What Is The BRRRR Method A Guide to Scaling Your Real Estate Portfolio

Wondering what is the BRRRR method? Discover how to buy, rehab, rent, refinance, and repeat to build your real-estate portfolio with less of your own capital.

If you’ve been around real estate investing for a while, you’ve probably heard people talking about the BRRRR method. It’s more than just a catchy acronym—it’s a powerful strategy for building a rental portfolio by recycling the same pot of money over and over again.

The letters stand for Buy, Rehab, Rent, Refinance, Repeat. At its heart, this is a five-step system that lets you buy a property, force its value up with smart renovations, and then pull your original investment back out to do it all again.

A Cyclical Strategy for Building Wealth

Think of the BRRRR method as a self-funding engine for growing your real estate portfolio. Traditional buy-and-hold investing is great, but it often means your down payment is locked up in a single property for years. BRRRR flips that script by focusing on creating new equity through renovations, not just waiting for the market to appreciate.

This "forced appreciation" is the secret sauce. It's what allows you to get your initial capital back and redeploy it.

It's like building a snowball. You start with a small chunk of cash to buy and fix up an undervalued property. Once it's renovated and has a paying tenant, you go to a lender and refinance based on its new, higher value—the After Repair Value (ARV), not what you paid. That cash-out refinance puts your original investment money right back in your pocket, freeing you up to find the next deal. The best part? You still own the first cash-flowing property.

The Five Stages of the BRRRR Method

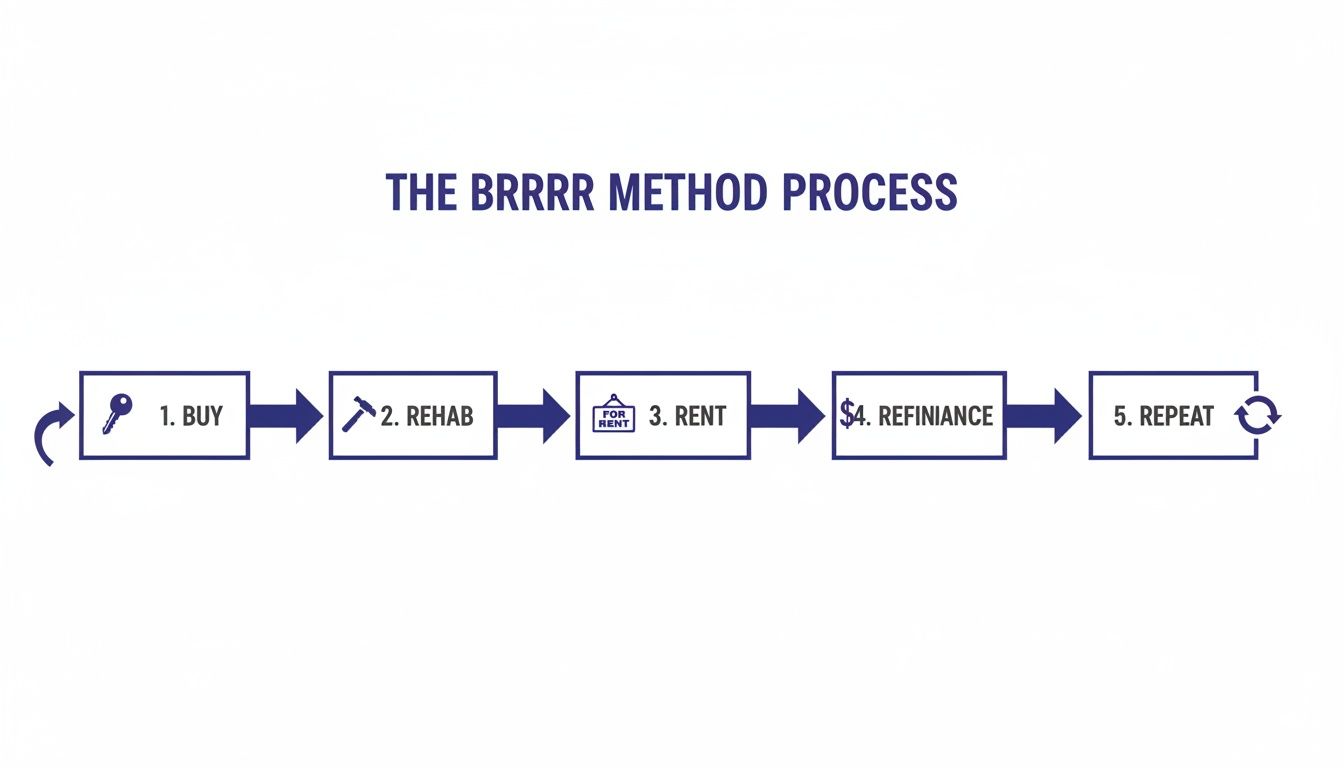

The process is broken down into five clear stages. Each one builds directly on the last, creating a repeatable cycle that can help you build wealth much faster than saving up for a new down payment every single time. Nailing each stage is key to making the whole thing work.

