What Is Loan to Value Ratio A Guide for Real Estate Investors

Learn what is loan to value ratio, how it's calculated, and how it impacts your mortgage approval, interest rates, and overall investment strategy.

When you're trying to get a mortgage, lenders look at a lot of different numbers, but one of the most important is the Loan-to-Value (LTV) ratio. So, what is it?

Simply put, the LTV ratio is a percentage that compares the size of your loan to the appraised value of the property you want to buy. It’s the lender's go-to metric for quickly assessing how much risk they’re taking on by giving you a loan.

Understanding Your LTV Ratio

A good way to picture LTV is to think of a seesaw. On one end, you have the loan amount. On the other, you have the property's value. The LTV ratio just tells you how balanced—or unbalanced—that seesaw is.

If you make a big down payment, you're putting more of your own money on the value side, which lowers the loan amount and creates a lower LTV. But if you borrow most of the property's price, your loan side is much heavier, resulting in a higher LTV. This tells the lender that you have less of your own money, or "skin in the game," invested in the property.

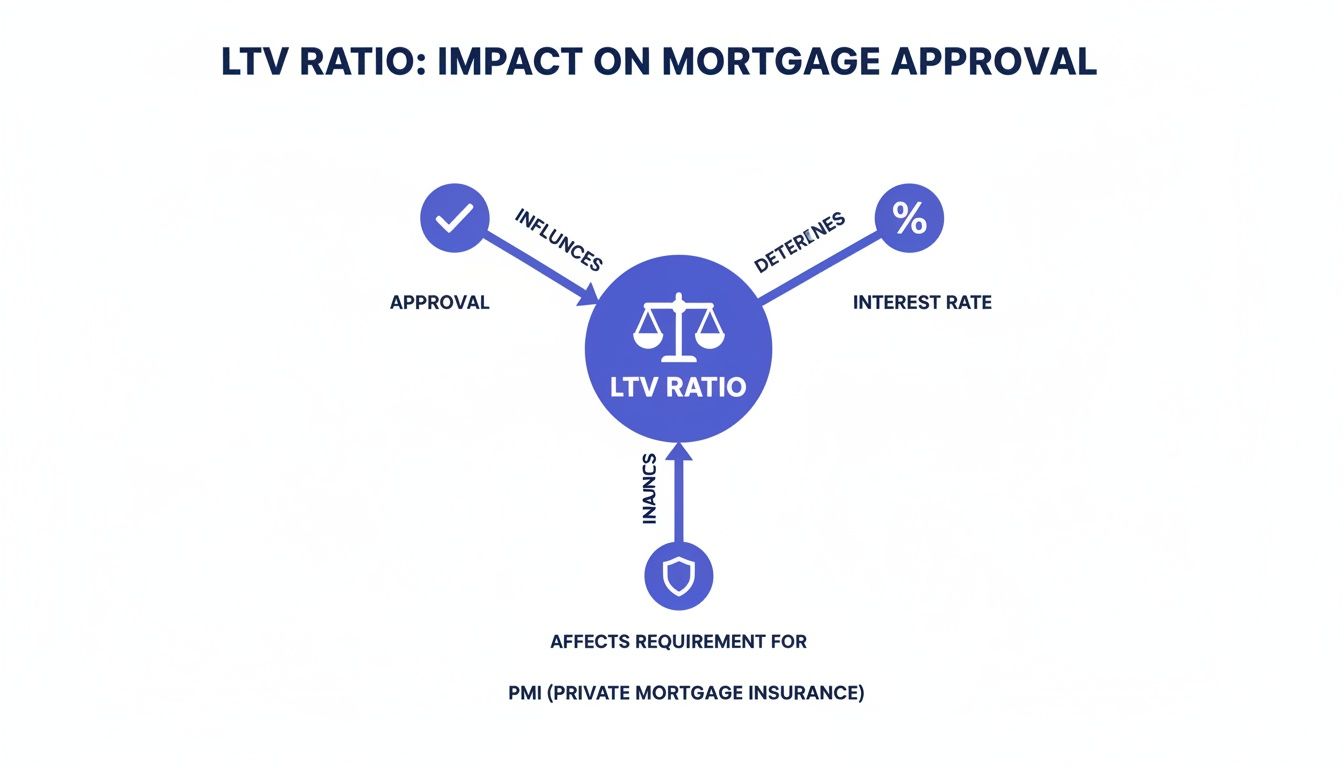

Why This Ratio Is a Big Deal

This single percentage has a huge ripple effect on your entire mortgage. It’s not just banker-speak; it directly shapes the terms of your loan and can impact your finances for years to come. For a lender, it's their primary way of gauging risk.

A higher LTV suggests that if you were to default on your loan, the lender has a smaller equity cushion to absorb potential losses from a foreclosure sale.

Because it’s all about risk, your LTV ratio plays a direct role in a few key parts of your financing:

- Loan Approval: Lenders have strict LTV limits. If your ratio is too high for their guidelines, your application might get rejected outright.

- Interest Rates: A lower LTV makes you a less risky borrower. To reward that, lenders will almost always offer you a better, lower interest rate.

- Mortgage Insurance: With a conventional loan, if your LTV is over 80%, you’ll almost certainly have to pay Private Mortgage Insurance (PMI), which adds an extra cost to your monthly payment.

For a quick summary, here's how to think about the core concepts of LTV.

LTV Ratio at a Glance

| Concept | What It Means for Investors |

|---|---|

| Basic Definition | The loan amount divided by the property's appraised value, shown as a percentage. |

| Risk Indicator | A high LTV (>80%) signals higher risk to the lender; a low LTV means less risk. |

