How to Finance Rental Property The Savvy Investor's Playbook

Learn how to finance rental property with this comprehensive guide. We cover everything from conventional loans to creative financing for your next investment.

Getting the financing for your first (or next) rental property doesn't start when you find a great deal. It starts months, sometimes even years, before. The real work is in shaping your financial profile so that when you do find that perfect property, lenders see you as a slam-dunk applicant.

It's all about laying the groundwork—beefing up your credit score, wrestling your debt-to-income ratio into submission, and having your paperwork in order. This prep work is what separates a smooth, successful closing from a stressful, last-minute scramble.

Becoming the Borrower Lenders Want to Fund

Before you even start browsing listings, your goal should be to look like an ideal borrower on paper. Think of it from the lender's perspective. They're looking for stability, responsibility, and a low risk of default. It's about more than just having money in the bank; it’s about strategically managing your entire financial picture.

Getting a Handle on Your Debt-to-Income Ratio

Lenders are obsessed with one particular metric: your Debt-to-Income (DTI) ratio. This little number tells them how much of your monthly income is already spoken for by other debt payments. It's a quick stress test of your ability to handle another mortgage.

For investment properties, most lenders want to see a DTI of 43% or less.

To get your DTI in shape, focus on paying down debt. A lot of people talk about the "snowball" method, but for this purpose, the "avalanche" strategy is often better. That means tackling your high-interest debt first—think credit cards. Paying down a $10,000 credit card with a 22% APR will make a much bigger dent in your monthly payments and DTI than chipping away at a low-interest student loan.

Building an A+ Credit Profile

Your credit score is your financial report card, and lenders are tough graders. They're not just looking at the final score; they're digging into the details of your credit report.

Here’s what they care about most:

- Payment History: This is a pass/fail test. A solid history of on-time payments is absolutely critical. A single 30-day late payment can be a deal-breaker for some underwriters.

- Credit Utilization: This is how much of your available credit you're using. You want to keep this figure below 30%, but if you can get it under 10%, you're in the gold-star category.

- Length of Credit History: Lenders love to see old, well-managed accounts. It shows you have a long track record of responsible borrowing. Whatever you do, don't close your oldest credit cards, even if you rarely use them.

I see this all the time with new investors: they'll open a new store credit card or apply for a car loan right before they start shopping for a mortgage. Big mistake. Those hard inquiries and the drop in the average age of your accounts can ding your credit score at the worst possible moment.

Getting Your Paperwork in Order

When you find a deal, you need to move fast. The last thing you want is to be scrambling to find two-year-old tax returns while another buyer swoops in. Start building your "loan application kit" now.

Lenders will almost always ask for the following:

- Two years of tax returns (personal and business, if you have one)

- Two months of recent bank statements for every single account (checking, savings, brokerage)

- 30 days of pay stubs or other proof of steady income

- A full accounting of your assets and liabilities

Having this ready to go shows you’re organized and serious.

For investors who hold their properties in a business entity, you'll also need an Employer Identification Number. You can learn more about understanding EIN numbers.

Lenders use this paper trail to confirm your income is stable, check for any large, sketchy deposits, and make sure you have enough cash reserves to cover the down payment, closing costs, and a few months of mortgage payments. If you're planning to use the property's future rent to help you qualify, you'll want to get familiar with specific loan products built for that. To learn more, check out our guide on DSCR loans and see how they can unlock your next investment: https://propertyscout360.com/blog/what-is-dscr-in-real-estate

So, you're ready to jump into real estate investing. Fantastic. The first major hurdle for almost everyone is figuring out the financing. It can feel a bit overwhelming, but let's break down the most common path: the conventional loan.

This is the bread and butter of real estate financing. Think of it as the go-to loan from traditional lenders like banks and credit unions. It’s the standard for a reason, but when you're buying a rental, the rules are a bit different than when you bought your own home. Lenders see an investment property as a business transaction, so expect them to look at your application with a much finer-toothed comb.

The Ground Rules of Conventional Investment Loans

The first thing any lender will want to know is how much skin you have in the game. For a conventional investment loan, that means a down payment of at least 20%, though 25% is becoming the new standard.

