Down Payment Requirements for Investment Property Uncovered

Unlock your real estate portfolio. This guide breaks down the down payment requirements for investment property, loan types, and funding strategies.

When you're buying a home to live in, you can often get away with a pretty small down payment. But when you step into the world of investment properties, the rules of the game change entirely.

The standard down payment for an investment property is a whole different ballgame, typically falling somewhere between 15% and 25% of the purchase price. This isn't an arbitrary number; it's all about how lenders see the deal.

Your First Hurdle in Real Estate Investing

So, why the steep entry fee for an investment property? It boils down to one word: risk.

Lenders view your primary home as a necessity—it's the roof over your head. An investment property, on the other hand, is a business venture. That simple distinction completely changes their risk calculation. From their perspective, if you hit a financial rough patch, you're far more likely to make the mortgage payment on your own home and let the rental property slide.

To protect themselves from that added risk, lenders demand more "skin in the game" from you, the investor. This is why the typical 3-5% down payment you see for an owner-occupied home balloons into a much more substantial figure for a non-owner-occupied property.

A higher down payment shows the lender you're serious and financially committed. It also gives them a bigger equity cushion, which reduces their potential loss if things go south and the property ends up in foreclosure.

Primary Home vs Investment Property Down Payment at a Glance

Let's put some real numbers to this to see just how different the cash requirement can be. The table below shows a quick comparison for a sample $350,000 property, illustrating what you might expect to pay for your own home versus an investment.

| Loan Type | Property Use | Typical Down Payment % | Down Payment Amount on $350,000 |

|---|---|---|---|

| Conventional | Primary Home | 3% - 5% | $10,500 - $17,500 |

| Conventional | Investment Property | 15% - 25% | $52,500 - $87,500 |

As you can see, the upfront cash needed for an investment property is significantly higher, a crucial factor to plan for long before you start making offers.

The Financial Reality of an Investment Down Payment

This isn't just a small jump; it’s a financial leap. For a pretty standard $300,000 rental property—a common starting point for many new investors—you're looking at needing $45,000 to $75,000 for the down payment alone. And that's before you even factor in closing costs and cash reserves, which can easily push the total cash you need to $70,000 or more.

As you start your journey, it’s a good idea to understand the different types of real estate investment, as the financing can have unique quirks for each.

Grounding your property search in this financial reality from day one is absolutely critical. Before you fall in love with a listing, you need a crystal-clear picture of the capital required to actually close the deal.

This is where tools like Property Scout 360 become so valuable. They let you model these upfront costs with precision. You can run scenarios with different down payment percentages and instantly see how much cash you'll need and how that decision impacts your long-term returns. It turns abstract numbers into a concrete, actionable investment plan.

For those just getting their feet wet, our guide on how to buy your first rental property provides a great step-by-step roadmap to get you started.

Navigating Your Investment Loan Options

When you're figuring out the down payment for an investment property, the single biggest factor is the type of loan you get. Not all financing is built the same, and getting a handle on the different options is essential before you even start looking at properties. Each loan product has its own rulebook for how much cash you need to bring to the table.

Think of it like choosing the right tool for a job. You wouldn't use a hammer to drive a screw. In the same way, the loan you pick needs to match your specific investment strategy and financial situation.

The Investor Go-To: Conventional Loans

For most real estate investors, the conventional loan is the well-trodden path. These are the standard mortgages you’d get from a bank or private lender, but they come with stricter requirements when you aren't planning to live in the property yourself.

Lenders are going to want a down payment somewhere between 15% and 25% for a conventional investment property loan. While you might occasionally snag a 15% deal if you have a stellar credit score and plenty of cash reserves, the real industry standard is 20%. Putting down that 20% is crucial because it lets you sidestep Private Mortgage Insurance (PMI)—an extra monthly fee that protects the lender, not you, and can take a serious bite out of your cash flow.

A Savvy Workaround: The FHA Multi-Family Loan

What if you could buy an investment property with as little as 3.5% down? It sounds too good to be true, but it's entirely possible with a strategy called "house hacking." This involves using an FHA loan to buy a multi-family property with two to four units.

