How to Invest in Rental Property A Data-Driven Guide

Learn how to invest in rental property with our data-driven guide. We cover market analysis, deal evaluation, and financing to build your real estate portfolio.

Investing in rental property isn't about luck; it's about following a proven framework. You start by defining your financial goals, then find a market that makes sense, learn to analyze deals, line up your financing, and manage the asset well. The journey doesn't begin on real estate websites—it starts with a solid strategy built to match your long-term vision for building wealth.

Laying the Groundwork for Your First Rental Property

Before you even think about scrolling through listings, the single most important thing you can do is define what a "win" looks like for you. Jumping into real estate without a clear "why" is like setting off on a road trip without a destination. You'll definitely end up somewhere, but probably not where you intended.

This is the stage where you turn vague ambitions into a concrete financial plan. What's the main driver here? Every investor has a different primary motive.

- Consistent Monthly Cash Flow: Are you hoping to generate an extra income stream to cover bills or maybe even quit your day job sooner?

- Long-Term Equity and Appreciation: Is the goal to build a massive nest egg for retirement by letting an asset grow in value over 20 or 30 years?

- Portfolio Diversification: Maybe you're just looking to balance out your stock portfolio with a physical asset that kicks off its own returns.

Define Your Investment Criteria

Your personal finances will heavily influence your strategy. Get real with yourself about your risk tolerance. Would you be comfortable with a major fixer-upper that needs a ton of cash and work upfront but offers a huge potential payoff? Or does a turnkey property with smaller, more predictable returns sound better?

You also need a realistic timeline. Are you in this for five years or thirty? That answer alone will dramatically change the kind of property and market you should be looking at.

A well-defined strategy is your filter. It gives you the power to say "no" to the dozens of shiny objects and "good deals" that don't actually fit your plan, saving you a ton of time and stress.

This is where a tool like Property Scout 360 becomes invaluable right from the start. Instead of just guessing, you can anchor your goals to actual numbers and make sure your financial blueprint is built on solid ground.

The market is showing some real opportunities for investors who come prepared. The global real estate outlook from Aberdeen points to strengthening rental growth and more reasonable prices on the horizon for 2025. With the number of U.S. single-family rental households growing by 1.7% and multifamily rents still up over 20% from pre-pandemic levels, the demand is clearly there. Getting your plan straight now means you'll be ready to pounce when the right deal comes along.

How to Pinpoint Profitale Rental Markets

We’ve all heard it a thousand times: "location, location, location." While that's true, it’s only half the story for a rental investor. A great location isn't just about curb appeal; it's about the economic engines humming beneath the surface that create real, lasting rental demand. To succeed, you have to stop thinking like a homebuyer and start thinking like a market analyst.

This means you’ve got to get past the pretty pictures and dive into the data. The goal is to find those sweet spots where the number of people looking for a place to rent is set to outpace the available supply for years to come. A data-first approach lets you find these gems before everyone else does.

The Economic Clues of a Strong Market

Before you even look at a single property, you need to zoom out and look at the big picture. Start your search by focusing on cities and regions with healthy, diverse economies. A town that lives and dies by a single factory is a house of cards. A city with booming healthcare, tech, and university sectors? Now you're talking.

Here are the vital signs I always check first:

