Debt Service Coverage Ratio Real Estate: An Investor Guide

Discover the debt service coverage ratio real estate with our concise guide. Learn the DSCR formula, lender criteria, and how to improve your numbers.

When a lender looks at a potential investment property, they're really asking one simple question: can this property pay its own bills? The metric they use to answer this is the Debt Service Coverage Ratio, or DSCR.

It's a straightforward calculation that divides the property's Net Operating Income (NOI) by its total mortgage payments for the year (Total Debt Service). If the result is greater than 1.0, the property brings in enough money to cover its debt. The higher the number, the healthier the investment.

What DSCR Means for Your Real Estate Investment

Think of the debt service coverage ratio real estate investors use as a quick stress test for a property's finances. It's the primary language lenders speak, and it cuts right to the heart of whether an investment is viable on its own.

I like to use a simple bucket analogy. Imagine your property's annual income is the water filling a bucket, and your total mortgage payments are a hole in the bottom. The DSCR tells you how much water is left over after the "leak" is accounted for. A nice overflow means you have strong positive cash flow. But if the water level is just barely covering the hole, you're in a risky spot.

The Financial Safety Cushion

At its core, the DSCR is your property’s financial safety net. A bigger ratio means you have a more substantial buffer to handle unexpected vacancies or a sudden roof repair without missing a loan payment.

Let’s break down what the numbers actually mean:

- A DSCR of 1.0x means your Net Operating Income (NOI) is a perfect match for your debt payments. You’re breaking even, with absolutely no room for error.

- A DSCR of 1.25x is a common minimum for most lenders. It shows the property generates 25% more income than it needs to cover the mortgage, which is a decent cushion.

- A DSCR of 1.50x is where you want to be. This signals a 50% income surplus, making the property look like a very stable, low-risk investment to a bank.

A strong DSCR isn't just a number—it's your key to unlocking better loan terms, securing financing, and proving your investment's stability from day one. Understanding this metric is the first step toward building a resilient and profitable real estate portfolio.

Why Lenders Prioritize DSCR

Lenders zero in on DSCR because it isolates the property's ability to pay back the loan using its own income—completely separate from your personal finances. A solid DSCR proves the asset can stand on its own two feet.

This is exactly why getting your numbers right is so critical. When you learn how to calculate cash flow on a rental property, you gain direct control over your DSCR and can build a much stronger case when you walk into a bank.

Ultimately, a good DSCR does more than just get you a "yes" on a loan application. It validates your entire investment strategy, confirming that the property is financially sound. For anyone serious about building long-term wealth in real estate, this insight is the foundation for making smarter decisions that minimize risk and boost returns.

Calculating Your Property's DSCR Step by Step

Getting a handle on the Debt Service Coverage Ratio (DSCR) formula is the first step to really understanding a deal's potential. At its core, the math is simple: you just divide a property's Net Operating Income (NOI) by its annual mortgage payments.

DSCR = Net Operating Income (NOI) / Total Debt Service

But as any seasoned investor knows, a formula is only as good as the numbers you plug into it. Let's walk through how to calculate each part correctly so you can run the numbers with confidence on any property that crosses your desk.