Here’s the catch: you have to live in one of the units as your primary residence for at least one year. By doing this, you can finance the entire building with a tiny down payment and have your tenants' rent payments cover a huge chunk of your mortgage. For new investors trying to break into the market with limited capital, this is one of the most powerful strategies out there.

Specialized Financing for Investors

Beyond the standard choices, a few specialized loans are designed specifically for real estate investors, each with its own down payment expectations.

- VA Loans: If you're an eligible veteran or active-duty service member, you can also use a VA loan to house hack a multi-family property (up to four units). The best part? It requires 0% down, as long as you live in one of the units.

- DSCR Loans: Debt Service Coverage Ratio (DSCR) loans are a real game-changer. With these, lenders qualify you based on the property’s projected rental income, not your personal W-2. Because the property’s ability to pay for itself is the main focus, lenders want more skin in the game from you, typically requiring a down payment in the 20% to 30% range.

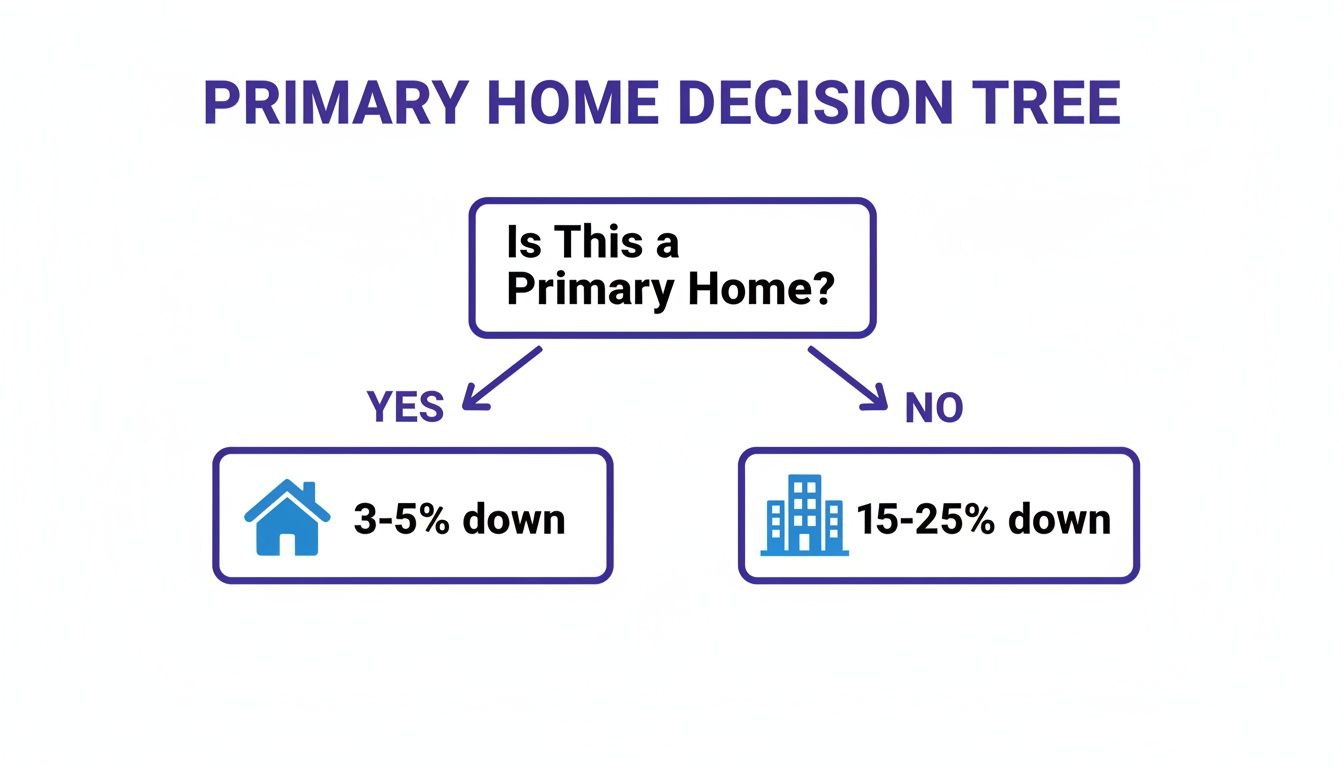

This decision tree breaks down the core factor that determines your down payment.