Why so high? It's all about managing risk for the bank. They know that if you hit a financial rough patch, you’re far more likely to default on a rental property mortgage than on the one for your own home. A bigger down payment means you have more equity from day one, which gives the lender a solid cushion.

Here’s a pro tip for new investors: a larger down payment can often score you a better interest rate. Bumping your down payment from 20% to 25% can sometimes shave a quarter of a point or more off your rate. That might not sound like much, but it adds up to thousands of dollars in savings over the life of the loan.

Next up is your credit score. To get the best rates and terms on an investment property, you’ll want a score of 740 or higher. It's sometimes possible to get approved with a score in the high 600s, but you'll definitely pay for it with a higher interest rate.

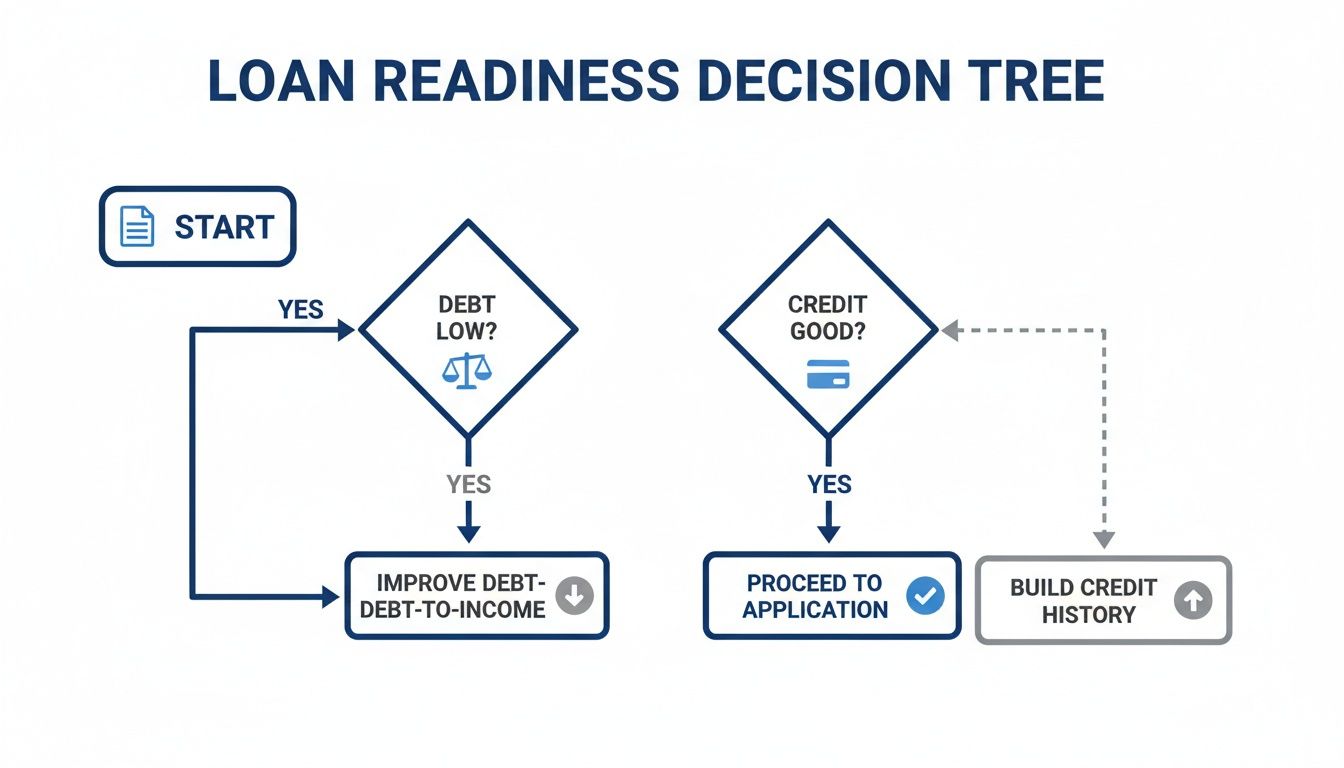

This decision tree gives you a quick visual on where to start—it all comes down to getting your debt and credit in order before you even talk to a lender.