This visual shows you exactly how the steps flow together, creating a continuous loop.

As you can see, the whole process is designed to lead back to the beginning. That final "Repeat" step is where the magic really happens, and it's all powered by the capital you unlock during the refinance phase.

Here’s a quick breakdown of what happens at each stage of the process.

The 5 Stages Of The BRRRR Method

This table summarizes the core goal and primary task for each step in the BRRRR cycle.

| Stage | Objective | Key Activity |

|---|---|---|

| Buy | Acquire an undervalued property with potential for forced appreciation. | Purchase a distressed home well below its After Repair Value (ARV). |

| Rehab | Increase the property's market value through strategic renovations. | Execute a value-add renovation focused on high-ROI improvements. |

| Rent | Stabilize the asset with a tenant to generate consistent cash flow. | Market the property and secure a qualified, long-term tenant. |

| Refinance | Pull out the initial investment capital and the equity created. | Complete a cash-out refinance based on the property's new appraisal. |

| Repeat | Use the recovered funds to acquire the next investment property. | Reinvest the tax-free loan proceeds into another BRRRR deal. |

Understanding these individual components is the first step. The real skill comes in executing them smoothly so you can move from one deal to the next without losing momentum.

Buying The Right Distressed Property

The entire BRRRR method lives and dies by one simple truth: you make your money on the buy. This isn’t just about finding a property. It’s about finding the right one—an asset you can snag at a deep discount, with built-in equity from day one. Your profit margin is created the moment you sign the purchase agreement, long before the first hammer swings.

Think of this initial purchase as the foundation for the whole project. A great deal gives you the financial breathing room for unexpected repair costs and all but guarantees a successful refinance down the road. But a bad deal? It can tie up your cash and kill the BRRRR cycle before it even gets started.

The 70 Percent Rule Explained

So, how do you know if you're "buying right"? Experienced investors rely on a time-tested guideline called the 70% Rule. It’s a straightforward formula that helps you calculate your Maximum Allowable Offer (MAO) and avoid overpaying.

The 70% Rule says you should never pay more than 70% of a property's After Repair Value (ARV), minus the estimated cost of repairs.

Let's break that down with the formula: (ARV x 0.70) - Estimated Rehab Costs = Maximum Allowable Offer

Imagine you find a property with a potential ARV of $250,000, but it needs $40,000 in work. Here's how the math plays out:

- ($250,000 x 0.70) = $175,000

- $175,000 - $40,000 = $135,000

Your top offer should be $135,000. By sticking to this, you automatically build a 30% equity buffer into the deal. This cushion isn't just for profit; it’s there to cover holding costs (like taxes and insurance), closing fees, and any surprises that pop up during the renovation. Deviating from this rule is a gamble you don't want to take.

Finding Undervalued Properties

The best deals are rarely listed on the MLS, sitting pretty for everyone to see. You have to actively hunt for them. The most profitable BRRRR projects are typically found off-market, where you face less competition from retail buyers. Success comes down to your ability to find motivated sellers and see potential where others see problems.

Here are a few proven ways to source these hidden gems:

- Wholesaler Networks: These are your on-the-ground deal finders. Connect with local wholesalers who specialize in sourcing distressed properties. They do the hard work of finding motivated sellers, and you get access to the deal for a fee.

- Driving for Dollars: It sounds old-school, but it works. Get in your car and drive through neighborhoods you're targeting. Look for signs of neglect—overgrown yards, boarded-up windows, peeling paint. These are visual cues of a property that might have a very motivated seller.

- Direct Mail Campaigns: A targeted, personalized letter can cut through the noise. Send mailers to lists of absentee owners, landlords who are tired, or homeowners facing pre-foreclosure.

The BRRRR method is a powerful way to scale a portfolio precisely because it starts with buying at such a steep discount. Most pros agree that aiming for deals at 60-70% below ARV is non-negotiable. It creates that all-important safety net for market shifts and those inevitable renovation surprises.