As you can see, whether or not you plan to live in the property is the first and most important question a lender asks. It completely changes the amount of cash you need upfront.

The gap between financing a primary home versus a pure investment is huge. For conventional loans, the down payment for an investment property has really firmed up around 20-25%, which is a world away from the 3-3.5% options available to owner-occupants. This difference is all about risk; lenders need a bigger cushion to protect themselves against potential vacancies.

Picking the right financing is a foundational step in your investment journey. For a more detailed look at your options, take a look at our complete guide on how to finance a rental property. Before you make a decision, it’s a smart move to model these different scenarios in a tool like Property Scout 360 to see exactly how each loan structure will impact your long-term returns.

How Your Choice of Property Impacts Your Down Payment

Lenders don't just put you under the microscope; they're scrutinizing the property itself just as carefully. The type of real estate you decide to buy isn't just a portfolio strategy—it's a major factor in determining your down payment requirements for an investment property. Lenders see different levels of risk in different types of properties, and that risk calculation directly translates into how much cash you need to bring to the table.

Think of it this way: a standard single-family home is like buying a blue-chip stock—predictable and relatively low-risk. A multi-unit building, on the other hand, is more like a complex investment fund with more moving parts. Each has a unique risk profile, and your lender will adjust the "buy-in" price—your down payment—to match.

Single-Family Residences (SFRs)

From a lender's point of view, single-family homes are often the safest bet. They're generally easier to appraise, manage, and, if it comes to it, sell. This lower perceived risk usually means you get more favorable financing terms.

For a conventional loan on an SFR, you can sometimes find a lender willing to go as low as a 15% down payment. Still, the gold standard is 20%. Hitting that magic number helps you secure better interest rates and, crucially, avoid paying Private Mortgage Insurance (PMI).

Condominiums and Properties with HOAs

Buying a condo isn't just about you and your unit. The lender is also taking a chance on the financial stability of the Homeowners Association (HOA). A poorly run or underfunded HOA can spell trouble, leading to surprise special assessments or neglected common areas, which jeopardizes the lender's collateral.

Because of this extra layer of risk, lenders almost always ask for more skin in the game for investment condos. Don't be surprised to see down payment requirements jump to 25% or even higher, especially for buildings that don't meet strict lending guidelines (often called "non-warrantable condos").

Small Multi-Family Properties (2-4 Units)

Multi-family properties—duplexes, triplexes, and fourplexes—are fantastic for building wealth because you get multiple rent checks from a single property. But for a lender, this is a double-edged sword. Yes, the income potential is greater, but so are the headaches: more complex management, higher maintenance bills, and the risk of multiple vacancies at once.

To balance out this increased risk, lenders will demand a larger down payment. For a purely investment (non-owner-occupied) multi-family property, you should be prepared to put down at least 25%. The thinking is simple: a bigger upfront investment from you shows you're serious about managing a more complicated asset. If you're exploring this path, our guide on how to buy a duplex property gets into the nitty-gritty of this strategy.

Knowing how property type influences your down payment helps you focus your search on what you can realistically afford. It saves you from spinning your wheels and ensures your investment goals are grounded from day one.

The Financial Factors That Move the Needle

When you're trying to secure a loan for an investment property, the lender isn't just looking at the building. They're really looking at you. Your personal financial health is the biggest piece of the puzzle, telling them how much of a risk they're taking by lending you money. A strong financial picture can open doors to better terms, while a weaker one often means the lender will ask for a higher down payment to feel more secure.

Think of it this way: lenders need to know you can handle the mortgage payments, even if a tenant moves out unexpectedly or the furnace dies in the middle of winter. Four key metrics paint this picture for them. Let's break them down.

Your Credit Score and Why It Matters

The very first thing a lender will pull is your credit score. It’s a quick, standardized way for them to see how you've handled debt in the past. While you might be able to buy your own home with a score in the low 600s, the game is different for investment properties. The bar is set much higher.

For the best possible terms—including the lowest down payment, usually 20% on a conventional loan—most lenders want to see a credit score of at least 740. If your score dips below that, don't be surprised if the lender asks for more skin in the game. They might bump the required down payment to 25% or more to offset what they perceive as added risk.