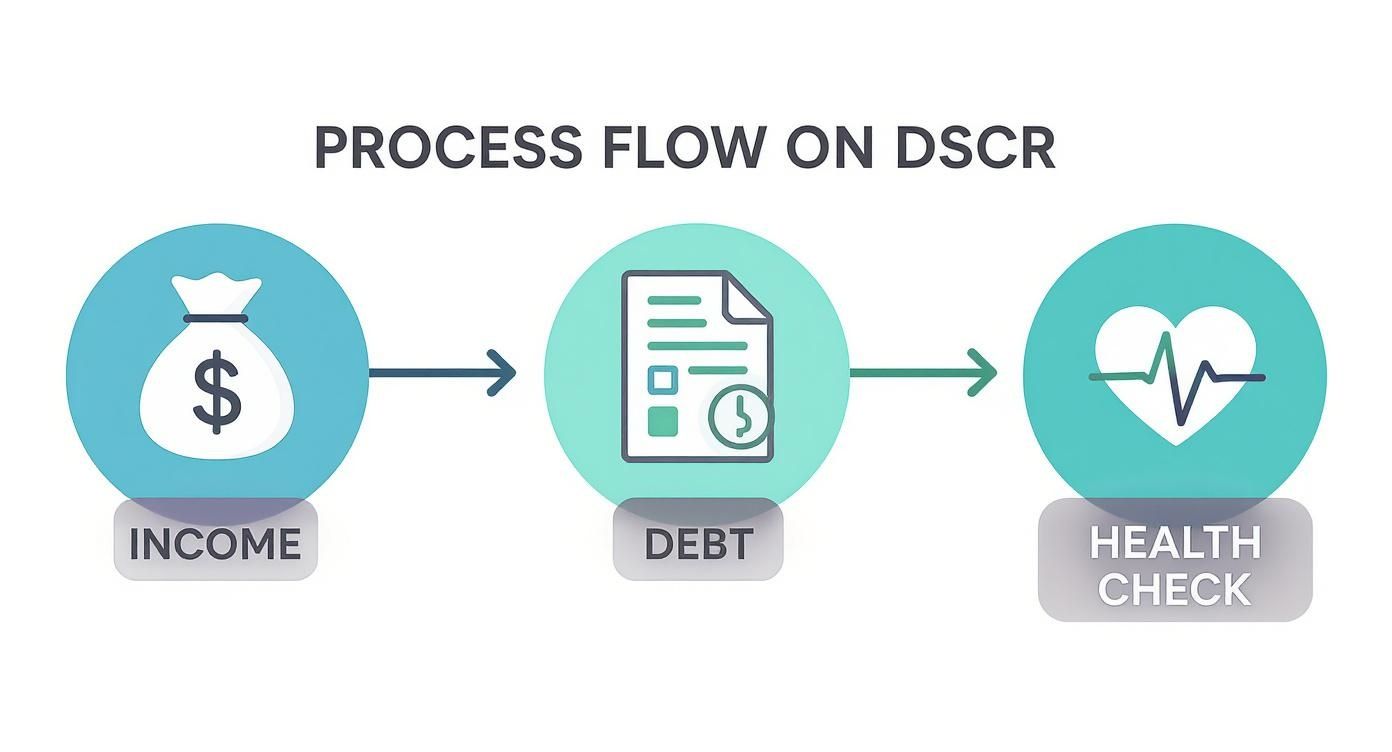

This process is all about seeing if the income can truly support the debt, which is a fundamental health check for any investment property.

As the diagram shows, it's a three-stage process: income comes in, debt gets paid, and only then can you assess the financial health of the asset.

Step 1: Calculate Your Net Operating Income

First up is the Net Operating Income, or NOI. This is your property's total income after you've paid all the bills to keep it running—but before you've paid the mortgage or income taxes.

To get your NOI, you'll start with the property's gross income and then subtract all your operating expenses.

- Gross Operating Income (GOI): This is all the rent you could possibly collect in a year, minus a realistic amount for vacancies and tenants who don't pay. Don't fall into the trap of using a perfect, best-case scenario number here.

- Operating Expenses: These are all the costs required to keep the lights on and the property in good shape. Think property taxes, insurance, routine maintenance, property management fees, utilities, and any HOA fees.

It’s just as important to know what not to include. Things like depreciation, major capital expenditures (like replacing a roof), and loan interest are kept out of the NOI calculation.

NOI = Gross Operating Income - Operating Expenses

You can think of NOI as the property's raw earning power. It tells you exactly how much cash the building itself generates from its day-to-day business of renting out space, completely separate from its financing.

Step 2: Determine Your Total Debt Service

The second part of the equation, Total Debt Service, is much easier to pin down. It’s simply the total of all your mortgage payments—both principal and interest—over a full year.

This number is usually fixed, so you can find it on your loan amortization schedule or just multiply your monthly mortgage payment by 12.

Lenders are laser-focused on this ratio. Today, most commercial lenders want to see a minimum DSCR of 1.25. This means the property needs to generate at least 25% more income than what’s needed to cover its debt payments. This became a common benchmark after the 2008 financial crisis as a way for banks to build in a safety buffer.