Using Technology To Find Deals

Manually digging through listings and crunching numbers on dozens of potential properties is a surefire path to burnout. This is where technology gives savvy investors a massive edge. A platform like Property Scout 360 can transform the grueling task of finding deals into a focused, data-driven hunt.

Instead of guessing, you can apply investment-specific filters to scan entire markets for properties that fit your BRRRR criteria. Filter by purchase price, required rental income, or cash-on-cash return to instantly bring the best opportunities to the surface. To learn more about sourcing deals effectively, check out our complete guide on how to find an investment property. This approach lets you analyze more properties in less time, dramatically tipping the odds of finding a home run in your favor.

Executing A Value-Add Renovation

The rehab is where the magic really happens in the BRRRR method. This isn’t just about making a place look nice; it’s about manufacturing equity. While buying a property below market value gives you a head start, the renovation is how you actively force the property's value up. This creates the financial breathing room you need for the critical refinance step later on.

Your mindset here is crucial. You're not building your dream home or chasing the latest high-end trends you saw on a design show. Every single dollar you spend has to be a calculated investment aimed squarely at boosting the After Repair Value (ARV) and attracting a great tenant. Think like a property appraiser, not just a designer.

This means putting your money into smart, functional upgrades that deliver the biggest return. These will almost always win out over expensive, overly personal finishes.

Building Your Scope of Work

Before a single hammer swings, you need a rock-solid Scope of Work (SOW). This document is your renovation blueprint, detailing every task from demolition to the final coat of paint. A vague plan is a recipe for budget overruns and painful delays.

A good SOW is hyper-specific. Don't just write "update kitchen." Instead, spell it out: "Install 15 linear feet of white shaker cabinets, 'Luna Pearl' granite countertops, and a white subway tile backsplash." This level of detail is non-negotiable for getting accurate quotes from contractors and keeping the project on track.

For a deep dive into creating a comprehensive plan, our house flipping checklist provides a structured framework that works perfectly for BRRRR investors, too.

Prioritizing High-Impact Renovations

So, where should you spend your money? Focus on the things that both appraisers and tenants care about most. Your guiding principles should be durability, function, and broad-market appeal.

Here are the heavy hitters that consistently deliver the biggest bang for your buck:

- Kitchens and Bathrooms: These are the money rooms. Updated cabinets, durable countertops, new fixtures, and clean flooring here can dramatically increase your ARV.

- Curb Appeal: First impressions are everything. You can't put a price on how a property feels from the street. Fresh exterior paint, a tidy lawn, and a welcoming front door add massive perceived value for a relatively small cost.

- Flooring and Paint: Nothing makes a home feel fresh and new like a coat of neutral paint and clean, consistent flooring. Luxury Vinyl Plank (LVP) is an investor favorite for a reason—it's durable, waterproof, and looks great.

- The "Boring" Stuff: Don't get so caught up in cosmetics that you forget the core systems. A reliable HVAC, a solid roof, and safe electrical are essential for passing an appraisal and attracting quality, long-term tenants.

The most successful BRRRR investors renovate for two people: the appraiser and the future tenant. Your goal is to create a clean, safe, and modern home that commands top rent and meets strict lender standards.

Budgeting With Precision

Your renovation budget is a make-or-break part of the BRRRR strategy. If you underestimate your costs, you risk tying up all your capital in one deal, which completely short-circuits the "Repeat" part of the cycle.

A smart budget should account for materials, labor, permits, and a contingency fund of at least 10-15% for the inevitable surprises that pop up. Below is a sample budget to give you an idea of what a moderate renovation on a 1,500 sq. ft. home might look like.

Sample Rehab Budget For A BRRRR Project

This table gives a realistic cost breakdown for a typical rental-grade renovation on a 1,500 sq. ft. single-family home. Costs can vary significantly by location, but this provides a solid baseline.

| Renovation Area | Estimated Cost Range | Impact on ARV |

|---|---|---|

| Kitchen Remodel (Moderate) | $8,000 - $15,000 | High |

| Bathroom Remodel (Moderate) | $5,000 - $10,000 | High |

| Interior & Exterior Paint | $4,000 - $7,000 | High |

| Flooring (LVP/Carpet) | $4,500 - $8,000 | High |

| Fixtures (Lighting/Plumbing) | $1,500 - $3,000 | Medium |

| Landscaping & Curb Appeal | $1,000 - $2,500 | Medium |

| Contingency Fund (10-15%) | $3,000 - $6,500 | N/A |

Remember, these are estimates. Getting multiple quotes from trusted local contractors is the only way to lock in your actual numbers.