| Down Payment Link | Your down payment is the inverse of your LTV. A 20% down payment equals an 80% LTV. |

| Financial Impact | Directly influences loan approval, interest rates, and the need for private mortgage insurance (PMI). |

Wrapping your head around the LTV ratio is a fundamental step for anyone serious about real estate. Whether you're a first-time homebuyer or a seasoned pro analyzing different real estate use cases, mastering this concept gives you more control over your financing and sets you up for smarter investment decisions.

How to Calculate LTV with Step-by-Step Examples

Running the numbers on your Loan-to-Value (LTV) ratio is simpler than it sounds. Once you get the hang of it, you start to see every deal the way a lender does, instantly sizing up the risk and opportunity.

The entire calculation hinges on just two key figures: how much you need to borrow and what the property is officially worth according to an appraiser. And here’s a crucial tip: lenders will always base their calculation on the lower of the two—either the purchase price or the appraised value. It's their safety net.

The LTV Formula:

LTV = (Total Loan Amount ÷ Appraised Property Value) x 100

Let's walk through a couple of real-world scenarios that you'll definitely encounter as an investor.

Example 1: The Standard Rental Purchase

You’ve found a promising duplex with a list price of $320,000, and the appraisal comes back right at that number. Perfect. To get a conventional investment loan, your lender requires a 20% down payment.

- Appraised Value: $320,000

- Down Payment: $64,000 (which is 20% of $320,000)

- Loan Amount: $256,000 ($320,000 - $64,000)

Now, let's plug those numbers into our formula:

- Divide the Loan Amount by the Value: $256,000 ÷ $320,000 = 0.80

- Convert to a Percentage: 0.80 x 100 = 80% LTV

That 80% LTV is a massive milestone. For conventional loans, it's the magic number that lets you sidestep costly Private Mortgage Insurance (PMI), which is why so many savvy investors aim for it.

Example 2: The BRRRR Strategy

Now, let's look at the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method, where LTV is calculated against a future value. Imagine you snag a fixer-upper for $150,000, put $50,000 into renovations, and the property's After Repair Value (ARV) appraises for $280,000.

Your goal is a cash-out refinance to pull your initial investment back out and fund your next project. On a refi, lenders are a bit more conservative and might cap the loan at 75% of the ARV.