A DSCR below 1.0 is a major red flag, showing a property isn't even making enough to pay its mortgage. On the flip side, a DSCR of 1.5 shows it's bringing in 50% more income than needed—a sign of a very healthy investment. You can read more about these industry benchmarks and see how they can affect your ability to get financing.

A Practical DSCR Calculation Example

Let's see how this works with a real-world example. Imagine you’re looking at a small multi-family building.

Income & Expenses:

- Annual Gross Potential Rent: $80,000

- Vacancy Allowance (5%): -$4,000

- Gross Operating Income (GOI): $76,000

- Total Operating Expenses (Taxes, Insurance, Repairs): -$26,000

- Net Operating Income (NOI): $50,000

Debt Service:

- Monthly Mortgage Payment (Principal & Interest): $3,500

- Total Annual Debt Service: $3,500 x 12 = $42,000

Now, we just plug those numbers into our formula:

DSCR = $50,000 (NOI) / $42,000 (Total Debt Service) = 1.19x

The DSCR for this property is 1.19. This tells us it makes enough money to pay its debt and has a 19% cushion left over. While it's cash-flow positive, that 1.19 is just shy of the 1.25 minimum many lenders look for. In one simple number, you get a powerful snapshot of the deal's financial strength.

What Lenders Consider a Good DSCR

While the formula for the debt service coverage ratio real estate investors use is simple math, what lenders actually consider a "good" number is a different story. You might think a DSCR of 1.0x is a passing grade—after all, it means income perfectly covers the debt.

But to a lender, a 1.0x DSCR is like walking a tightrope without a safety net. It leaves zero room for error. A single unexpected repair or a slow month for leasing could instantly throw the property into negative cash flow, putting the loan at risk. That's why you'll almost never get financing with a DSCR of exactly 1.0x.

The Industry Standard The 1.25x Benchmark

Lenders need to see a buffer. They're looking for a financial cushion that protects their investment from the real-world chaos of owning property. This is why the industry has largely landed on a minimum DSCR benchmark of 1.25x.

This magic number tells a lender that the property generates 25% more income than it needs to cover its debt payments. It’s not arbitrary; it's a calculated safety margin. This surplus cash proves the property can handle a hit—like a drop in rent or a spike in utility costs—and still easily make its mortgage payment.

A DSCR of 1.25x or higher signals to a lender that the investment is not just surviving, but thriving. It proves the asset is a financially resilient operation, capable of weathering minor storms without defaulting on the loan.

Think of it this way: a lender is your financial partner in the deal. They need to know you’ve built enough breathing room into your numbers to handle whatever comes your way. Getting over that 1.25x hurdle is often the first and most important step in getting your loan approved.

How Property Type and Market Conditions Shift Expectations

Of course, the 1.25x benchmark isn't set in stone. The exact DSCR a lender wants to see can change based on the perceived risk of the property type and its location. Lenders are ultimately in the business of managing risk, so they adjust their standards accordingly.

- Stable Assets (Multifamily): Properties with highly predictable income, like apartment buildings, are a lender's favorite. They typically qualify with the standard 1.25x DSCR because tenant turnover is staggered and demand is usually consistent.

- Volatile Assets (Hotels or Self-Storage): On the other hand, properties with more fluctuating revenue, like hotels or self-storage facilities, are seen as riskier. Their income is more sensitive to economic shifts, so a lender might demand a higher DSCR of 1.40x or more to feel comfortable.

The local market is a huge factor, too. A property in a booming city with a long waitlist of renters might get a pass with a slightly lower DSCR. An asset in a town with a shaky economy, however, will face much tougher standards.

To make this crystal clear, here’s a breakdown of how lenders typically view different DSCR ranges.

