a deal, you need clear, straightforward answers to get past common roadblocks and make decisions you can stand by.

Let's tackle a few of the most frequent questions that pop up when you're on the hunt. Getting these right is what separates theory from actual, successful investing.

What’s a “Good” Cap Rate, Anyway?

I get this one all the time. The truth is, there’s no magic number. A "good" cap rate is completely relative to the market, the property type, and your goals. It’s a tool for comparison, not a universal benchmark of quality.

Think of it this way: a cap rate tells a story about risk and potential.

In a hot, stable market like Austin or Denver, a 4-5% cap rate might be fantastic. Why so low? Because that rate implies lower risk, tons of tenant demand, and a high likelihood of appreciation down the road. Investors there are willing to trade a little bit of immediate cash flow for long-term stability and growth.

On the other hand, if you're looking at a property in a smaller, less certain market, you should demand a higher return for the risk you're taking on. You’d want to see something in the 8-10% range, maybe even higher. That extra cash flow is your compensation for dealing with potential economic shifts or a smaller pool of tenants.

The smartest way to use the cap rate is to compare apples to apples. If most duplexes in a specific neighborhood are trading at a 7% cap rate, and you find one listed at 4.5%, you've got to dig deeper. Is it wildly overpriced, or is there some hidden upside the market isn't seeing?

How Much Cash Do I Actually Need?

The down payment is just the tip of the iceberg. New investors often make the mistake of focusing solely on the 20-25% down required for most conventional investment loans, and it’s a costly error. To really understand what you need in the bank, you have to account for three separate buckets of money.

Let’s walk through a $300,000 property to see what this looks like in practice:

- Down Payment (20%): This is your ticket to the game. For our example, that’s $60,000.

- Closing Costs (2-5%): Don't forget all the fees for the lender, appraisal, title search, and more. Budget another $6,000 to $15,000 for these.

- Cash Reserves (3-6 months): This is non-negotiable and, frankly, the most overlooked fund. You absolutely need 3-6 months of the property’s total expenses—mortgage, taxes, insurance, and estimated repairs—sitting in a separate account. This is your safety net. It's what turns a surprise HVAC failure from a financial crisis into a manageable problem.

So, for that $300,000 property, you really need to have $75,000 to $90,000 in liquid cash to be properly capitalized and sleep well at night.

Should I Go for a Turnkey Property or a Fixer-Upper?

This really boils down to an honest assessment of your personal resources: your cash, your time, and your stomach for chaos. Each path offers a completely different journey.

A turnkey property is all about immediate cash flow with minimal upfront hassle. It’s a fantastic way for new investors to learn the ropes of being a landlord without the stress of a major renovation. It’s also the go-to for remote investors who can't be on-site to manage contractors. The trade-off? You’ll pay a premium for the convenience and have less opportunity to create instant equity.

A fixer-upper, on the other hand, is the classic "BRRRR" method play. The whole point is to "force" appreciation through smart renovations, which can lead to a much bigger ROI. But let's be clear: this path is anything but passive. It demands a ton of your time for project management, a solid understanding of construction costs, and a hefty cash reserve for the inevitable surprises you'll find behind the drywall.

My advice for most beginners? Start with a turnkey property or one that only needs light cosmetic touches. It's the smarter, safer way to get your first win in real estate investing.

Ready to stop guessing and start analyzing deals with real confidence? Property Scout 360 gives you the tools to run the numbers on any U.S. property in minutes, not hours. Find your next great investment and build your portfolio on a foundation of solid data.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.