Is Rental Property a Good Investment an ROI and Cash Flow Guide

Is rental property a good investment? Discover how to analyze ROI, cash flow, and key metrics to build wealth with this data-driven guide for investors.

Let's get right to it. Is rental property a good investment? The short answer is yes, it absolutely can be. But it's not like winning the lottery.

Success in real estate investing comes down to smart analysis, knowing your market, and—most importantly—understanding the numbers that drive your returns. This is a business, not a get-rich-quick scheme. When you treat it like one, you can build serious, long-term wealth through four distinct but interconnected pillars.

How Rental Properties Build Real Wealth

When you ask if a rental is a good investment, you have to look past the monthly rent check. A great property is a powerful, multi-faceted wealth-building engine. It's working for you in several different ways at once, which is something that sets real estate apart from other assets.

Think about it. With stocks, you're generally just looking at appreciation and maybe some dividends. Real estate offers a much more robust framework for financial growth. This unique combination of immediate income, long-term equity growth, and tax advantages is what pulls so many successful investors into the game. Understanding how these pieces fit together is the first step toward making a smart decision.

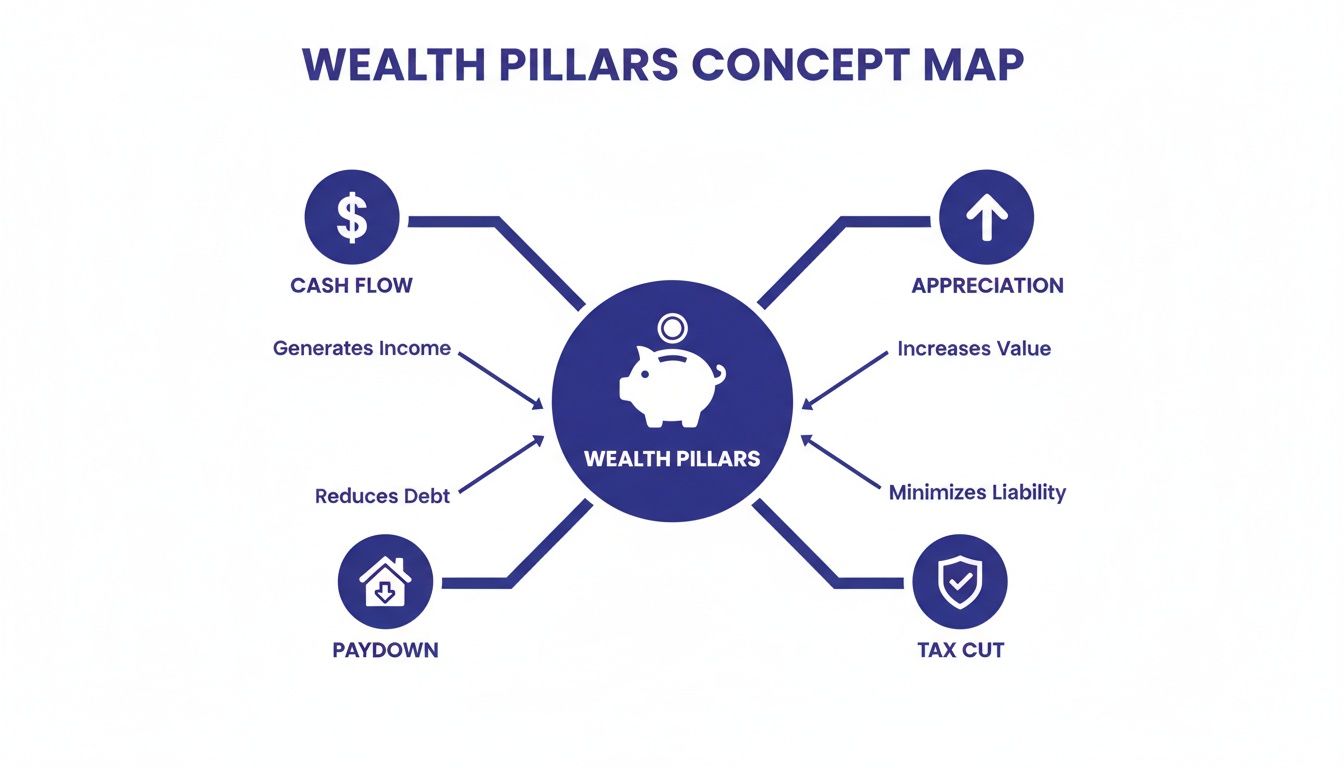

The Four Pillars of Real Estate Investing

To really see how a single rental property creates wealth, you need to break it down into four core components. Each one is a critical part of your total return. Let's dig into what I call the "four pillars."

These are the primary ways your investment property makes you money, often all at the same time.

The Four Pillars of Rental Property Wealth

Here's a quick overview of how each pillar contributes to your financial growth.

| Wealth Pillar | How It Works for You | Key Metric to Watch |

|---|---|---|

| Cash Flow | This is the money you pocket each month after every single expense is paid—mortgage, taxes, insurance, repairs, you name it. | Net Operating Income (NOI) |

| Appreciation | The property's value goes up over time due to market demand and inflation. This builds your net worth silently in the background. | Comparative Market Analysis (CMA) |

| Loan Paydown | Your tenant's rent check pays down your mortgage every month, building your equity for you. It's a powerful form of "forced savings." | Loan Amortization Schedule |

| Tax Benefits | The government offers major tax breaks for investors, like deducting mortgage interest, expenses, and even the property's depreciation. | Depreciation & Expense Tracking |

Each pillar plays a distinct role, but they work together to create a powerful financial outcome over the long haul.

The visual below ties all four of these concepts together, showing how they form the foundation of building wealth through real estate.

This synergy between cash flow, appreciation, loan paydown, and tax advantages is what makes rental properties such a compelling investment. Of course, finding a market where these factors align is key. For more on that, take a look at our guide on the best cities to invest in rental property.

Next, we’ll explore the key metrics you need to master to evaluate any potential deal.