- Appraised Value (ARV): $280,000

- Maximum Loan Amount: $210,000 (which is 75% of $280,000)

This new loan puts you at a 75% LTV. The $210,000 you pull out completely covers your initial costs ($150k purchase + $50k rehab = $200k) and even leaves you with $10,000 in your pocket. This is how understanding what is loan to value ratio in the context of ARV becomes the engine for scaling your rental portfolio.

Why LTV Is Your Mortgage Gatekeeper

Think of your Loan-to-Value (LTV) ratio as the very first number a lender looks at on your application. It's their go-to metric for measuring risk. In simple terms, it's a gatekeeper that decides if you get approved, what interest rate you'll land, and whether you'll have to pay extra fees. The logic is simple: a lower LTV means you have more skin in the game, which makes you a much safer bet in the lender's eyes.

This isn't just some modern banking quirk; it’s a lesson learned the hard way. Before the 2008 financial crisis, lending standards were incredibly lax, and some loans were approved with dangerously high LTVs. That over-leveraging poured fuel on the fire and made the market crash that much worse. Today’s stricter LTV rules are a direct result of that meltdown, put in place to build a more stable and resilient housing market.

How LTV Shapes Your Loan Terms

Your LTV ratio has a direct and powerful impact on three key parts of your mortgage. Even a small shift in this percentage can end up saving you tens of thousands of dollars over the life of the loan. It’s all part of the complex mortgage puzzle, where different players like title companies involved in real estate transactions play a crucial role in verifying the property's value and legal ownership.

Here’s exactly how LTV influences your financing deal:

- Mortgage Approval: Lenders have hard limits on LTV. If the loan you’re asking for pushes you past their threshold, your application could be rejected outright before it ever gets to an underwriter.

- Interest Rates: It’s a classic risk-reward scenario. Borrowers with a lower LTV almost always get offered better interest rates. For example, an LTV of 75% could easily secure you a lower rate than someone with an 85% LTV because, from the lender’s perspective, you’re less of a risk.

- Private Mortgage Insurance (PMI): This is a big one for conventional loans. If your LTV is higher than 80%, you’ll almost certainly be required to pay PMI. This insurance protects the lender—not you—and adds a frustrating extra cost to your monthly payment until you build enough equity to get your LTV down.

LTV Requirements Across Different Loans

Not all loans are built the same, and LTV requirements can change dramatically from one loan type to another. This is especially important for real estate investors who need to know how to finance a rental property with the most suitable loan product.

Your down payment is the most powerful lever you have for controlling your LTV. By putting more money down, you directly lower your LTV ratio, which opens the door to better loan terms and cuts your long-term borrowing costs.

Here’s a quick look at the typical LTV limits for common loans:

- Conventional Loans: The gold standard here is an 80% LTV to avoid PMI, which translates to the well-known 20% down payment.

- FHA Loans: These government-backed loans are designed to make homeownership more accessible, allowing for a very high LTV of up to 96.5%.

- VA Loans: An incredible benefit for eligible veterans and service members, VA loans can go all the way up to 100% LTV, meaning you can often buy a home with no down payment at all.

When you understand how to manage your LTV, you stop being just another loan applicant. You become a savvy strategist, putting yourself in the best possible position to lock in the most favorable financing available.

Going Beyond LTV with CLTV and TLTV

While LTV is the headline number for any single loan, it doesn't always tell the whole story. Lenders need a wider lens, especially when a property has more than one loan attached to it—a common scenario for savvy investors using creative financing.

To get a complete picture of a property's total debt load, lenders rely on two closely related metrics: Combined Loan-to-Value (CLTV) and Total Loan-to-Value (TLTV). Think of them as LTV's more comprehensive cousins. They reveal the true extent of leverage on an asset.

So, What's CLTV?

The CLTV ratio looks at your primary mortgage plus any other existing loans secured by the property. This includes second mortgages or the amount you've already drawn from a Home Equity Line of Credit (HELOC). It's a snapshot of the total current debt.