To illustrate just how much your credit score can influence your loan, let's look at some sample numbers. A higher score doesn't just lower your down payment; it can save you a significant amount of money over the life of the loan through a lower interest rate.

How Your Credit Score Impacts Down Payment and Interest Rate

| Credit Score Range | Typical Minimum Down Payment % | Example Interest Rate | Monthly Payment on $300k Loan |

|---|---|---|---|

| 760+ (Excellent) | 20% | 6.75% | $1,945 |

| 700-759 (Good) | 20% - 25% | 7.25% | $2,047 |

| 660-699 (Fair) | 25% | 7.875% | $2,171 |

| 620-659 (Below Average) | 25% - 30% | 8.5% | $2,307 |

As you can see, the difference between an excellent and a fair credit score can easily add up to several hundred dollars a month. That's cash flow that could be going into your pocket instead of the bank's.

Debt-to-Income Ratio (DTI)

Next up is your Debt-to-Income (DTI) ratio. This is a simple but powerful calculation that compares your total monthly debt payments (car loans, credit cards, student loans, and your future investment property mortgage) to your gross monthly income. It’s a lender’s gut check on whether you can comfortably take on another big payment.

For investment properties, lenders typically want to see a DTI of 43% or lower. If you’re already pushing up against that limit, a lender might see you as financially overextended. To protect themselves, they’ll likely ask for a larger down payment to reduce their loan amount and, by extension, their risk. A low DTI, on the other hand, screams financial stability and makes you a much more attractive borrower.

Loan-to-Value Ratio (LTV)

Loan-to-Value (LTV) is just the other side of the down payment coin. It's the loan amount measured as a percentage of the property's price. It’s a direct reflection of how much equity you have from day one.

Let's say you put 20% down on a $300,000 property. Your down payment is $60,000, which means your loan is for $240,000. Your LTV is 80% ($240,000 ÷ $300,000). A bigger down payment means a lower LTV.

And a lower LTV is exactly what lenders love to see. It gives them a bigger safety cushion. If something goes wrong and you default, they have a better chance of recouping their money. This is precisely why a 20% down payment, which creates an 80% LTV, has long been the gold standard for investment property loans.

Cash Reserves After Closing

Finally, lenders want to see that you’re not wiping out your savings account to buy the property. They need to know you have cash left over after paying the down payment and all the closing costs. This leftover money is called cash reserves.

These reserves are your safety net. They prove you can cover the mortgage (PITI: Principal, Interest, Taxes, and Insurance) and other holding costs if you hit a rough patch, like a few months of vacancy or a major appliance failure.

Most lenders will require you to show enough cash reserves to cover six months of PITI payments for the new property. Having more than the minimum is always a good thing—it strengthens your application and can sometimes even help you qualify with a slightly lower down payment. It shows the lender you're a responsible investor who is prepared for the unexpected.

Don't Have the Cash? Creative Ways to Fund Your Down Payment

Staring at the down payment requirement for an investment property can feel like looking at a mountain. It’s a big number, and it can feel a little overwhelming. But here's what experienced investors know: your checking account is just one place to find that cash.

The most successful investors get creative. They learn to look at their entire financial picture—not just their liquid savings—to find the capital needed to close a deal. Let's dig into a few of these strategies.

Look at the Assets You Already Own

For many homeowners, the single biggest untapped resource is sitting right inside their primary residence: home equity. A Home Equity Line of Credit (HELOC) is a popular tool for a reason. It lets you borrow against the equity you've built, giving you a revolving line of credit that you can tap for a down payment.

Think of it this way: you're essentially turning the "dead" equity in your house into working capital for an asset that will generate income. It's a smart move, but you have to go in with your eyes open. This strategy adds another monthly payment to your personal budget and directly links the performance of your investment property to the safety of your own home.

Another powerful, though more advanced, option is to look at your retirement accounts. With a Self-Directed IRA (SDIRA), you can break free from the traditional stock and bond market and invest those retirement funds directly into real estate. The compliance rules are tight and you'll need a specialized custodian, but it allows you to put your tax-advantaged dollars to work in a tangible asset.