As you can see, a strong credit score and a manageable debt load are the two pillars that support a successful loan application. Get those right, and you're halfway there.

Owner-Occupied Strategies: A Smarter Way In

While conventional loans are the standard, they aren't your only option. Government-backed loans can be a brilliant workaround, especially if you’re open to a strategy called "house hacking."

The concept is simple: you buy a small multi-family property (a duplex, triplex, or fourplex), live in one of the units yourself, and rent out the others. Because you're an owner-occupant, you unlock access to loans with incredible terms.

- FHA Loans: Insured by the Federal Housing Administration, these loans let you buy a property with as little as a 3.5% down payment. The only catch is you have to live in one of the units for at least a year.

- VA Loans: If you're a veteran, active-duty service member, or eligible surviving spouse, the VA loan program is a game-changer. We're talking 0% down and no private mortgage insurance (PMI), which can slash your monthly payments.

Think about it this way: you could buy a $400,000 duplex with an FHA loan for just $14,000 down. If the rent from the other unit covers most of your mortgage, you could be living nearly for free while building equity. After your year is up, you can move out, rent your old unit, and now you have a fully-functioning cash-flowing asset. It’s one of the most powerful ways to get started.

Comparing Common Rental Property Loan Types

To help you see how these stack up, here’s a side-by-side look at the most common loan types for new investors. Each has its place depending on your goals and financial situation.

| Loan Type | Typical Down Payment | Occupancy Requirement | Best For |

|---|---|---|---|

| Conventional | 20-25% | None (investor loan) | Investors with strong credit and significant capital for a down payment. |

| FHA | 3.5% | Must occupy one unit for 1 year | First-time investors using the "house hacking" strategy on a 2-4 unit property. |

| VA | 0% | Must occupy one unit for 1 year | Eligible veterans looking for the lowest entry cost via house hacking. |

| Portfolio | Varies (often 25%+) | Varies by lender | Experienced investors who need flexible underwriting to scale their portfolio. |

Choosing the right loan is about aligning the product's features with your specific investment strategy, whether that’s a traditional single-family rental or a multi-unit house hack.

Portfolio Loans: The Key to Scaling Up

Once you’ve successfully acquired a few properties, you might find that getting another conventional loan becomes tricky. Most big lenders have a cap on the number of mortgages they'll give to a single person.

This is where portfolio loans come into play.

A portfolio loan is a non-conforming loan, meaning it doesn't have to meet the rigid standards of Fannie Mae or Freddie Mac. The lender keeps the loan on its own books (its "portfolio") instead of selling it, which gives them a ton of flexibility in the approval process.

Instead of obsessing over your personal debt-to-income ratio, a portfolio lender takes a holistic look at your entire real estate portfolio. They’re more interested in the cash flow your existing properties generate. If you can show them that your portfolio is healthy and profitable, they’re often happy to fund your next deal, even if you wouldn't qualify under strict conventional rules. For serious investors, these loans are the key to building a real estate empire.

Sometimes, the best rental property deals are the ones everyone else overlooks. In a competitive market, it's not always the highest offer that wins, but the one that's the most flexible and can close the fastest. This is where conventional bank loans can hold you back.

When you need to move quickly or a property doesn't fit the bank's perfect little box, creative financing isn't just an option—it’s your competitive advantage.

These non-traditional approaches let you craft a deal that solves a problem for the seller, which in turn solves your financing problem. It takes more hustle and negotiation, but the payoff can be huge, letting you snap up opportunities that are invisible to other buyers.

The Power of Seller Financing

In a seller financing deal, you cut out the middleman. The property owner effectively becomes your bank, and you make your monthly payments directly to them. It’s a beautifully simple concept.

So, who is the ideal seller for this? Think of landlords who’ve owned their properties for years and are just tired of the day-to-day management. Or maybe they’re facing a big capital gains tax bill and would rather receive a steady income stream over time. These are motivated sellers who can be open to a creative solution.

Everything is on the table when you negotiate the terms. This is your chance to structure a true win-win.

- Down Payment: A bank will almost always demand 20-25% for an investment property. A seller, however, might be perfectly happy with 10-15% if the interest rate is right.

