What Is Cash Flow in Real Estate Explained

Understand what is cash flow in real estate with our guide. Learn how to calculate, analyze, and increase profits on your rental property investments.

When you get down to it, cash flow in real estate is simply the money left in your pocket after you’ve collected the rent and paid all the bills. It’s the real, tangible profit you earn each month.

Think of it as your property’s monthly paycheck. If that paycheck is a positive number, you’re making money. If it’s negative, you’re dipping into your own funds to keep the property afloat.

What Is Real Estate Cash Flow Really

It's easy to get caught up in the excitement of appreciation—the idea that your property's value will climb over time. While that's a fantastic long-term goal, appreciation doesn't help you pay the mortgage or fix a leaky faucet today.

Cash flow, on the other hand, is the lifeblood of a healthy rental investment. It’s the consistent, predictable income that covers all your costs and actually builds your wealth month by month. This reliable income stream is what turns a property from a speculative bet into a true investment.

Without positive cash flow, just one major repair or a month of vacancy can force you to pay out-of-pocket, quickly turning your asset into a liability.

Positive vs. Negative Cash Flow

Every real estate investor needs to master one simple concept: the difference between positive and negative cash flow. It's a straightforward idea with huge consequences for your financial success.

Positive Cash Flow: This is the investor's dream. It’s when your rental income is higher than all your operating expenses and mortgage payments combined. That leftover money is your profit.

Negative Cash Flow: This is the red flag. It happens when your total expenses exceed the rent you collect. You’re now responsible for covering the difference yourself, which is a recipe for financial stress.

The core purpose of a rental property is to generate more income than it costs to own. Positive cash flow proves your investment is working for you, not the other way around.

Why Cash Flow Matters More Than You Think

A property with strong, consistent cash flow is the bedrock of a successful real estate portfolio. It gives you the financial cushion to handle big-ticket items—like a new roof or an HVAC replacement—without derailing your entire financial plan.

Historically, the income component has been responsible for about 78% of long-term returns in global commercial real estate. You can learn more about these real estate return drivers to see just how critical it is. Ultimately, cash flow is the engine that builds true, lasting wealth, not just the hope of future appreciation.

How to Calculate Cash Flow Step by Step

Forget trying to decipher complex spreadsheets. Calculating a property's cash flow is actually pretty straightforward once you get the hang of the basic components. It really just boils down to one simple idea: start with all the money coming in, then subtract all the money going out.

Following this step-by-step process gives you a reliable framework you can use to analyze any deal that crosses your desk. It helps you move past wishful thinking and land on a real number that tells you if a property is a winner or a dud.

Start with Gross Rental Income

First things first, you need to figure out your Gross Rental Income (GRI). This is simply the absolute maximum rent you could collect in a year, assuming you have a tenant paying on time, every single month, with zero downtime. It's your best-case scenario.

For example, if you've got a single-family home that rents for $2,000 per month, your Gross Rental Income is:

$2,000 (monthly rent) x 12 (months) = $24,000 (GRI)

Think of this as your starting line. It's the top-line number from which all your costs will be deducted.