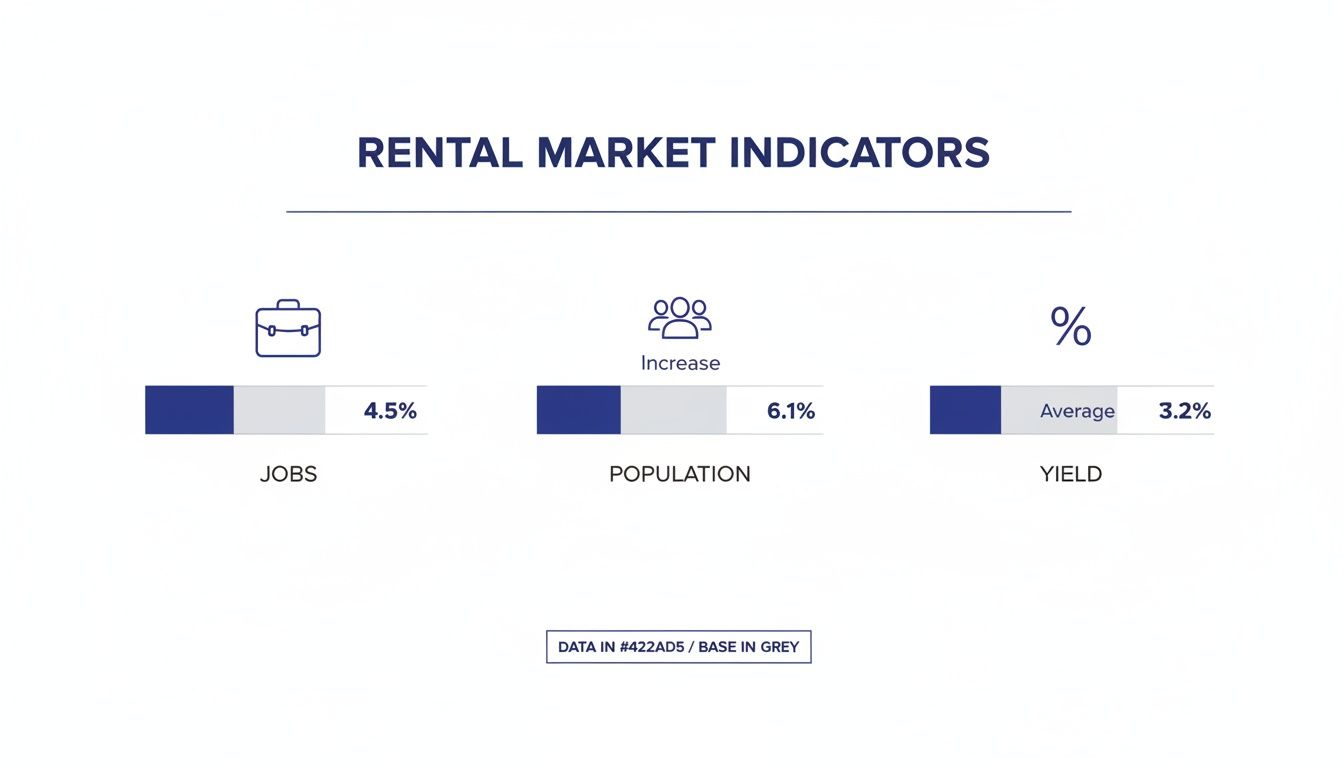

- Job Growth: Are companies setting up shop or expanding? A steady stream of new jobs means a steady stream of new tenants. I look for markets with year-over-year job growth that’s beating the national average.

- Population Trends: Are more people moving in than moving out? Positive net migration is one of the most powerful indicators of a healthy rental market. Simple as that.

- Local Development: Keep your ear to the ground for news about big infrastructure projects, new hospitals, university expansions, or major corporate relocations. These are magnets for people who will need a place to live.

This is where you can use a tool like Property Scout 360 to filter entire regions based on the metrics that matter most to you, like rental yield and price-to-rent ratio.

By layering these data points, you can quickly screen out stagnant markets and focus your energy on areas where the economic fundamentals actually support a strong rental business.