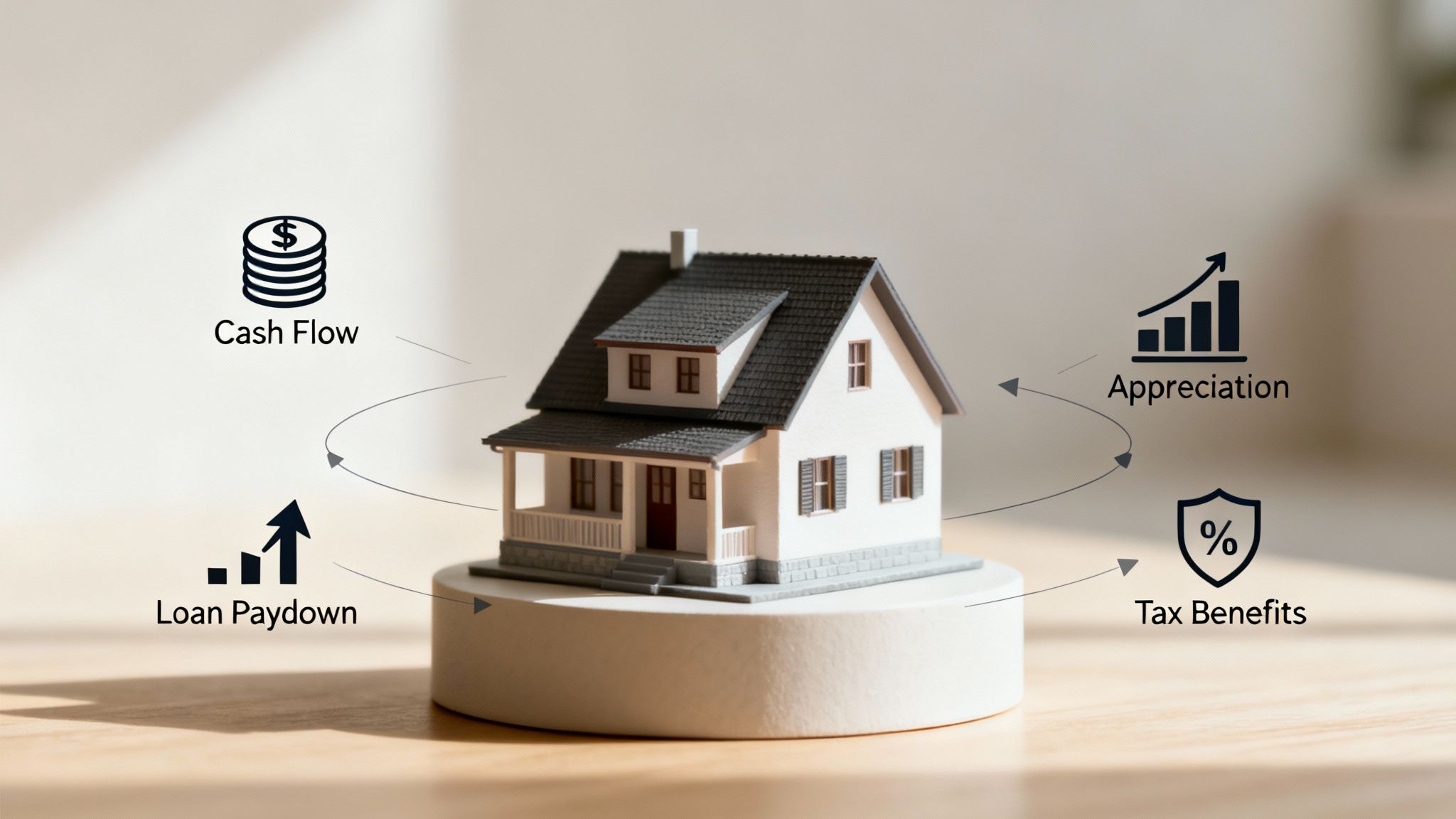

Understanding How Rental Properties Build Wealth

To really figure out if a rental property is a good investment, you have to look past the monthly rent check. A great property is like having a star employee who works for you 24/7, creating value in four different ways. It’s this powerful combination that sets real estate apart from most other investments.

Think of it like this: a single asset is generating returns from multiple sources all at once. Stocks grow when their price goes up and maybe pay a small dividend, but a good rental property is actively building your wealth on several fronts simultaneously. Let's break down these four financial "jobs."

Pillar 1: Cash Flow

This one’s the most obvious. Cash flow is simply the money left in your pocket after you’ve collected rent and paid all the bills for the month. Those bills include the mortgage, property taxes, insurance, repairs, and any fees for a property manager.

Let's say your tenant pays $2,500 in rent. After you cover $2,100 in total expenses, you’re left with $400. That’s your cash flow. It’s the immediate, tangible reward for owning the property—a steady income stream that can beef up your savings, pay down other debts, or get rolled into your next investment.

Pillar 2: Appreciation

Appreciation is the silent partner in your investment, quietly building wealth in the background. It's the increase in your property's market value over time. While nothing is guaranteed, real estate has a long history of appreciating thanks to inflation, population growth, and simple supply and demand in good locations.

A house you buy for $300,000 today could easily be worth $400,000 in ten years. That $100,000 gain is pure equity added to your net worth, and it happened without you having to do much at all. For many investors, this long-term growth is where the real magic happens.

The Power of Compounding Returns

Here’s where it gets interesting. You can take the cash flow from Pillar 1 and reinvest it into the property—say, by renovating a kitchen. That improvement can increase the property's value (appreciation) and justify a higher rent, which in turn boosts your future cash flow. It's a powerful wealth-building cycle.

Pillar 3: Loan Paydown

This might be the most underrated part of the whole deal. Every single month, your tenant is the one paying your mortgage. A chunk of that payment goes directly toward the loan's principal, which means your ownership stake—your equity—grows automatically.

Essentially, your tenant is buying the asset for you. It’s a forced savings account that someone else funds. You're using the bank's money (the loan) and your tenant's money (the rent) to build your own wealth. This is the classic definition of leverage, and it’s why real estate can deliver such fantastic returns.