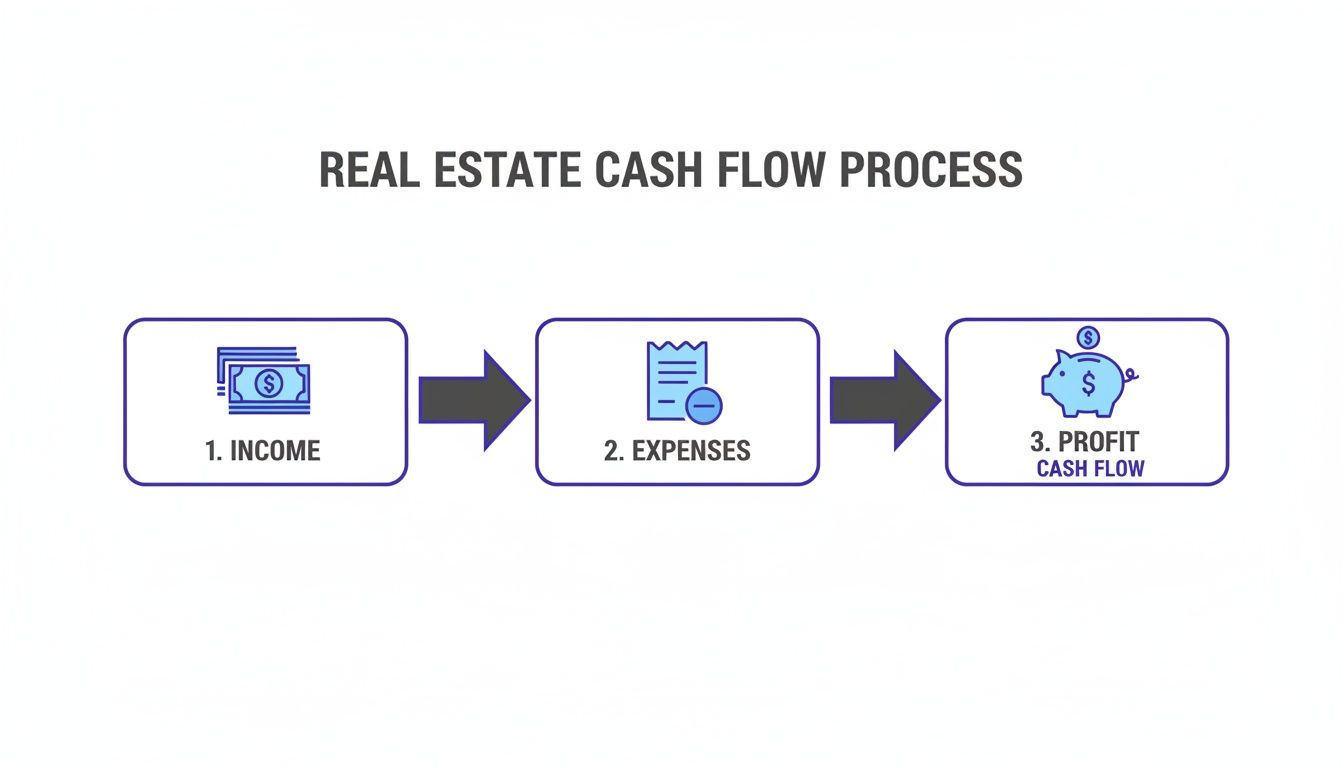

This simple diagram shows you how you get from that total income to the actual profit you'll see.

As you can see, the gross income gets chipped away by expenses, leaving you with the net profit—your cash flow—at the very end.

Subtract Vacancy and Operating Expenses

Now, let's get real. No property stays rented 365 days a year, year after year. Tenants move out, and it takes time to find new ones. That's why you have to account for vacancy. A conservative and safe estimate is usually 5-10% of your GRI.

In our example, a 5% vacancy rate on $24,000 comes out to $1,200 for the year.

Next, you have to subtract all your Operating Expenses. These are all the non-mortgage costs of keeping the lights on and the property in good shape.

Common operating expenses include:

- Property Taxes: What the city or county charges you annually.

- Insurance: Your landlord or hazard insurance policy is a must-have.

- Repairs & Maintenance: Things break. Always budget for them. A good rule of thumb is 5-10% of the GRI.

- Property Management Fees: If you hire a pro to handle the day-to-day, they'll typically charge 8-12% of the monthly rent.

- Utilities: Any bills you're responsible for, like water, sewer, or trash.

Once you subtract vacancy and these operating costs from your GRI, you're left with a crucial number: Net Operating Income (NOI).

Key Insight: Net Operating Income (NOI) is the purest measure of a property's profitability. It shows you how much money the asset itself generates, completely separate from any loans. This makes it the perfect metric for comparing the performance of two different properties on an apples-to-apples basis.

Deduct Your Debt Service

The last piece of the puzzle is your mortgage. You need to subtract your total loan payments for the year, often called debt service. This includes both the principal and the interest you pay to the bank.

Let's say the annual mortgage payment for our example property is $13,200 (which works out to $1,100 per month).

Now we can put it all together:

- Gross Rental Income: $24,000

- Less Vacancy (5%): -$1,200

- Less Operating Expenses (taxes, insurance, etc.): -$6,000

- Equals Net Operating Income (NOI): $16,800

- Less Debt Service (Mortgage): -$13,200

- Equals Final Annual Cash Flow: $3,600

That breaks down to $300 per month in positive cash flow. This is the real, spendable profit you actually get to put in your pocket after everyone else has been paid.