Key Market Analysis Metrics

To make this even clearer, here’s a breakdown of the key data points I always analyze when vetting a potential market. It’s not just about finding a good number; it’s about understanding the story that number tells you.

| Metric | What to Look For | Why It Matters | How Property Scout 360 Helps |

|---|---|---|---|

| Population Growth | Consistent, positive growth | A growing population fuels housing demand. | Provides historical and projected population data. |

| Job Growth | Above national average | More jobs mean more potential tenants with stable income. | Tracks employment trends and key industries. |

| Median Home Price | Affordable relative to your budget | Determines your entry cost and potential financing. | Shows real-time property values by neighborhood. |

| Price-to-Rent Ratio | Lower is often better (e.g., < 15) | Indicates if it's more favorable to rent than buy. | Calculates this ratio automatically for any area. |

| Rental Vacancy Rate | Low and decreasing | A low vacancy rate signals strong rental demand. | Displays current and historical vacancy trends. |

| Property Taxes | Lower is better | Directly impacts your monthly holding costs. | Integrates local tax data into cash flow analysis. |

Looking at these metrics together gives you a holistic view, helping you avoid markets that look good on the surface but have hidden flaws.

Don't Forget the Local Details

Once you have a promising city on your radar, it's time to zoom in. The nitty-gritty local details can make or break your investment. These are the things that can turn a good deal into a great one—or a profitable-looking property into a money pit.

Take property taxes. They can swing wildly from one county to the next. A 2% property tax rate versus a 0.5% rate on the exact same house can mean thousands of dollars a year out of your pocket, completely torpedoing your cash flow.

Just as critical are the local landlord-tenant laws. Some areas are famously "tenant-friendly," with complicated eviction processes and strict rent control. Others are more "landlord-friendly," which makes managing your property much more straightforward. You absolutely have to know the rules of the game before you buy in.

A market might have incredible appreciation potential, but if local laws make it a nightmare to evict a non-paying tenant, that potential might not be worth the headache. Always balance the numbers with the on-the-ground operational reality.

Comparing Neighborhoods with Precision

Even within the same city, one neighborhood can be a world away from another. This is where having a powerful analysis tool gives you a serious edge. You need to compare specific submarkets to find that perfect blend of affordability, demand, and growth.

Imagine two neighborhoods in the same metro:

- Neighborhood A: It's the trendy, hot spot. Property values are high, and the price-to-rent ratio is tight. You might see great appreciation down the road, but your monthly cash flow could be thin or even negative.

- Neighborhood B: This is a solid, working-class area. Home prices are lower, but rental demand is steady and strong. The price-to-rent ratio is much healthier, meaning you'll likely see positive cash flow from day one, even if appreciation is a bit slower.

There's no single "right" answer here—it all comes back to your personal investment strategy. By running side-by-side comparisons of key numbers like rental yield and cash-on-cash return, you can make a decision backed by hard data, not just a hunch. If you want to go deeper on this, our guide to the best markets for rental properties breaks this down even further.

Running the Numbers on Any Potential Deal

You’ve found a promising market and maybe even a few properties that have caught your eye. This is the moment of truth. It's where seasoned investors separate themselves from the dreamers. The whole game comes down to one critical skill: analyzing a deal quickly, accurately, and without letting your emotions get in the way.

Forget about complex spreadsheets for now. When you're first looking at a property, you need a way to figure out if it's a winner or a dud in minutes, not hours. By mastering a few key financial metrics, you’ll gain the confidence to pull the trigger on good deals and, more importantly, walk away from the bad ones.

This skill is the engine of your entire investment strategy. It turns raw market data into a clear "yes" or "no."

The Three Pillars of Deal Analysis

Before you get lost in the weeds of complex formulas, let's simplify. When you're sizing up a potential rental, the entire financial picture boils down to three core concepts. Grasping how these work together is absolutely fundamental to your success.

Cash Flow: This is the big one, the metric that pays the bills. It’s the money left in your pocket each month after you’ve collected rent and paid all the expenses—mortgage, taxes, insurance, maintenance, everything. Positive cash flow is your paycheck.

Capitalization (Cap) Rate: Think of this as a way to compare apples to apples. The cap rate helps you gauge the profitability of different properties, regardless of their price or your financing. It measures the property's annual return as if you paid all cash.