Let's break it down with an example. Say your property is valued at $500,000. You have a first mortgage of $350,000 and a second mortgage of $50,000.

- Total Loan Balances: $350,000 + $50,000 = $400,000

- CLTV Calculation: ($400,000 / $500,000) = 80% CLTV

This number is crucial when you're refinancing or applying for a new loan because it shows the lender how much equity is actually left after all existing debts are accounted for.

And How Does TLTV Differ?

Total Loan-to-Value takes this a step further. It calculates the risk based on the maximum potential debt a property could carry. The TLTV includes your primary mortgage and the full credit limit of any lines of credit, like a HELOC, whether you've used the money or not.

A lender uses TLTV to stress-test their risk. They're asking, "What's our exposure if the borrower maxes out every available line of credit?" This "worst-case scenario" number heavily influences their decision.

This focus on total exposure is why understanding LTV and its relatives is so important. As the diagram below shows, these metrics sit at the very center of a lender's decision-making process, impacting everything from your approval odds to your interest rate.

Comparing Leverage Ratios LTV vs CLTV vs TLTV

To keep these terms straight, it helps to see them side-by-side. Each metric gives a lender a slightly different perspective on the risk associated with your property's financing.

| Metric | What It Includes | When It's Used |

|---|---|---|

| LTV | A single loan amount (usually the primary mortgage). | When underwriting a new primary mortgage or a simple refinance. |

| CLTV | The primary mortgage plus the drawn balance of all other loans (e.g., HELOCs). | When applying for a second mortgage or refinancing with multiple existing loans. |

| TLTV | The primary mortgage plus the full credit limit of all other lines of credit. | To assess the maximum potential risk, especially when approving a new HELOC or other lines of credit. |

Ultimately, LTV, CLTV, and TLTV all work together to paint a full picture of your financial position. Mastering these ratios is just as critical as understanding other key investment metrics. If you’re looking to dive deeper, you should also check out our guide on what is DSCR in real estate.

Using LTV Thresholds to Your Advantage

Knowing your loan-to-value ratio is one thing. Actively using it to your advantage is a whole different ballgame.

For smart real estate investors, LTV isn't just a number you calculate once and forget about. It's a strategic lever you can pull to unlock better financing, slash your costs, and grow your portfolio faster. Lenders have specific LTV thresholds that act like gates; get your numbers right, and you get access to much better terms.

By knowing where these gates are, you can structure your deals to walk right through them. The most famous threshold is the 80% LTV mark. For conventional loans, staying at or below this magic number means you get to skip Private Mortgage Insurance (PMI)—a costly premium that only protects the lender, not you.

Key LTV Thresholds for Investors

Beyond just avoiding PMI, other LTV benchmarks are crucial for specific investment strategies. Each one signals a different level of risk to a lender, and hitting the right target can be the difference between a profitable deal and a dud.

- 75% LTV: Many investors consider this the sweet spot for cash-out refinances on investment properties. Lenders get a bit more conservative when you’re pulling equity out of a property. Coming in at a 75% LTV shows them you still have significant skin in the game, which often secures you the best rates available.

- 90% LTV: You won't see this often for investment properties, but some specialized loan products might go this high. Be prepared for a trade-off, though. These deals almost always come with higher interest rates and much stricter qualification requirements.

When you intentionally manage your LTV, you stop being a passive loan applicant and become an active deal-shaper. You’re directly influencing the terms you get, whether it's through a larger down payment upfront or a timely refinance after the property appreciates.

You can also use a platform like Property Scout 360 to game out how different LTV scenarios will affect your long-term returns. The screenshot below shows how the platform’s financial analysis tools can model these different outcomes for you.

This kind of detailed breakdown lets you see exactly how a lower LTV can boost your cash flow and overall profit by shrinking your monthly mortgage payment.