Going Beyond Cash Flow With Key Metrics

Seeing a positive number on your monthly cash flow statement is a great start, but it’s just that—a start. It doesn't tell you the whole story about your investment's performance. To really get under the hood and see what’s going on, seasoned investors use a handful of key metrics.

Each one offers a different lens to look through, helping you spot risks and opportunities that a simple cash flow number might hide. This is how you move from just asking "Does it make money?" to making truly strategic, data-backed decisions.

Cash-on-Cash Return: Your True ROI

The Cash-on-Cash (CoC) Return cuts straight to the point. It answers the one question every investor has: "For every dollar I put in, what am I getting back each year?" It’s a direct measure of how hard your actual invested capital is working for you.

Think about it this way. If you stuck $100 in a savings account and got $5 in interest after a year, your return is 5%. Real estate works the same way. The formula is simply:

Annual Pre-Tax Cash Flow / Total Cash Invested = Cash-on-Cash Return

Your "Total Cash Invested" isn't just the down payment. It’s everything you paid out-of-pocket to get the deal done—closing costs, initial repairs, the works. This is why CoC is so powerful; it zeroes in on the return on your money, not the bank's.

Cap Rate: Comparing Apples to Apples

Next up is the Capitalization Rate, or Cap Rate. This is your go-to metric for comparing different properties against each other, even if they have completely different financing structures. It strips away the loan details to reveal the raw income-generating potential of the asset itself.

The formula looks like this:

Net Operating Income (NOI) / Current Market Value = Cap Rate

Because the Cap Rate ignores your mortgage, it lets you evaluate a property purely on its own merits. This makes it a fantastic tool for quickly stacking up multiple potential deals. A higher Cap Rate often signals a higher potential return, but it can also mean more risk. To really master this concept, check out our deep dive into what is cap rate in real estate.

The 1% Rule: A Quick Litmus Test

Finally, we have the 1% Rule. This isn't a deep analytical tool, but rather a quick-and-dirty filter to see if a property is even worth your time. It’s a simple rule of thumb: the gross monthly rent should be at least 1% of the purchase price.

So, for a $200,000 house, you'd want to see it renting for at least $2,000 a month. If it doesn't meet this basic threshold, there's a good chance it will struggle to cash flow once you factor in all the expenses. This simple check helps you weed out duds early, so you can focus your energy on deals that actually have a shot. Of course, a full financial picture requires understanding accounts payable and accounts receivable to manage the property's books effectively.

Comparing Investment Analysis Metrics

To put it all together, these metrics aren't in competition with each other; they're members of the same team, each playing a different position. Here’s a quick breakdown of what each one tells you and when to use it.

| Metric | What It Measures | Best Use Case |

|---|---|---|

| Cash-on-Cash Return | The annual return on your actual out-of-pocket cash investment. | Evaluating the efficiency of your capital and comparing deals with different financing. |

| Cap Rate | The property's unleveraged annual return based on its income and market value. | Quickly comparing the raw profitability of different properties, regardless of loans. |

| The 1% Rule | A rough guideline to see if a property's rent is high enough relative to its price. | As a fast, initial screening tool to eliminate underperforming properties from consideration. |

Using this trio gives you a well-rounded view, allowing you to quickly filter properties with the 1% Rule, compare their underlying value with the Cap Rate, and finally, project your personal return with the Cash-on-Cash calculation.

The Hidden Factors That Influence Your Cash Flow

Getting your initial cash flow numbers on a spreadsheet is a great first step. But the real world has a funny way of throwing curveballs at those neat calculations. A handful of powerful, and often overlooked, factors can either pump up your returns or quietly eat away at your profits.

If you want to protect and grow your investment, you have to understand these variables. They generally fall into three buckets: things specific to the property itself, shifts in the broader market, and the way you structure your financing. Let's break them down.

Property-Specific Variables

The unique details of your rental property have the most direct and immediate impact on your cash flow. It’s common sense, really: a well-kept building in a great spot will always command higher rent and attract better tenants, which means fewer costly vacancies.

Here are the big ones to watch:

- Location and Neighborhood: How close is the property to jobs, good schools, or popular amenities? This directly drives rental demand and what you can realistically charge. Finding the best cities to invest in rental property is often the most important decision you'll make.