Lender DSCR Requirements and Implications

This table illustrates common DSCR benchmarks, what they signify to lenders, and the likely impact on loan approval and terms for real estate investors.

| DSCR Range | Lender's Interpretation | Likely Loan Outcome |

|---|---|---|

| Below 1.0x | Negative Cash Flow. The property is losing money and cannot cover its debt obligations. | Loan application will almost certainly be denied. |

| 1.0x - 1.15x | High-Risk. Extremely thin margin for error, vulnerable to any financial stress. | Unlikely to be approved by most traditional lenders. |

| 1.15x - 1.25x | Borderline. May be considered, but often requires compensating factors like a low LTV or strong borrower. | Approval is possible but not guaranteed; may come with less favorable terms. |

| 1.25x or Higher | Low-Risk & Healthy. The property has a solid financial cushion to absorb unexpected costs. | Strong candidate for approval with competitive interest rates and terms. |

At the end of the day, a higher DSCR gives you more power. It doesn't just boost your odds of getting the loan; it puts you in a position to negotiate better interest rates, higher loan amounts, and a much smoother underwriting process. A strong DSCR proves your investment is a solid bet for everyone involved.

Using DSCR to Make Smarter Investment Decisions

While lenders live and breathe the debt service coverage ratio in real estate, savvy investors know its true value goes far beyond just getting a loan approved. When you stop seeing DSCR as just a financing hurdle, it transforms into a powerful lens for assessing the genuine financial health and cash-flow potential of a property.

By making DSCR analysis a core part of your due diligence, you can graduate from hopeful guesses to data-backed decisions that protect your capital. It’s a clean, standardized metric that lets you compare wildly different opportunities on an even playing field.

Comparing Investment Opportunities

Let's say you're looking at two similar duplexes. Property A has a lower price tag but also brings in less rent, giving it a DSCR of 1.20x. Property B costs more upfront, but its stronger rental income pushes its DSCR to a healthier 1.45x.

At first glance, Property A might seem like the bargain. But that 1.20x ratio reveals a dangerously thin safety margin. One unexpected vacancy or a costly repair could easily erase your cash flow for the month. On the other hand, Property B’s robust 45% income cushion makes it a far more stable investment, even with the higher initial cost. This is where DSCR truly shines, exposing hidden risks and strengths that a price tag alone can't tell you.

This kind of analysis works beautifully alongside other key metrics. For another way to compare deals, check out our guide on the internal rate of return calculator for real estate.

When you compare the DSCR of different properties, you’re not just crunching numbers; you’re measuring their ability to withstand financial pressure. The property with the higher DSCR is almost always the one better equipped to deliver consistent, reliable returns.

Stress-Testing a Potential Investment

DSCR is also your best friend when it comes to stress-testing a deal against the unknown. Before you ever sign on the dotted line, you can model how a property’s financials will hold up when things don't go exactly as planned.

You can ask, "What if?"

- Rising Interest Rates: What does the DSCR look like if my ARM adjusts upward in five years?

- Increased Vacancy: What happens if the local market softens and my vacancy rate jumps from 5% to 10%?

- Higher Operating Expenses: If property taxes or insurance premiums spike by 15%, does the deal still cash flow?

Running these scenarios helps you find a property's breaking point. If a small change sends the DSCR plummeting below that critical 1.25x mark, you know the investment lacks the resilience you need. This proactive analysis is what separates seasoned investors from speculators—it prepares you for market shifts and helps you sidestep deals that are liabilities in disguise.

A Powerful Indicator of Credit Risk

Don't just take our word for it—the data backs this up. The multifamily sector offers a clear lesson in DSCR's predictive power. Since the Great Recession, stricter underwriting standards have pushed the average DSCR for multifamily loans up by 34%, climbing from 1.6x in 2009 to 2.15x in recent years.

The result? Far fewer defaults. Loans with a DSCR below 1.0x (meaning they aren't generating enough income to cover their debt) have default rates hovering around 3.3%. Meanwhile, newer properties built since 2008 with stronger financials show default rates of just 1.33%. This historical data confirms it: a higher DSCR is one of the most reliable indicators of lower risk and better loan performance. You can read more about this trend in this multifamily property credit risk analysis.

Actionable Strategies to Improve Your Property's DSCR

A low debt service coverage ratio in real estate can feel like hitting a brick wall, stopping you from refinancing or landing new loans. The good news is that it’s not set in stone. With a few strategic moves, you can directly influence your property’s financial health and make it a much more attractive prospect for lenders.

Think of the DSCR formula—Net Operating Income divided by Debt Service—as a couple of levers you can pull. To get that ratio up, you have two main options: push your NOI higher or pull your debt service down. Working on both can turn a property on the bubble into a solid, bankable asset.