Modeling Your Renovation Scenarios

Guessing which upgrades will pay off is a rookie mistake. This is where you can use technology to get a serious leg up. A platform like Property Scout 360 lets you run the numbers on different renovation plans before you ever spend a dime.

You can input various rehab budgets to see how they affect your projected ARV and potential cash flow. This data-driven approach helps you answer critical questions, like whether a $15,000 kitchen remodel will actually add enough value to make your refinance numbers work. It turns what used to be a gut-feeling decision into a calculated strategy.

Securing Tenants And Generating Cash Flow

The rehab is done, the final coat of paint is dry, and the dust has settled. You now have a beautiful, renovated property. But right now, it's a non-performing asset, costing you money every day it sits empty. This is where the "Rent" stage comes in—it's time to turn this property into a cash-flowing machine.

The rehab is done, the final coat of paint is dry, and the dust has settled. You now have a beautiful, renovated property. But right now, it's a non-performing asset, costing you money every day it sits empty. This is where the "Rent" stage comes in—it's time to turn this property into a cash-flowing machine.

Getting a tenant in the door isn't just about starting the income stream. It’s about proving your entire investment strategy to the bank. A signed lease from a solid tenant is the proof they need to see that your property can support the new, larger mortgage you're about to ask for. Without it, the BRRRR method grinds to a halt.

Determining The Right Market Rent

Figuring out what to charge for rent is a tricky balancing act. If you aim too high, you’ll be stuck with a costly vacancy. Aim too low, and you're leaving money on the table every single month, which hurts your cash flow and makes your refinance numbers less attractive. This isn't the time for guesswork.

You need to find the sweet spot by running a comparative market analysis (CMA) specifically for rentals. This means digging into what similar properties—or comps—in the immediate area have recently rented for. Look for places with the same number of bedrooms and baths, and comparable square footage and finishes.

This is another place where having the right data gives you a huge leg up. Instead of spending hours scrolling through listings, a tool like Property Scout 360’s rent estimator uses real-time MLS data to give you a sharp, unbiased rent projection. It takes the guesswork out of the equation and makes sure your income projections are based on what's happening in the market right now.

Implementing A Rigorous Tenant Screening Process

A vacant property is a problem, but a bad tenant is a catastrophe. Evictions are a nightmare—they're expensive, they take forever, and they can easily wipe out an entire year's worth of profit. Your best defense is a rock-solid, consistent screening process.

Think of your process as a multi-step filter. You want to systematically identify responsible people who will pay on time and take care of your property. To stay compliant with fair housing laws, it's critical that every single applicant goes through the exact same evaluation.

A strong lease with a poorly screened tenant is nearly worthless. A thoroughly screened tenant is your best asset protection, even more so than the lease itself. Protecting your investment starts with choosing the right person to live in it.

Your screening checklist has to be non-negotiable. It protects you, finds you a great tenant, and creates a defensible, well-documented system.

Your Essential Tenant Screening Checklist

- Written Application: This collects all the basic info and, crucially, gives you written permission to run background checks.

- Credit Check: You're looking for a history of paying bills on time, a solid credit score (think 650+), and a manageable debt load.

- Criminal Background Check: This helps you screen for any relevant history that might pose a risk to the property or the neighborhood.

- Eviction History Check: This is a massive red flag. A past eviction is one of the strongest predictors of future problems.

- Income Verification: The gold standard is that an applicant's gross monthly income should be at least 3x the monthly rent. Always verify with recent pay stubs or an official offer letter.

- Landlord References: Call their last two landlords. Ask the important questions: Did they pay on time? How did they leave the property? Would you rent to them again?

Following these steps methodically is how you professionalize your operation. Securing a great tenant doesn't just start the cash flow; it stabilizes your asset and gives the lender the confidence they need to approve your cash-out refinance, which is the key to repeating the process all over again.

Pulling Your Capital Back Out With Refinancing

This is the moment of truth. After all the hard work—hunting down the deal, managing the messy renovation, and finding a great tenant—the cash-out refinance is where you get your money back to do it all over again. It’s the critical step that turns a one-off project into a repeatable, wealth-building machine.