- Property Condition and Age: Sure, that older property might have an attractive price tag. But it could be a money pit waiting to happen, with surprise capital expenditures like a new roof or HVAC system that can wipe out your cash flow for an entire year.

- Tenant Quality: A fantastic, long-term tenant who pays on time and treats the place with respect is worth their weight in gold. On the flip side, poor tenant screening can lead to a nightmare of late payments, property damage, and the expensive headache of eviction.

Market and Economic Dynamics

No property is an island. Your investment is constantly being pushed and pulled by wider economic trends and what’s happening in the local market. A booming local economy with lots of job growth can be a powerful tailwind, driving up rental demand and letting you increase your income.

But it works both ways. An economic downturn can lead to higher vacancies and force you to lower rents. Seemingly small events, like a major local employer shutting down or a change in zoning laws, can dramatically impact your property’s performance.

Stable cash flow is the hallmark of a resilient investment. When markets recover, the smartest money often flows into assets with locked-in income. For example, European real estate deals hit $50 billion in early 2025, a jump driven by investors chasing properties that guarantee long-term cash flow.

This is exactly why experienced investors are obsessed with market health. To see what the pros are watching, you can explore insights into global private markets.

Financing and Loan Terms

Finally, how you finance the deal is one of the biggest levers you have for controlling cash flow. Your mortgage—the interest rate, the loan term, the type of loan—directly sets your monthly debt service, which is almost always your single biggest expense.

It's simple math. A lower interest rate means a smaller monthly payment and more cash left over for you. A 30-year loan will have a lower monthly payment than a 15-year loan, instantly improving your cash flow (even if you pay more in total interest over the life of the loan). Thinking carefully about your financing isn't just a final step; it's a core strategy for maximizing profit from day one.

Proven Strategies to Increase Rental Cash Flow

Once you’ve got a handle on the math behind cash flow, the real work begins: actively managing and improving it. Smart investors know that owning a rental property isn't a "set it and forget it" venture. It’s a constant process of optimization, always looking for ways to widen that all-important gap between what comes in and what goes out.

At its core, it's pretty simple. You can either make more money or spend less of it. The truly successful investors manage to do both at the same time, turning a good investment into a great one and building real, long-term wealth.

Smart Ways to Increase Your Income

Boosting your property's income doesn't always require a massive overhaul. Often, it's about making smart, strategic upgrades that tenants are genuinely willing to pay more for. A small investment can justify a significant rent increase and attract a better pool of applicants.

Here are a few proven ways to get more out of your property:

- Make Strategic Upgrades: Don’t just renovate—renovate with a purpose. Focus on the high-impact areas. A refreshed kitchen with a modern backsplash or updated bathroom fixtures can completely change the feel of a unit and boost its rental value.

- Add In-Demand Amenities: Think about what makes a renter's life easier. An in-unit washer and dryer is almost always at the top of the list. That one addition can often let you bump the rent by $50-$100 per month.

- Monetize Unused Space: Do you have an empty garage, a spare driveway spot, or a storage shed just sitting there? These are hidden assets. Consider renting them out separately, either to your tenants or even to neighbors, for a surprisingly easy new income stream.

Proven Tactics to Reduce Expenses

Now for the other side of the coin: cutting costs. Trimming your expenses has an immediate and direct impact on your cash flow. The key is to be efficient without being cheap—you don't want to cut corners in a way that hurts the tenant experience and leads to vacancies.

This focus on the income side of the equation is becoming critical. Global forecasts for 2025 point toward flat capital values, which means investors will need to lean almost entirely on rental income for their returns. Some sectors, like data centers, are already showing strong cash flow potential, delivering 11.2% returns through Q3 2024. You can dig into the full global real estate trends report to see the bigger picture.

Key Takeaway: Every dollar saved on expenses is a dollar of pure profit added directly to your cash flow. Unlike increasing rent, which can be limited by market conditions, cost-saving is almost entirely within your control.

Here are some of the most effective cost-cutting strategies to consider:

- Refinance Your Mortgage: Your mortgage is likely your biggest single expense. If interest rates have dropped since you bought the property, refinancing could slash your monthly payment and instantly improve your cash flow.