Boost Your Net Operating Income

Your Net Operating Income (NOI) is the engine driving your property's cash flow. The most sustainable way to improve your DSCR is to make that engine more powerful and efficient. Even small, gradual tweaks here can have a surprisingly big impact over time.

Here are four solid ways to get your NOI moving in the right direction:

- Implement Strategic Rent Increases: Take a hard look at your rent roll regularly to make sure you're keeping pace with the market. A simple 3-5% annual bump can significantly boost your income without chasing away good tenants.

- Add Value-Add Amenities: Small upgrades can justify bigger rents. Things like in-unit laundry, smart thermostats, or even a designated parking spot can command a premium, attracting better, longer-term tenants in the process.

- Minimize Vacancy Rates: An empty unit is a hole in your pocket, directly draining your NOI. Keep your tenants happy with great service and quick maintenance. A positive community feel goes a long way in reducing turnover and the marketing costs that come with it.

- Cut Operating Expenses: Go through your expense reports with a fine-toothed comb. Can you renegotiate vendor contracts? Appeal your property tax assessment? Or maybe invest in energy-efficient upgrades like LED lighting and low-flow toilets to cut down on utility bills?

Example in Action:

Let’s say your property’s NOI is $50,000 and your annual debt is $42,000. That gives you a DSCR of 1.19x—a little too close for comfort for most lenders. But by raising rents just a bit and trimming utility costs, you manage to add $5,000 to your NOI, bringing it to $55,000.New DSCR = $55,000 / $42,000 = 1.31x

Just like that, a few smart adjustments have pushed your property well past that lender-friendly 1.25x benchmark.

Reduce Your Total Debt Service

While growing your income is key, the other side of the DSCR equation—your total debt service—offers a faster, more direct path to a better ratio. Lowering your annual mortgage payments gives you immediate breathing room and can pump up your DSCR with a single transaction. This is a particularly powerful strategy when interest rates are working in your favor.

The main play here is to renegotiate your loan terms to shrink your yearly payments.

1. Refinance for a Lower Interest Rate

If rates have dropped since you got your original loan, refinancing can be a game-changer. Even shaving off a fraction of a percentage point can translate into thousands of dollars in annual savings.

2. Extend the Amortization Period

Another refinancing tactic is to stretch out your loan's amortization period. For example, extending a loan from 20 years to 30 years will drop your monthly payments, reduce your annual debt service, and give your DSCR an instant lift.

In today's market, keeping a healthy DSCR is more important than ever. The commercial real estate world is facing new pressures on cash flow, especially in overbuilt metro areas. In a telling sign, U.S. banks recently saw problem loans spike to $55 billion, a fourfold jump in just two years. This shows the real strain on investors, especially those who underwrote deals with razor-thin DSCRs between 1.00 and 1.10. That kind of minimal buffer leaves no room for error when rent growth stalls, which is exactly why lenders have good reason to stick to the 1.25x DSCR standard as a crucial safety net. You can find more details on how DSCR standards have evolved to protect lenders and borrowers.

By actively managing both your income and your debt, you build a much more resilient investment portfolio. A strong debt service coverage ratio in real estate isn't just a number for a loan application; it's the vital sign of a healthy, profitable property that can weather market storms and deliver reliable returns for years to come.

Common Questions About DSCR in Real Estate

Once you get the hang of the formulas, the real questions start popping up when you're looking at actual deals. Let's tackle some of the most common points of confusion I see from both new and seasoned investors. The goal here is to clear things up so you can walk into your next lender meeting with confidence.

Can I Get a Real Estate Loan with a DSCR Below 1.25?

While 1.25x is the benchmark everyone talks about, it’s not set in stone. It's absolutely possible to get a loan with a lower DSCR, but you’ll need to make the deal look attractive in other ways. Think of it as a balancing act—if the cash flow is a little light, you need to add weight somewhere else to reduce the lender's risk.

Lenders might give the green light on a DSCR between 1.15x and 1.24x if you bring something else to the table:

- Low Loan-to-Value (LTV) Ratio: Putting more skin in the game always helps. If you come in with a huge down payment, say 40% or more, the lender has far less at risk. That big equity cushion can make them feel much safer about a tighter cash flow.