The whole idea is beautifully simple. You're not asking for a loan based on the low price you paid. Instead, the bank appraises the property at its new, much higher After Repair Value (ARV)—the value you literally created with smart updates. That new, forced equity is what lets you pull your original cash right back out, often tax-free.

How The Cash-Out Refinance Works

Think of it this way: you bought an undervalued house, put your own cash and sweat into making it shine, and now you’re asking a bank for a long-term loan based on what it’s actually worth today. The bank is happy because they get a stable, income-producing asset as collateral. And you? You get your seed money back to go find the next diamond in the rough.

For most investors, the magic number is a loan for 75% of the new appraised value. This Loan-to-Value (LTV) is a pretty standard benchmark for investment properties. If you ran your numbers correctly from the start, that 75% loan should be more than enough to pay off any short-term financing (like a hard money loan) and, most importantly, put your initial cash investment right back in your pocket.

A Step-By-Step Numerical Example

Let's break down the math to see this in action. Say you found a deal with these numbers:

- Purchase Price: $150,000

- Rehab Budget: $40,000

- Total Initial Investment (Your Cash): $190,000

After you've completed your renovation, a licensed appraiser comes in and gives the home its new valuation.

- New Appraised Value (ARV): $260,000

Now, you head to a lender who agrees to a cash-out refinance at 75% LTV. Here’s how the money flows:

- Calculate the New Loan Amount: $260,000 (ARV) x 0.75 (LTV) = $195,000

- Pay Off Your Initial Investment: From that $195,000 loan, you repay yourself the $190,000 you originally put in.

- Capital Recovered: $195,000 - $190,000 = $5,000

In this perfect scenario, you not only got 100% of your cash back, but you actually walked away with an extra $5,000. Even better, you now own a turnkey rental property with $65,000 in equity ($260,000 ARV - $195,000 loan) and have all your original capital freed up for the final "Repeat" step.

Navigating Lender Requirements

Of course, lenders don't just hand over the cash automatically. They have specific boxes to check to make sure they're backing a solid, low-risk investment.

One of the biggest hurdles is the seasoning period. This is simply a waiting period the bank requires between when you bought the property and when they’ll let you refinance it. It usually lasts between six and twelve months. Lenders do this to make sure the new value you created is stable and not just a blip in the market. To get a better handle on all your options, you can learn more about how to finance rental property in our detailed guide.

A successful refinance is the ultimate validation of your BRRRR strategy. It proves you bought right, rehabbed smart, and stabilized the asset. Your job is to present the bank with a clean, profitable deal they are eager to finance.

This whole step is designed to get your cash out by using smart leverage. When done right, hitting that 75% LTV refinance lets you pull out most, if not all, of your initial investment. That’s what makes this system so scalable. For instance, one investor turned $55,000 into a fully renovated $180,000 property, allowing a cash-out refinance to pull every dollar back out for the next deal.

This is where a tool like Property Scout 360 becomes incredibly useful. It lets you model different financing scenarios on the fly. You can plug in various loan terms, interest rates, and LTVs to see exactly how it affects your ability to get your cash back and what your long-term cash flow will look like. It takes the guesswork out of the equation and helps you walk into a conversation with a loan officer already knowing your numbers cold.

Repeating The Process to Scale Your Portfolio

The last “R” in BRRRR is where the real magic happens. Repeat. This is what turns a one-off project into a scalable, wealth-building engine. Once the cash-out refinance puts your initial investment back in your pocket, you’re not stuck on the sidelines waiting to save up for another down payment. You’re ready to jump right back in and hunt for the next deal.

The last “R” in BRRRR is where the real magic happens. Repeat. This is what turns a one-off project into a scalable, wealth-building engine. Once the cash-out refinance puts your initial investment back in your pocket, you’re not stuck on the sidelines waiting to save up for another down payment. You’re ready to jump right back in and hunt for the next deal.

This is the core of the BRRRR strategy. Each cycle adds a cash-flowing property to your portfolio and returns the capital you need to do it all over again. It’s a powerful feedback loop that allows BRRRR investors to scale far more quickly than folks using traditional methods, where their cash is tied up for years in a single property.

Understanding Capital Velocity

The concept driving this growth is called capital velocity. Think of it as the speed at which you can put your money to work, get it back, and send it out to work for you again. The faster you can "turn" your capital, the more properties you can snap up in a shorter amount of time.

The magic of BRRRR is in the repeat. But repeating too fast or without a documented process is how portfolios crumble. The goal is to reinvest freed capital into new deals with a system that makes each cycle more efficient than the last.