- Interest Rate: You have a lot of wiggle room here. Offering a rate slightly higher than the going bank rate can make the deal much more attractive to the seller, especially if you're asking for a lower down payment.

- Loan Term: Seller-financed deals often have shorter terms, like 5-10 years, with a balloon payment at the end. This gives you plenty of time to add value to the property and then refinance into a traditional mortgage down the road.

Seller financing isn't just a backup plan; it's a strategic tool. I once secured a duplex with just 10% down because the seller was more interested in reliable monthly income than a large cash payout. We agreed on a seven-year term, giving me plenty of time to increase rents and build equity before refinancing.

The whole arrangement gets formalized with a promissory note and a mortgage or deed of trust, just like a loan from a big bank. To get into the nitty-gritty of the paperwork, check out our deep dive on understanding what a seller note is.

Using Hard Money for Speed and Opportunity

Think of hard money loans as the secret weapon for investors who need to act fast. These are short-term loans from private companies or investors who care about one thing above all else: the asset.

They're not digging through your tax returns. Instead, hard money lenders focus almost entirely on the property’s potential, specifically its After Repair Value (ARV). This makes them a perfect fit for strategies like BRRRR (Buy, Rehab, Rent, Refinance, Repeat), where you’re buying a distressed property that a traditional lender wouldn't even consider. You can often get funded in a matter of days, not months.

Of course, this speed comes at a price. You're looking at interest rates anywhere from 8-15% and origination fees of 2-5%. It sounds steep, but when it’s the only tool that lets you seize a killer deal, that cost can be easily justified.

Partnering Up with Private Money Lenders

Private money is just a fancy term for borrowing from people you know—friends, family, colleagues, or other investors in your network. This is lending built on relationships, not algorithms.

Unlike hard money, the terms are completely bespoke. You and your private lender sit down and hammer out every detail: the interest rate, the repayment schedule, the length of the loan. It's all about what works for both of you.

These partnerships usually take one of two forms:

- Debt Partnership: This is a straightforward loan. Your private lender gives you capital, and you pay them a fixed interest rate. They get a predictable return on their money, and you get to keep all the equity and appreciation.

- Equity Partnership (Joint Venture): Here, your partner contributes cash in exchange for a piece of the pie—an ownership stake in the property. They’re taking on more risk alongside you, but they also get to share in the cash flow and long-term profits.

To succeed with private money, you have to treat it professionally. You need a rock-solid deal analysis, a clear business plan, and realistic projections that show exactly how you’ll protect their investment and deliver the returns you’re promising. Trust is your most valuable currency here.

Stress-Testing Your Deal Before You Commit

Getting approved for a loan feels like a victory, but it’s not the finish line. Let me be clear: the best financing on the planet can't save a bad deal. Before you even think about signing those loan documents, you have to put the property through its paces and make sure the numbers hold up under pressure.

This isn't about wishful thinking. This analysis is your financial firewall. It’s what separates a smart, data-driven decision from a costly mistake that looks good on paper but crumbles in the real world.

It’s time to roll up your sleeves and dig into the math. This is where you prove the investment works before your own capital is at risk.

Calculating Your Core Profitability Metrics

To properly vet a rental property, you need to speak the language of real estate investors. Three key metrics will give you a clear, honest snapshot of any deal's potential.

- Net Operating Income (NOI): Think of this as the property's pure profit potential. It's all the income it generates minus all the operating expenses—before you factor in your mortgage payment. NOI tells you if the property itself is a winner, regardless of how you finance it.

- Capitalization Rate (Cap Rate): This is a simple but powerful one. You just divide the NOI by the property's purchase price. The cap rate gives you a quick way to compare the raw return potential of different properties. A higher cap rate often means a higher potential return (but usually, it comes with higher risk).

- Cash-on-Cash Return: For anyone using a loan, this is the number that matters most. It measures the annual cash flow you pocket (before taxes) against the total cash you put into the deal (down payment, closing costs, etc.). It answers the most important question: "For every dollar I invest, how much am I getting back each year?"