Cash-on-Cash (CoC) Return: This one is all about your money. It tells you exactly how hard your down payment and closing costs are working for you. It's the most personal of the metrics because it's based on the actual cash you pulled out of your pocket.

These aren't just numbers on a page; they're the vital signs of your investment. The infographic below highlights some of the market forces, like job growth and population trends, that directly impact these numbers and drive your returns.

The takeaway here is simple: a healthy local economy with more jobs and more people moving in almost always leads to stronger rental demand and better investment outcomes.

A Practical Example: Single-Family Home vs. Duplex

Let's make this real. Imagine you're using a tool like Property Scout 360 to compare two very different opportunities.

Scenario 1: The Single-Family Home (Growth Market)

- Purchase Price: $300,000

- Monthly Rent: $2,200

- Your Down Payment (20%): $60,000

Scenario 2: The Duplex (Cash-Flow Market)

- Purchase Price: $350,000

- Total Monthly Rent (2 units): $2,800

- Your Down Payment (25%): $87,500

Just looking at the raw numbers, it's tough to know which is the better investment. The single-family home might appreciate faster, but the duplex brings in more rent from day one. This is where analysis makes the decision for you. The numbers will clearly show which property aligns with the goals you set earlier.

The numbers don't have opinions. They simply tell you which property aligns better with your specific financial goals—whether that’s immediate income or long-term wealth creation.

This is where you can move beyond napkin math. For a deeper dive into the calculations, our guide on using a rental property analyzer spreadsheet offers free templates and more context.

Using Technology to Analyze Deals in Minutes

Let's be honest, manually calculating taxes, insurance, vacancy rates, and maintenance costs for every property you look at is a surefire way to burn out. This is where modern tools give you a massive edge.

Platforms like Property Scout 360 do all the heavy lifting for you. You just plug in the property address, and the software pulls in MLS data, tax records, and local rent estimates to generate a full financial breakdown almost instantly. You can immediately see the property’s health—from cash flow and cap rate to long-term return projections.

This speed is crucial. It lets you sift through dozens of listings, discard the duds in seconds, and focus your energy only on the deals that actually have potential. Instead of getting stuck in "analysis paralysis," you can move from analysis to action with total confidence.

Securing Your Financing and Structuring the Deal

You’ve found a property that looks like a winner and the initial numbers are promising. Great. Now comes the moment of truth: securing the financing that turns this "deal on paper" into an actual income-producing asset.

Getting the right loan isn't just a box to check. It's a strategic decision that will shape your monthly cash flow and overall returns for years to come. The world of investment property loans is a completely different ballgame than buying your own home—lenders see it as a business transaction, which means the rules are stricter and the stakes are higher.

What Are Your Loan Options?

When you first start looking for an investment loan, you’ll realize quickly that you have a few different paths you can take. The best one for you hinges on your personal finances, your long-term strategy, and whether you plan on living in the property.

Common Financing Avenues

Conventional Investment Loans: This is the workhorse loan for most investors buying a property they don't plan to live in. Be prepared for a higher down payment, typically in the 20-25% range. Your interest rate will also be a bit higher than on a primary residence mortgage, and lenders will scrutinize your credit score and debt-to-income (DTI) ratio.

Government-Backed Loans (for House Hacking): Here’s where new investors can get a serious leg up. If you plan to live in one unit of a duplex, triplex, or fourplex, you open the door to some incredible low-down-payment options. FHA loans let you get in for as little as 3.5% down, and if you're an eligible veteran, a VA loan could mean 0% down. This "house hacking" strategy is arguably one of the most powerful ways to start building a portfolio.

Portfolio Loans: Already have a few properties under your belt? Some banks, often smaller local or regional ones, offer portfolio loans. Instead of focusing solely on your personal W-2 income, they'll assess the performance of your entire real estate portfolio. This can be a fantastic, flexible option once you start to scale.