Pillar 4: Tax Benefits

Let’s be honest, this is a huge one. The U.S. tax code is surprisingly friendly to real estate investors, offering up some serious advantages that can supercharge your overall returns. The government essentially rewards you for providing housing.

Here are a couple of the heaviest hitters:

- Expense Deductions: You can write off almost every cost tied to owning and managing the property. We're talking mortgage interest, property taxes, insurance, repairs, marketing, and property management fees.

- Depreciation: This is a game-changer. The IRS lets you deduct a portion of your property's value each year for "wear and tear," even if the property is actually going up in value. It's a "phantom" deduction that can dramatically lower your taxable income, sometimes even to zero.

These four pillars—cash flow, appreciation, loan paydown, and tax benefits—all work together, turning a single property into a financial engine. While rental properties are just one option, they offer a unique combination of benefits. It's always smart to diversify, and you might want to explore a range of other top income-generating investments as well.

Key Financial Metrics Every Investor Must Master

If you really want to know if a rental property is a good investment, you have to learn to speak the language of real estate finance. Forget gut feelings. Successful investors don't guess—they calculate. The numbers always tell the real story of a property's potential.

Think of these core metrics as your toolkit. They're what you'll use to dissect any deal, compare different properties, and ultimately, protect your hard-earned money. Mastering them is what separates a hopeful homebuyer from a confident, strategic investor.

Net Operating Income: The Foundation of Value

Before you can figure out any kind of return, you need to know your Net Operating Income (NOI). This is arguably the most important number for understanding a property’s raw profitability.

NOI is simply all the income the property brings in, minus all the day-to-day operating expenses. The key thing to remember is that it does not include your mortgage payment. This is intentional. It lets you judge the property on its own merits, separate from whatever financing you might arrange.

Net Operating Income (NOI) Formula

Gross Rental Income - Operating Expenses = Net Operating Income (NOI)

- Gross Rental Income: The total rent you could collect in a year.

- Operating Expenses: Everything from property taxes and insurance to maintenance, management fees, and a fund for when the unit is empty (vacancy).

Think of NOI as the property's "annual salary." A healthy, positive NOI means you're looking at a solid business that can stand on its own two feet.

Capitalization Rate: For Comparing Apples to Apples

The Capitalization Rate, or Cap Rate, is your best friend when you need to quickly compare different investment opportunities. It gives you a clean, unleveraged rate of return, showing what the property earns based purely on its income and price.

By taking the mortgage out of the picture, the cap rate gives you an unbiased look at how efficiently a property turns its price tag into pure profit.

Capitalization Rate (Cap Rate) Formula

Net Operating Income (NOI) / Property Purchase Price = Cap RateFor example, if a property has an NOI of $12,000 and you bought it for $250,000, your cap rate is 4.8% ($12,000 / $250,000).

A higher cap rate can mean a better return, but it often comes with more risk. A lower cap rate might suggest a safer bet in a more stable, premium market. There’s no magic number for a "good" cap rate—it's all about the local market and what level of risk you're comfortable with.

Cash-on-Cash Return: Your True Pocket Return

While the cap rate is fantastic for comparing deals, the Cash-on-Cash Return is what really matters to you. It tells you the exact return you're making on the actual cash you pulled out of your pocket to buy the property.

This metric is incredibly powerful because it brings your financing back into the equation. It answers the one question every investor has: "For every dollar I put in, how many cents am I getting back each year?" Most savvy investors I know aim for an 8-12% cash-on-cash return, at a minimum.

Cash-on-Cash Return Formula

Annual Pre-Tax Cash Flow / Total Cash Invested = Cash-on-Cash Return

- Annual Cash Flow: This is your NOI after you've paid your annual mortgage payments.

- Total Cash Invested: Your down payment, all closing costs, and any money spent on initial repairs or upgrades.

This is the number that tells you if an investment truly works for your personal financial situation.

Total Return on Investment: The Big Picture

Finally, the Return on Investment (ROI) gives you the most complete picture of how your investment is performing. It doesn't just look at cash flow; it also factors in the other ways real estate builds wealth, like appreciation and the equity you build as you pay down your loan.