These aren't just academic exercises. Seasoned investors are constantly benchmarking loan terms against local rental yields. For example, in Spain, gross rental yields average around 5.4%, but you might see 6–8% for small apartments in prime Madrid or Barcelona districts. Over in Dubai, apartments generally produce ~6–7% gross yields. If you can lock in a loan with a moderate interest rate, those numbers work.

Building a Realistic Cash Flow Projection

I see new investors make this mistake all the time: they underestimate expenses. Your real monthly cost is so much more than the mortgage payment, often called PITI (Principal, Interest, Taxes, and Insurance). A solid projection has to account for the "Big Three" hidden cash-flow killers.

- Vacancy: Your property will not be occupied 100% of the time. Period. Set aside 5-10% of the gross annual rent for when the unit is empty between tenants.

- Repairs & Maintenance: Faucets leak. Water heaters fail. Things break. Budgeting another 5-10% of the gross rent for this is non-negotiable.

- Property Management: Even if you plan to manage it yourself, calculate an 8-12% property management fee. Why? It ensures the deal still makes sense if you hire a pro later, and more importantly, it pays you for your time and effort.

Don't forget the long-term impact of taxes. Understanding smart tax strategies for business owners can dramatically boost your actual take-home profit over the years.

A deal that "cash flows" by $50 a month on paper can quickly turn negative once you factor in a single month of vacancy or an unexpected HVAC repair. Always build these buffers into your analysis.

Comparing Financing Scenarios: A Tale of Two Mortgages

The loan you choose will have a massive impact on your investment's performance. Let's run a quick comparison on a hypothetical $300,000 property. You're putting 25% down ($75,000), so your loan is $225,000.

Scenario 1: 30-Year Fixed at 7% Interest

- Monthly Principal & Interest: $1,497

- Lower monthly payment which means more cash in your pocket each month.

- Slower equity build-up because you're stretching the payments out.

Scenario 2: 15-Year Fixed at 6.5% Interest

- Monthly Principal & Interest: $2,084

- Higher monthly payment that will significantly eat into your cash flow.

- Rapid equity build-up and you'll own the property free-and-clear much faster.

So, which one is better? It comes down to your personal strategy. The 30-year loan is the go-to for investors who want to maximize monthly cash flow. The 15-year loan, however, is a fantastic wealth-building machine for those who want to crush debt and build equity as quickly as possible.

Trying to run these numbers by hand is a pain. To make your life easier, we've built a powerful tool for this. Check out our guide on using a https://propertyscout360.com/blog/rental-property-spreadsheet-analysis to model these different scenarios in just a few minutes. This is how you make an informed, confident decision before putting your money on the line.

From Application to the Closing Table: What to Expect

Getting that pre-approval letter feels great, but it’s really just the starting gun for the final lap. The real race is getting from that initial application to the closing table, and this is where a lot of deals can get shaky.

This part of the process isn’t so much about your financial history—that's already been vetted. Now, it's all about the nitty-gritty details of the property itself and navigating the lender’s internal hoops. You've done the hard work of saving up and polishing your credit; now you have to stick the landing.

Choosing Your Lending Partner

Just because you have a pre-approval doesn't mean you're married to that lender. In fact, you absolutely should be shopping around. Don't get fixated on the interest rate alone; you need to scrutinize the entire loan estimate. I've seen lenders hide a less-than-great deal behind a low rate, only to make up for it with sky-high origination fees and other closing costs.

When you're comparing offers from different lenders, get straight to the point with these questions:

- What are your total estimated closing costs?

- Can you lock my interest rate today? For how long?

- Is there any kind of prepayment penalty on this loan?

- What's your typical closing timeline for an investment property?

A lender who hems and haws or is slow to respond is a huge red flag. As an investor, your two most valuable assets are speed and certainty. You need a partner who gets it and can close on schedule.

Surviving the Underwriting Gauntlet

Once you've picked a lender and have a property under contract, your file gets handed off to underwriting. Think of the underwriter as the ultimate skeptic. Their job is to poke holes in your file, comb through every document you’ve submitted, and verify every single claim.

This is where deals often get bogged down. That large, random cash deposit from two months ago? They’ll want a full paper trail explaining where it came from. Opened a new credit card and saw a slight dip in your score? That could genuinely put your entire approval at risk.