The financing rabbit hole goes deep, with plenty of nuances for each option. For a more detailed breakdown, check out our complete guide on how to finance your rental property.

Why Lenders Obsess Over Your DTI Ratio

Your debt-to-income (DTI) ratio is the magic number lenders use to gauge whether you can truly afford another mortgage. They calculate it by dividing all your monthly debt payments (credit cards, car loans, student loans) by your gross monthly income.

For an investment property, most lenders draw a hard line at a DTI of 43% or less.

They’re so strict because they need to feel confident you can cover all your personal bills plus the new mortgage, even if your new rental sits vacant for a month or two. A high DTI is an immediate red flag. My advice? Get a handle on your consumer debt before you even start applying for investment loans.

Think of your DTI as a financial stress test. A low ratio signals to the bank that you have enough breathing room in your budget to absorb the unexpected punches that come with being a landlord.

How Structure and Scenarios Affect Your Bottom Line

This is where the real strategy comes into play. How you structure the purchase—specifically your down payment and loan term—can radically alter your financial picture. A small tweak here can mean thousands of dollars in cash flow over time.

Let's revisit that $300,000 single-family home we looked at earlier, assuming a 7% interest rate. This is where a tool like Property Scout 360 becomes indispensable, letting you model different scenarios in seconds.

Here's a quick comparison of the most common loan types to help you see the differences at a glance.

Financing Options Comparison

| Loan Type | Typical Down Payment | Best For | Pros | Cons |

|---|---|---|---|---|

| Conventional | 20-25% | Most non-owner-occupied properties; experienced investors. | Widely available; can be used for any type of property. | Higher down payment; stricter credit/DTI requirements. |

| FHA Loan | 3.5% | House hackers living in a 2-4 unit property. | Very low down payment; more lenient credit score rules. | Must be your primary residence; mortgage insurance required. |

| VA Loan | 0% | Eligible veterans and service members house hacking. | No down payment required; no private mortgage insurance. | Must be an eligible veteran; primary residence only. |

| Portfolio Loan | Varies (often 25%+) | Investors with multiple properties looking to scale. | Flexible underwriting based on portfolio, not just personal income. | Not offered by all banks; can have higher interest rates. |

Choosing the right loan is about aligning the terms with your specific goals for the property.

Real-World Scenarios: Cash Flow vs. Equity

Now, let's see how changing the structure impacts our numbers for that $300,000 house:

| Financing Scenario | Down Payment | Monthly P&I | Initial Cash-on-Cash Return |

|---|---|---|---|

| 20% Down / 30-Year Loan | $60,000 | $1,596 | 9.8% |

| 25% Down / 30-Year Loan | $75,000 | $1,496 | 9.1% |

| 20% Down / 15-Year Loan | $60,000 | $2,157 | 2.5% |

Look closely at what's happening. Putting 25% down instead of 20% drops your monthly payment by $100, which is great for cash flow. But since you had to bring more cash to the table, your cash-on-cash return actually dips a bit.

The 15-year loan is even more telling. Your monthly payment jumps dramatically, which absolutely crushes your immediate cash flow. On the flip side, you're building equity like crazy and will own the property free and clear in half the time, saving a fortune in interest.

There's no single "right" answer here. The best choice depends entirely on your strategy: are you optimizing for maximum monthly income right now, or are you focused on building long-term wealth as quickly as possible?

From Closing Day to Cashing Your First Rent Check

You’ve crunched the numbers, gotten your financing in order, and now the finish line is just ahead. This is the moment a deal stops being a spreadsheet and becomes a real, physical asset. The stretch between getting a property under contract and depositing that first rent check is a make-or-break sprint that will set the stage for your entire investment journey.

Getting this part right is what separates the pros from the panicked first-timers. It all boils down to a repeatable process for your final checks and a clear game plan for your first year. Think of this as your playbook for a smooth handover from buyer to landlord, so you can start generating income without unnecessary delays.