ROI adds everything up to show you the total financial benefit you've gained compared to what you put in. To get a better handle on all the moving parts, take a look at our complete guide on calculating rental property ROI.

The historical performance of real estate is nothing short of impressive. One landmark 145-year study found that rental properties delivered an average annual return of 7.05%, which actually edged out stocks at 6.89% over the same long haul. It’s a powerful reminder of how effective real estate can be as a long-term wealth-building machine.

Each of these metrics tells you a different piece of the story. When you use them together, you get a 360-degree view, giving you the confidence to make smart, data-driven decisions.

Comparing Real Astate and Stock Market Investing

When people wonder if a rental property is a good investment, what they’re usually asking is, "Is it a better investment than the stock market?" It's the classic showdown: the tangible, brick-and-mortar asset versus the liquid, digital one.

Let's break down this age-old debate with a simple story.

Imagine two friends, Alex and Ben, each with $50,000 ready to invest. Ben plays it safe and puts his entire $50,000 into an S&P 500 index fund. His investment is straightforward—it grows or shrinks based on how the market performs that day.

Alex, on the other hand, takes a different route. He uses his $50,000 as a 20% down payment to buy a $250,000 rental property. Right out of the gate, Alex is controlling a quarter-million-dollar asset with the exact same starting cash as Ben. This is the superpower of real estate: leverage.

The Power of Leverage in Real Estate

In simple terms, leverage means using other people's money—in this case, the bank's mortgage—to buy a much larger asset. While Ben’s $50,000 in stocks can only grow on its own, Alex’s $50,000 is a key that unlocks a $250,000 asset. This magnifies his potential returns in a way stocks just can't.

Let’s see how this plays out with appreciation. Say both the stock market and the local housing market grow by a modest 5% in one year:

- Ben’s S&P 500 fund earns $2,500 (5% of his $50,000).

- Alex’s property value grows by $12,500 (5% of the property's $250,000 value).

Just from appreciation, Alex made 25% on his original cash investment. That’s the magic of leverage. But it doesn't stop there. Every single month, his tenants are paying rent, which covers his mortgage and slowly builds his equity. Essentially, someone else is buying the asset for him.

Cash Flow Versus Dividends

Another huge difference is how you get paid. Stock portfolios might throw off some dividends, but they're often small and can be slashed without warning if a company hits a rough patch.

A well-chosen rental property, however, is a cash-generating machine. After you've paid the mortgage, taxes, insurance, and set aside money for repairs, the leftover profit is your cash flow. It's a predictable stream of income that hits your bank account month after month, regardless of what the market is doing.

Long-Term Performance: A Real-World Test

Over the long haul, real estate has more than held its own. Take an investor who put a $34,000 down payment on an average Phoenix home back in 2000. By 2025, their equity had ballooned to roughly $460,000. After factoring in all costs and adjusting for inflation, that property delivered a real internal rate of return of about 5.0% per year. That's right in line with the S&P 500's 5.1% real return over the same 25-year stretch. You can dive into the full 25-year inflation-adjusted return analysis to see the numbers for yourself.

Control, Volatility, and Liquidity

Of course, no investment is perfect. Stocks have a clear advantage in liquidity—you can sell them with a click of a button. Selling a house is a much bigger undertaking that can take weeks or even months.

But what real estate lacks in liquidity, it makes up for in control. You can't call up a CEO and tell them how to run their company, but you absolutely can add value to your property through smart renovations or better management. Real estate is also far less volatile. Home prices don't swing wildly from day to day like stock prices do.

At the end of the day, both are powerful tools for building wealth. But when you add up the unique advantages of real estate—leverage, consistent cash flow, loan paydown by tenants, and direct control—it's easy to see why so many successful investors swear by it for building lasting financial freedom.

Navigating the Inevitable Bumps in the Road

Let's be real for a moment. Anyone who tells you rental property investing is a "set it and forget it" path to riches is selling you a fantasy. It’s not like buying an index fund and checking it once a quarter. This is a business. And like any business, it has its share of headaches and hurdles.