- Appeal Your Property Taxes: Tax assessments aren't set in stone, and they aren't always right. Do some homework on comparable properties in your area. If you find your assessment is out of line, file an appeal—you could end up with a much lower tax bill.

- Implement Preventative Maintenance: Don't wait for that panicked 2 a.m. call about a burst pipe. A proactive maintenance schedule for your HVAC, plumbing, and roof can catch small issues before they snowball into budget-destroying emergencies. It's about spending a little now to save a lot later.

Automating Your Cash Flow Analysis

Knowing the formulas is a great start, but let's be realistic. Running the numbers for every single property you see is a huge time-sink. In a hot market, spending hours buried in spreadsheets means you could watch the perfect deal slip through your fingers. This is exactly where technology gives savvy investors an edge, turning tedious manual work into an automated advantage.

Tools like Property Scout 360 are built to do all the heavy lifting. Forget plugging numbers into a calculator one by one. You get an instant, in-depth financial breakdown for any residential property in the U.S. All those critical metrics we just covered—NOI, cash-on-cash return, and cap rate—are crunched in seconds, taking guesswork and human error out of the equation.

This gives you a crystal-clear financial snapshot of any property you’re eyeing.

The dashboard lays out the most important numbers visually, so you can compare potential returns at a glance and immediately see which properties are worth a closer look.

Make Decisions Faster with Data

The real magic happens when you combine automation with powerful, integrated data. Property Scout 360 doesn't just run formulas; it pulls in real-time MLS listings, tax records, and market-based rent estimates. This means your analysis is built on solid ground, not just wishful thinking. The platform can also model different financing scenarios and project detailed expenses, from insurance and property taxes to vacancy and maintenance costs.

The shift from manual calculation to automated analysis turns hours of tedious research into minutes of focused decision-making. It cuts through analysis paralysis and empowers you to act with confidence, backed by solid data.

Sure, you could try to build your own system from scratch. Our guide on creating a rental property calculator in XLS walks you through it, but you'll see just how complex it can be to build and maintain. For those wanting to manage finances more broadly, a pre-built cash flow forecasting template can also be a helpful tool.

Ultimately, automation frees you up to focus on what actually matters: interpreting the results and making the right call. Instead of getting bogged down in math, you can spend your time on strategy. You can analyze more properties, make offers faster, and dramatically increase your odds of landing a top-performing investment before someone else does.

Common Questions About Real Estate Cash Flow

Even after you've got the formulas down, some practical questions always pop up. Let's tackle a few of the most common ones I hear from investors to help you move forward with confidence.

What Is a Good Cash Flow for a Rental?

Everyone wants a magic number, but the truth is, "good" cash flow really depends on your specific market and goals. That said, a solid rule of thumb many seasoned investors aim for is $200 to $400 per month, per unit.

This range usually gives you a nice cushion for those inevitable surprise costs while still making the investment worth your time. In a pricey market like San Diego, you might be happy with less. In a more affordable area like Cleveland, you might shoot for even more.

Can Negative Cash Flow Ever Be a Good Investment?

It can be, but you have to know what you're getting into. This is a classic high-risk, high-reward play. When you buy a property with negative cash flow, you’re not investing for monthly income; you’re betting purely on appreciation.

You're hoping the property's value goes through the roof, giving you a massive payday when you eventually sell. This strategy is really only for experienced investors with deep pockets who can comfortably cover losses each month. For most of us, positive cash flow is the far safer and more reliable way to build wealth.

A property that pays you every month is a business. A property that you pay for every month is an expensive hobby—or a gamble.

How Do I Plan for Unexpected Expenses?

The trick is to stop thinking of them as "unexpected." They will happen. The key is to budget for Capital Expenditures (CapEx) and vacancies from the very beginning. A smart practice is to automatically set aside 5-10% of your gross monthly rent for those big-ticket items like a new roof or an HVAC system down the line.

On top of that, budget another 5% for vacancies. By building these reserves into your monthly plan, a major repair or a month without a tenant won't sink your investment. It just becomes a predictable cost of doing business.

Ready to stop guessing and start making data-driven decisions? Property Scout 360 automates all these complex calculations, giving you instant cash flow analysis for any property in the U.S. Find your next profitable investment in minutes at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.