Your Final Due Diligence Checklist

Once your offer is accepted, the clock starts ticking. Your inspection and appraisal contingencies aren't just formalities; they're your last chance to find any deal-breakers. This is where you can negotiate repairs, get a price reduction, or walk away without losing your earnest money.

When it comes to the home inspection, you need to think beyond the basics. Sure, the inspector will cover the major systems, but you need to view the property with two sets of eyes: as a future tenant and as a business owner.

- Hunt for the big-ticket problems: Zero in on the roof's age, the HVAC system's condition, any hint of foundation issues, and old electrical panels. These are the $5,000+ surprises that can devour your first year's profits in one go.

- Think about durability: Take a hard look at the flooring, paint, and fixtures. Can they handle the wear and tear of tenants, or are you going to be replacing them every time someone moves out?

- Scrutinize the appraisal: When the appraisal report lands, first confirm it supports your purchase price. But don't stop there. Dig into the comparable properties—the "comps"—the appraiser used. Are they genuinely similar in size, condition, and location to your property?

An appraisal that comes in low isn't just a headache for your loan. It's a flashing red light from the market telling you that you might be overpaying. Use that report as a powerful piece of leverage in your negotiations.

Nailing Down a Competitive—and Profitable—Rent

The ink is dry on the closing documents. Now what? Your very first job is to set the rent, and it's a delicate balance. Price it too high, and you're stuck with a costly vacancy. Go too low, and you're leaving cash on the table every single month.

To get this right, you need solid, real-time data. This is where a tool like Property Scout 360 becomes a huge asset, giving you up-to-the-minute rent estimates for similar properties right in your neighborhood. Pull at least three to five active, comparable listings and be brutally honest about how your property's amenities, condition, and location stack up.

And a quick heads-up: be transparent about the total cost for the tenant. The FTC has started cracking down on landlords who tack on hidden mandatory fees. If you charge for trash service, parking, or anything else, disclose it upfront. It builds trust and keeps you out of legal trouble.

The Big Management Decision: DIY or Hire a Pro?

Your last major decision is how you're going to manage this property day-to-day. There’s no universal right answer here; it really comes down to how close you live, how much free time you have, and frankly, your personality.

| Management Style | Best For | Pros | Cons |

|---|---|---|---|

| Self-Management | Local investors with flexible schedules and a hands-on approach. | You save 8-10% on management fees and have direct control. | It's a major time commitment. You're the one on call 24/7 for emergencies. |

| Property Manager | Out-of-state investors or anyone prioritizing passive income. | Truly hands-off operations, professional tenant screening, and legal compliance. | Costs 8-10% of the gross monthly rent, which eats into your cash flow. |

If you decide to hire a property manager, do your homework. Ask for references from other owners, make sure they're properly licensed, and read their fee structure with a magnifying glass. A great property manager is a true partner who can make you successful. A bad one can turn a dream investment into a total nightmare. Making this choice thoughtfully is a critical step as you learn how to invest in rental property.

Scaling Your Portfolio and Dodging Common Pitfalls

Getting the keys to your first rental is a huge milestone, but it's really just the starting line. The long-term game is about building a portfolio that generates wealth, and that means shifting your mindset from a hands-on landlord to a strategic portfolio manager. It’s all about creating systems so you're ready to grow.

One of the most powerful ways to expand is by putting your equity to work. As you pay down the mortgage and your property's value climbs, you unlock a fresh source of capital. You can tap this equity with a cash-out refinance or a Home Equity Line of Credit (HELOC) to get the down payment for your next property. This is the core of the popular BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), and it's how seasoned investors acquire multiple properties without starting from zero on each down payment.

Sidestepping Costly Investor Mistakes

As you scale, the challenges change. I've seen more investors get knocked out of the game by poor operations than by bad properties. Nailing the fundamentals is what separates the pros from the amateurs.