- A Strong Borrower Profile: If you have a great credit score, plenty of cash reserves, and a solid track record of successful investments, you look like a much safer bet. This personal strength can help make up for a property with a borderline DSCR.

- High-Growth Markets: Is the property in a hot neighborhood where rents are climbing and demand is strong? A lender might be more willing to bend the rules, betting that rising rents will naturally push the DSCR up in the near future.

It's also worth noting that specialized "DSCR loans" are built for this. They focus almost entirely on the property’s income, not your personal finances. They might approve a lower DSCR, but that flexibility usually comes with a slightly higher interest rate or more fees.

How Is DSCR Different from Cap Rate or Cash on Cash Return?

As an investor, you have a whole toolkit of metrics, and it's critical to know which tool to grab for which job. DSCR, Cap Rate, and Cash on Cash Return each tell a unique and vital part of a property's financial story. They aren't interchangeable—they work together to give you the full picture.

Think of them this way: DSCR is the lender's metric for safety, Cap Rate is the investor's metric for comparison, and Cash on Cash Return is the investor's metric for personal performance.

Here’s a quick rundown of what each one is for:

| Metric | Formula | Primary Purpose | Who Cares Most? |

|---|---|---|---|

| DSCR | NOI / Total Debt Service | Measures if the property can actually pay its mortgage. | The Lender |

| Cap Rate | NOI / Property Value | Measures the raw, unleveraged return to compare different properties. | The Investor (for analysis) |

| Cash on Cash | (NOI - Debt Service) / Total Cash Invested | Measures the return on the actual money you pulled out of your pocket. | The Investor (for ROI) |

A high Cap Rate might get you excited about a deal, but a low DSCR will tell you it's a non-starter for financing. A good DSCR gets you the loan, but a weak Cash on Cash Return might mean your money could be working harder for you elsewhere.

What Common Mistakes Do Investors Make When Calculating DSCR?

Getting your DSCR right is non-negotiable. So many investors make simple mistakes that inflate the number, giving them a dangerously false sense of security. If you get this wrong, you're not just misleading the bank; you're fooling yourself about the deal's stability.

Here are the top three blunders I see all the time:

- Underestimating Operating Expenses: It's tempting to be optimistic, but you have to account for everything. This means budgeting for vacancies, routine repairs, property management, and bigger capital expenditures (CapEx) down the road, like a new roof or HVAC system. Forgetting these will make your NOI look much better than it really is.

- Using Gross Potential Rent: Never, ever use the "perfect world" rent number where every unit is occupied all year. You have to subtract a realistic amount for vacancy and credit loss to get your true Gross Operating Income. A 5-8% vacancy factor is a safe place to start.

- Ignoring Part of the Debt Service: Make sure your calculation uses the total annual debt payment, which includes both principal and interest (P&I). A surprising number of people only factor in the interest, which dramatically skews the number and hides the property's true debt burden.

Does My Personal Income Matter for a DSCR Loan?

This is where DSCR-based financing really shines. For a true DSCR loan, your personal income—from your W-2 job or small business—is not the main thing lenders look at. In this scenario, the property is essentially applying for the loan on its own merits.

The logic is simple: if the property's Net Operating Income can cover the mortgage with a healthy buffer (that 1.25x DSCR or higher), the deal stands on its own. This is a complete game-changer for self-employed investors or anyone looking to scale a portfolio without hitting a wall with their personal debt-to-income ratio.

But that doesn't mean your personal finances are totally off-limits. While the lender won't ask for tax returns or pay stubs, they will almost certainly check:

- Your Credit Score: A strong credit history is still a must-have.

- Liquidity: They'll want to see that you have the cash on hand for the down payment, closing costs, and a few months of mortgage payments in reserve.

- Experience: Some lenders give better terms to investors who have been around the block a few times.

At the end of the day, the DSCR loan shifts the spotlight from you to the asset, letting you make decisions based on the quality of the investment itself.

Ready to stop guessing and start making data-driven investment decisions? Property Scout 360 eliminates manual spreadsheets by providing instant calculations for DSCR, cash flow, ROI, and more on any U.S. property. Find and analyze your next profitable rental in minutes at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.