But don't let that scare you off. The smartest investors I know don't have some magic ability to avoid problems. Instead, they’ve learned how to anticipate them. They build systems and create buffers to turn a potential crisis into a manageable, predictable cost. That's the mindset you need.

The Pain of an Empty Property

There's nothing worse for a landlord's bank account than a vacancy. When your property sits empty, the income stream drops to zero, but 100% of your expenses—the mortgage, property taxes, insurance—keep coming like clockwork. Every single month without a tenant is pure profit evaporating into thin air.

So, how do you fight back? It comes down to two simple things:

- Price it Right: Do your homework. See what comparable units in your neighborhood are renting for. If you get greedy and overprice your rental, you're practically inviting it to sit empty for months.

- Market Like a Pro: Don't wait until the day your tenant moves out to find a new one. Start advertising 30-60 days before the current lease is up. Great photos and a compelling description will get qualified people lined up, minimizing that gap between renters.

And remember, your absolute best defense against vacancies (and a whole lot of other problems) is a rock-solid tenant screening process. A deep dive into an applicant's credit, job history, and past rentals can save you from a world of financial pain.

The True Cost of a Bad Tenant

Think an eviction is just a hassle? Think again. Between legal fees, months of lost rent, and repairing potential damage, a single eviction can easily cost $2,500 to over $10,000. That one mistake can erase years of your hard-earned profits. This is why you never, ever skip a thorough screening.

When Things Break (and They Always Do)

It’s not a question of if your property's water heater will give out, but when. And it will almost certainly happen on a holiday weekend in the middle of the night. That's just how it works. These big-ticket repairs can absolutely demolish your cash flow if you're not ready for them.

The solution is a Capital Expenditures (CapEx) fund. It’s just a fancy name for a dedicated savings account. Every month, you skim 5-10% of the rent and stick it in this account. When you eventually need a new roof or HVAC system, the money is already there. What would have been a financial emergency becomes just another planned business expense.

The Bigger Picture: Market Swings and Legal Rules

Real estate markets don't just go up. They move in cycles. Interest rates can climb, a major local employer could shut down, or a hot market can suddenly cool off. You can’t control the economy, but you can insulate your investment. How? By focusing on properties that generate positive cash flow from day one, not just hoping for appreciation. A rental that pays for itself every month can survive almost any storm.

On top of market risks, you're stepping into a role with serious legal duties. Being a landlord isn't just about collecting a check; you have obligations that differ from state to state and city to city. For example, understanding the specific landlord responsibilities in Texas is non-negotiable if you own property there. Staying compliant isn't just good advice—it's how you protect yourself from expensive lawsuits.

How to Find and Analyze Your First Investment Deal

Theory is one thing; putting your own money on the line is a completely different ballgame. This is the moment where all the concepts we've talked about—from cash flow to cap rates—get real. Finding and analyzing your first deal isn't about getting lucky. It's about having a disciplined, repeatable system.

Think of yourself as a detective. You’re looking for clues that point to a profitable investment, sifting through dozens of listings to find the one that actually fits your financial goals. The right tools and a clear strategy can turn this overwhelming task into a confident, data-driven decision.

Setting Your Investment Criteria

Before you even glance at a listing, you need to know exactly what a "good deal" looks like for you. This goes way beyond the purchase price; it’s about the performance you expect from your investment. Without clear goals, every property seems like a possibility, and you'll quickly find yourself stuck in analysis paralysis.

Start by setting your non-negotiable targets for the key metrics:

- Target Cash-on-Cash Return: What's the minimum annual return you need on your down payment and closing costs? Many experienced investors won't look at a deal unless it’s 8% or higher.

- Minimum Monthly Cash Flow: How much money do you want in your pocket each month after all expenses are paid? Decide on a hard number, like at least $200 per unit.

- Property Type and Location: Don't try to be a jack-of-all-trades. Focus on a specific neighborhood or property type—like single-family homes or small duplexes—and become the local expert.

Think of these criteria as your personal filter. They instantly weed out properties that don't match your objectives, saving you countless hours and preventing you from chasing deals that won't move you forward.