Here are three of the most common—and expensive—mistakes to watch out for:

Miscalculating Maintenance Costs: You'll often hear the "budget 1% of the property's value per year" rule, but honestly, that can leave you dangerously short. A much safer bet is to earmark 5-10% of your monthly gross rent for both routine repairs and big-ticket capital expenditures, like a new roof or furnace.

Sloppy Tenant Screening: One bad tenant can wipe out a year's worth of profit. A simple credit check isn't enough. You need to verify their income (I always look for at least 3x the rent), personally call their previous landlords, and run a full background check. Think of it as your first line of defense.

Not Having Enough Cash on Hand: Unexpected expenses are not a matter of if, but when. You absolutely need a separate cash reserve for each property. A good target is 3-6 months' worth of total operating expenses (PITI, utilities, etc.). This safety net is what keeps a surprise plumbing issue from derailing your entire investment.

Your real estate portfolio is a business, not a hobby. You have to systemize rent collection, maintenance, and bookkeeping if you want to scale. If you don't, you're not building an asset; you're just creating a high-stress, low-paying job for yourself.

Systemize Everything to Fuel Your Growth

You can't do it all yourself, especially once you have a few doors. The trick is to build your systems before you need them. Start using property management software to automate rent reminders and track every dollar. Create a standard turnover checklist you use every time a tenant moves out.

Finally, a quick but important legal note: always be transparent with your pricing. The Federal Trade Commission (FTC) is cracking down on landlords who advertise a low rent and then tack on hidden mandatory fees. Be upfront about every cost to stay out of legal hot water and build a reputation your tenants can trust.

By steering clear of these common blunders and building solid systems from day one, you’ll be in a powerful position to grow your portfolio and achieve your financial goals.

Your Top Rental Property Questions, Answered

Even with the best roadmap, you're going to have questions. That's a good thing—it means you're thinking critically. Let's tackle some of the most common ones that come up for new investors so you can move forward with confidence.

How Much Money Do I Really Need to Get Started?

This is the big one, and the honest answer is: it depends on your market and your strategy. For a standard investment loan, plan on putting down 20-25%. You’ll also want to set aside another 3-5% of the purchase price for closing costs.

But the most important part? Have a cash reserve. I recommend keeping three to six months' worth of PITI (principal, interest, taxes, insurance) in the bank. This buffer is your safety net for surprise repairs or a month of vacancy.

Don't let those numbers scare you, though. There are creative ways to get in the game with less. If you're willing to "house hack"—living in one unit of a duplex, triplex, or fourplex—you can often secure an FHA loan with as little as 3.5% down.

What’s a Good Cash-on-Cash Return?

This is a classic question, and the answer isn't one-size-fits-all. A solid benchmark for a good cash-on-cash (CoC) return is often in the 8-12% range. However, this number can swing wildly depending on the market.

In a high-growth area like Austin or Boise, you might see investors perfectly happy with a 5-7% CoC return. They're playing the long game, betting on appreciation to build their wealth.

In markets prized for pure cash flow, like many in the Midwest, seasoned investors won't even look at a deal unless it's projecting 12% or more. This is where a tool like Property Scout 360 becomes indispensable—it runs the CoC calculation instantly, letting you filter opportunities based on the returns you're chasing.

Can I Actually Invest in Properties Out of State?

You bet. Investing from a distance is more common than ever, but it’s a team sport. You absolutely need a rock-solid crew on the ground: a savvy real estate agent who understands investors, a meticulous home inspector, and, most importantly, a fantastic property manager.

Since you can't just drive by to check on things, your success hinges on data. This is where analysis platforms shine. They give you the power to vet markets, zoom in on promising neighborhoods, and run the numbers on specific deals from thousands of miles away, giving you the confidence to pull the trigger.

Ready to stop guessing and start analyzing deals with precision? Property Scout 360 gives you the instant calculations and market data you need to find profitable rentals and build your portfolio. Sign up for free and analyze your first deal today!

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.