Using a HELOC or an SDIRA is a classic leverage play. You're using borrowed money (or retirement funds) to make more money. But remember, leverage magnifies everything. It can amplify your returns, but it can also amplify your losses if things go south. Before you pull the trigger, you absolutely must be sure the rental income can comfortably cover all your financing costs, not just the new mortgage.

Partner Up or Work with the Seller

What if you don't have a ton of home equity or a hefty IRA? All is not lost. You just have to think a little differently about how deals get done.

- Seller Financing: Sometimes, the seller themselves can become your bank. In a seller-financing arrangement, the owner agrees to carry a note for a portion of the purchase price, which can dramatically reduce the cash you need to bring to the table. This isn't common, but for the right property with a motivated seller, it can be a game-changer. It all comes down to your ability to negotiate.

- Investor Partnerships: Can't swing a deal on your own? Find someone who can! Partnering is a fantastic way to break into the market. You might have the skills to find and manage a great property, while your partner has the capital for the down payment. Just make sure you have a rock-solid legal agreement in place before any money changes hands.

Each of these strategies fundamentally changes the math on your investment. It’s absolutely critical to model every scenario to see how it affects your cash flow, your overall risk, and your potential return on investment.

Putting It All Together with Property Scout 360

It’s one thing to understand the theory behind down payments, but it's another thing entirely to make a confident investment decision with real money on the line. This is where all the concepts we've walked through—loan types, property risk, and your own financial health—finally come together. A tool like Property Scout 360 can be your co-pilot here, helping you move from guesswork to a data-driven analysis.

Let’s say you’ve found a promising duplex on the market for $320,000. Instead of getting tangled up in a messy spreadsheet trying to track dozens of variables, you can simply plug in different down payment requirements for your investment property and see what happens. How does a 20% down payment stack up against a 25% one? What does that do to your monthly cash flow?

Modeling Scenarios for a Clear Decision

This hands-on approach is what turns abstract financial concepts into a clear, actionable dashboard. As you gather intel on a potential deal, getting a new property estimate is a crucial first step for figuring out your potential down payment and whether the numbers work at all. With a tool like Property Scout 360, you can lay these scenarios out side-by-side.

- Scenario A (20% Down): You'll need less cash upfront, which is great. But your monthly mortgage payment will be higher, potentially putting a tight squeeze on your cash flow.

- Scenario B (25% Down): This requires more cash to close the deal, no doubt. The trade-off? A lower monthly payment that immediately boosts your cash-on-cash return and gives you a healthier profit margin from day one.

The platform doesn't just crunch the numbers; it visualizes the outcomes, showing you exactly how a bigger down payment can impact your long-term wealth creation.

Here’s a glimpse of a sample dashboard that shows how these key financial metrics are laid out.

This kind of clear, visual breakdown lets you instantly grasp the immediate and future financial impact of your down payment choice.

It's time to stop guessing and start making data-backed investment choices. The right tool gives you the power to analyze deals quickly and accurately, turning complex down payment requirements into a simple, solvable part of your investment equation. This is how you move forward with confidence, knowing your numbers are solid.

Your Top Down Payment Questions, Answered

When you're diving into investment property financing, a few common questions always pop up. Let's clear the air on these so you can build your strategy on solid ground.

Can I Use Gift Funds for My Down Payment?

For an investment property, the answer is almost always a hard no.

Lenders need to see that you have your own "skin in the game." The down payment has to come from your own money—checking, savings, or brokerage accounts—to prove you have a real financial stake in the deal. This is a huge part of their risk calculation. Gift funds are typically only allowed for primary residences, not rentals.

Do I Have to Pay PMI on an Investment Property?

You might, and it's something you definitely want to avoid. If you put down less than 20% on a conventional loan, you’ll almost certainly get hit with Private Mortgage Insurance (PMI).

This is exactly why most seasoned investors will do whatever it takes to hit that 20% down payment mark. Dodging that extra monthly PMI payment goes straight to your bottom line, boosting your property’s cash flow from day one.

Ready to stop guessing and start analyzing deals with precision? Property Scout 360 gives you the tools to model different down payment scenarios and instantly see their impact on your cash flow and long-term returns. Start analyzing properties for free today at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.