Running the Numbers Quickly and Accurately

Once you have a shortlist of properties that meet your criteria, it’s time to put them under the microscope. This is where manual spreadsheets can really slow you down. In a competitive market, being able to analyze a deal in minutes, not hours, gives you a serious advantage.

You need to project each property's potential income and expenses to get a clear financial picture. A solid analysis must include solid estimates for property taxes, insurance, vacancy (a conservative 5-8% is standard), maintenance (budget 1% of the property value annually), and property management fees.

The real estate landscape has consistently proven its worth for investors focused on income. Over the past two decades, U.S. private real estate generated average income returns of 5.22% annually, outperforming both bonds and stocks. This makes it a powerful asset for portfolio diversification and steady cash flow. For a deeper dive, you can explore the full report on single-family rental investing.

It's also crucial to compare different financing scenarios. How does a 15-year mortgage change your cash flow compared to a 30-year loan? What happens to your monthly return if you put down a larger down payment? Running these scenarios is fundamental to understanding a deal's true potential and its risk profile. Our guide on how to analyze a rental property walks through these steps in much greater detail.

By combining clear investment goals with swift, accurate analysis, you shift from being a passive observer to an active investor—ready to spot and seize the right opportunity when it appears.

Diving Into Your Top Questions About Rental Investing

Even when you've run the numbers and everything looks good on paper, a few nagging questions can still hold you back from pulling the trigger on your first deal. That's completely normal. Let's tackle some of the most common hurdles I hear from new investors to give you that final bit of confidence.

How Much Money Do I Actually Need to Start?

This is always the first question, and the answer is usually less than people fear. The standard advice is a 20-25% down payment for a conventional investment loan, which is true. But that’s not the only way in.

A popular strategy, especially for first-timers, is "house hacking." This is where you buy a small multi-family property (like a duplex) and live in one of the units. Doing this often lets you qualify for an FHA loan, which can drop your down payment to as low as 3.5%.

So what does that look like in real dollars? On a $250,000 property, you'd need the down payment, another 2-5% for closing costs, and a safety net of three to six months' worth of expenses. All in, you could be looking at anywhere from $25,000 to $75,000 in cash, depending on the path you take.

What’s the Best Type of Property for a Beginner?

When you're just starting out, keep it simple. A single-family home or a condo is almost always the best bet. They’re just easier to wrap your head around, finance, and manage than a big, complicated apartment building.

- Single-Family Homes: These tend to attract families who stick around for a while, meaning you'll likely deal with less tenant turnover and have more predictable income.

- Condos: Yes, they have HOA fees. But those fees typically cover big-ticket items like the roof, landscaping, and exterior maintenance, which takes a lot of the management headache off your plate.

Your first goal is to learn the business without getting buried. One solid, easy-to-manage rental is a much smarter move than a complex project that stretches you too thin.

A Quick Word on Management

No matter what you buy, you have to decide: will you manage it yourself or hire a pro? A property manager will typically cost you 8-12% of the monthly rent, but they handle the tenant calls, the midnight plumbing emergencies—everything. For new investors or anyone who lives far from their rental, that fee is often money well spent to buy back your time and sanity. It’s a huge factor in whether a property is a good investment for your life.

What Are the Biggest Tax Perks I Should Know About?

Real estate comes with a ton of tax advantages, but two are absolute game-changers for your bottom line. First, you get to deduct nearly every expense associated with the property. We're talking mortgage interest, property taxes, insurance, repairs—the works.

The second one is the real magic: depreciation. The IRS lets you claim a "paper loss" each year for the gradual wear and tear on the building. This is a non-cash deduction, meaning you get the tax break even if your property is making money hand over fist and going up in value. It's one of the most powerful wealth-building tools in all of real estate.

Ready to stop guessing and start analyzing? Property Scout 360 eliminates the spreadsheets and gives you instant, professional-grade investment analysis on any U.S. property. Run scenarios, project cash flow, and find deals that match your goals in minutes, not weeks. Make your next investment your best investment by visiting https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.