The Bigger Picture: Global Trends and Your Strategy

LTV standards aren't set in a vacuum. They’re heavily influenced by the broader economy and government regulations. In major markets around the world, LTV ratios are basically a health check for the housing market. For example, after the 2008 crash, regulators in the UK and New Zealand put strict caps on high-LTV lending to stop housing bubbles from forming again—a painful lesson learned from the U.S. crisis. You can discover more insights about these debt trends on jll.com.

What does this mean for a U.S. investor? It means that while aiming for an 80% LTV is a solid goal, paying attention to the larger economic climate can help you anticipate when lending standards might tighten or loosen.

It also highlights why building equity is so powerful. More equity means a lower LTV, which acts as a buffer, insulating your portfolio from market swings. This concept becomes even more important when you compare LTV to other key metrics. On that note, you might also find our guide on the rent-to-value ratio useful.

Common Questions About LTV

Alright, you've got the basics down. You know what LTV is and how to calculate it. But let's be honest, the real world is where the rubber meets the road. Investors always have those nagging "what if" questions that pop up during a deal.

This is your quick-fire guide to answer those common questions. Think of it as a cheat sheet to help you handle real-life financing scenarios with a bit more confidence.

Does a Lower LTV Ratio Guarantee Loan Approval?

In a word, no. While a low LTV makes you a much more attractive borrower, it’s not a golden ticket to loan approval. Lenders look at your entire financial picture, and a great LTV is just one part of that story.

Think of your loan application as a package. A low LTV shows you have skin in the game, which reduces the lender's risk. But they're also going to dig into your:

- Credit Score: They need to see a solid track record of you paying your bills on time. This is non-negotiable.

- Debt-to-Income (DTI) Ratio: Can you actually afford this new mortgage payment on top of your other debts? Lenders need proof you aren't overextended.

- Cash Reserves: What happens if you lose a tenant or face a big repair? Lenders want to see you have enough cash stashed away to cover mortgage payments for a few months.

A fantastic LTV simply can't rescue a bad credit score or a DTI that’s through the roof. Every piece has to fit together to get the green light.

How Does a Property Appraisal Affect My LTV?

The appraisal is everything. It's the independent, third-party valuation that forms the very foundation of your LTV calculation. Lenders don't care as much about what you agreed to pay; they care about what a professional appraiser says the property is actually worth.

Here’s the critical part: lenders will always use the lower of the two numbers—the purchase price or the appraised value—to calculate your LTV.

Let’s say you go under contract to buy a property for $400,000. But the appraisal comes back at only $380,000. The lender will base your loan amount on that $380,000 figure. This "appraisal gap" instantly changes your math and can force you to bring a lot more cash to the closing table to hit your lender's required LTV.

Can My LTV Ratio Change After Closing?

Absolutely. Your LTV is not a static number carved in stone on closing day. It’s a living metric that will (hopefully) change for the better over the life of your loan.

Your LTV drops in two main ways, both of which are about building your equity:

First, every single mortgage payment you make chips away at your principal loan balance. As that balance goes down, your LTV does too. Second, as the property appreciates in value—whether from market forces or your own smart renovations—your LTV also falls.

This is why your LTV is so important long-term. A shrinking LTV is what opens the door to future opportunities, like refinancing to a better rate, dropping PMI, or pulling out cash with a HELOC to buy your next deal.

What Is a Good LTV for an Investment Property?

When you’re buying an investment property, get ready for stricter rules. Lenders see an investment property as a slightly higher risk than the home you live in, so they tighten up the LTV requirements.

For an investment property, a "good" LTV is generally 75% or lower.

Most conventional lenders will want to see a down payment of at least 20-25%, which puts you in that 75-80% LTV ballpark from day one. If you can push that LTV down to 75% or less, you’ll often get access to the best interest rates and terms, which directly boosts your cash flow and makes your investment that much stronger.

Ready to stop guessing and start making data-driven investment decisions? Property Scout 360 eliminates the guesswork by letting you model different LTV scenarios across various loan products instantly. See how a small change in your down payment can impact your cash flow, ROI, and long-term wealth. Find your next profitable investment at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.