Every time you complete the BRRRR cycle, you’re not just collecting another property. You’re strengthening your entire financial position and building a true wealth-generating machine.

The Long-Term Benefits of Scaling

As you start repeating the process, you begin to see the incredible compounding effects of real estate investing. It's not just about one property; it's about how multiple properties work together to build serious long-term wealth.

- Growing Cash Flow: Every new rental adds to your monthly passive income. This creates a bigger financial cushion and more cash to pour into future projects.

- Loan Paydown: Across your entire portfolio, you now have tenants paying down your mortgage debt every single month, building your equity on autopilot.

- Market Appreciation: While BRRRR is all about forcing appreciation, you also get the bonus of natural market appreciation over the long haul—but now it's happening across multiple properties at once.

The jump from one property to five, and then to ten, creates a powerful snowball effect. What started as a single investment quickly becomes a self-sustaining business.

Building The Systems To Scale Effectively

Here's the thing about scaling: it's not just about having the money. It's about having the systems to handle the increased workload. Going from one project a year to several at a time means shifting your mindset from being just an investor to being a business operator.

This means you need to get serious about creating repeatable processes for every single stage:

- Deal Sourcing: You can't just stumble upon deals anymore; you need a reliable pipeline.

- Contractor Management: You need a go-to team of contractors you can trust to get the job done right, on time, and on budget.

- Property Management: You must have a rock-solid system for finding great tenants, collecting rent, and handling maintenance issues without losing your mind.

Trying to manage all of this on a spreadsheet just won't cut it as you grow. This is where a tool like Property Scout 360 becomes a game-changer. Instead of analyzing deals one by one, you can manage a dashboard of potential properties, quickly comparing purchase prices, rehab estimates, and projected cash flow. It helps you vet more opportunities and make faster, data-driven decisions so your BRRRR engine never runs out of fuel.

Common Questions About The BRRRR Method

Even with a solid plan, jumping into a strategy like BRRRR is going to bring up some questions. It's a complex cycle, and getting the details right on financing, timelines, and risks is what separates a successful investment from a frustrating lesson.

Let's break down some of the most common hurdles and concerns I hear from investors.

How Much Money Do I Need To Start?

The whole point of BRRRR is to get your initial capital back out, but you definitely need money to get the first deal done. Your first pot of cash needs to cover the down payment for the purchase and the entire renovation budget.

How much? It really depends on your market, but you're probably looking at somewhere between $20,000 and $100,000. Most people starting out use a hard money or private loan to buy and fix the property. These lenders typically want you to bring 10-25% of the total project cost to the table in cash. Don't forget to budget for holding costs like insurance and taxes, too.

What Are The Biggest Risks?

The BRRRR method is incredibly effective, but it’s not foolproof. The success of the entire strategy comes down to your numbers. One bad calculation can sink the whole project and trap your cash, breaking the "Repeat" cycle.

I've seen three main things trip people up:

- Underestimating Rehab Costs: You pull back a wall and find unexpected foundation issues or ancient wiring. Suddenly, your carefully planned budget is out the window.

- Overestimating The ARV: Your analysis says the house should be worth a certain amount after repairs, but the market disagrees. This shrinks your equity and your potential cash-out.

- A Low Appraisal: This is the big one. It's the most common deal-killer for a reason. If the appraiser's number comes in below your target ARV, the bank won't lend you as much. This means you can't pull all of your original cash back out.

A low appraisal is the number one reason a BRRRR cycle fails. It traps your initial capital in the deal, making it impossible to "Repeat" the process and scale your portfolio.

How Long Does One Full Cycle Take?

This isn't a get-rich-quick flip. You have to be patient. A typical BRRRR cycle, from finding the property to having a renter and a new loan, usually takes between 6 to 12 months. This timeline gives each critical step the time it needs.

Here's a rough breakdown:

- Find & Buy: 1-2 months

- Renovate: 2-4 months

- Rent: 1 month

- Refinance: 2-5 months, which includes the bank's required "seasoning period."

That seasoning period is a big factor. It's a mandatory waiting time most lenders enforce before they'll refinance a property based on its new, higher value. Any delays along the way can easily push your timeline out even further.

Stop guessing and start analyzing. With Property Scout 360, you can find and evaluate profitable deals in minutes, turning complex BRRRR calculations into simple, data-driven decisions. Explore your next investment with Property Scout 360 today.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.