The key to a smooth underwriting experience is to be organized and responsive. Give them exactly what they ask for, as quickly as you can, and don't volunteer extra information. Answer their questions cleanly and directly to avoid giving them new threads to pull on.

The Appraisal and Inspection Hurdles

Your lender is going to order an appraisal, and it's non-negotiable. They need to confirm the property is actually worth what you're agreeing to pay for it. If that appraisal comes in low, you've got a problem. The bank will only lend based on the lower appraised value, not your contract price.

When that happens, you really only have three moves: go back to the seller and renegotiate the price, bring more cash to closing to cover the gap, or walk away from the deal (assuming you have an appraisal contingency in your contract).

While the appraisal protects the bank, the inspection protects you. A good inspector can uncover thousands of dollars in hidden problems that could torpedo your cash flow. If they find major issues, that inspection report becomes your best negotiating tool to get the seller to pay for repairs or drop the price.

This whole process is playing out in a red-hot rental market. Globally, real estate rentals were valued at around USD 2.91 trillion in 2025 and are projected to climb to USD 3.87 trillion by 2029. This boom is fueled by trends that are great for investors, like the rise of remote work and housing affordability issues that are keeping more people in the rental pool for longer. You can dig into more of these insights on ResearchAndMarkets.com.

A Few Common Questions I Always Get About Financing

As you start digging into the world of rental property financing, you're bound to run into a few specific questions. These are the details that often trip people up, but getting them right can be the difference between a great deal and a dead end. Let's walk through the big ones.

What's This "10 Financed Properties" Rule I've Heard About?

Sooner or later, every growing investor bumps into the 10 financed properties limit. It’s a real thing. This is a rule from Fannie Mae and Freddie Mac—the two giants who buy most of the conventional loans out there. They basically draw a line in the sand and say they won't back a loan for anyone who already has ten mortgages.

Why? It all comes down to risk. In their eyes, an investor juggling more than ten loans is a much bigger gamble. Once you hit that magic number, you can't just apply for a standard conventional loan anymore.

This is exactly where you have to get a little more creative. It's the moment you graduate to portfolio loans and other financing strategies. Lenders who keep their loans on their own books aren't tied to Fannie and Freddie's rules, and they're often happy to work with seasoned investors with a solid history.

How Is Getting a Loan for a Rental Different from My Home Mortgage?

Remember when you bought your own home? The bank was almost entirely focused on your personal salary and your existing debts. Financing a rental property is a whole different ballgame. The underwriting is way more intense because, at the end of the day, it's a business deal.

Here’s a look at what changes:

- Higher Bar for Credit: Forget the minimums for a primary home. For the best rates on an investment property, most lenders are looking for a credit score of 720 or higher.

- Serious Cash Reserves: You'll have to show you have plenty of cash left over after closing. We're often talking six months' worth of PITI (principal, interest, taxes, and insurance) payments for every single property you own.

- The Property Gets a Full Workup: The property itself goes under the microscope. The appraiser isn't just checking its value; they're determining its market rent potential to make sure it's a sound investment on its own.

Think of it this way: underwriting an investment property loan is a two-part exam. The lender needs to be confident that you can handle the payments, but they also need to believe the property can pull its own weight as a profitable asset.

Can I Actually Use the Rent to Help Me Qualify?

Absolutely—and this is one of the most powerful tools in your financing toolkit. Most lenders will let you count a portion of the property's future rental income toward your own income, which can be a huge help in meeting their debt-to-income (DTI) ratio requirements.

Here's how it typically works: the lender will look at the appraiser's estimate for fair market rent and then multiply it by 75%. That 25% discount is their way of accounting for vacancies and routine maintenance. The resulting number gets added to your income for qualification purposes.

For instance, if the appraiser says a property should rent for $2,000 a month, the lender will likely credit you with $1,500 ($2,000 x 0.75) in monthly income. For many investors, that extra boost is what makes the deal possible.

Stop drowning in spreadsheets and start making smarter, faster investment decisions. Property Scout 360 gives you the instant analysis and market data you need to find and vet profitable rental properties in minutes, not weeks. Discover your next deal today at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.