How to Finance an Investment Property: A Practical Guide to Funding

Learn how to finance an investment property with practical loan options, creative strategies, and expert tips to fund deals and grow your portfolio.

Financing an investment property isn't like getting a mortgage for your own home. Lenders play by a different set of rules because, in their eyes, it’s a business deal, not a place to live. That means they're a lot stricter. You'll generally need a higher credit score (think 700+), a bigger down payment (usually 20-25%), and a lower debt-to-income ratio to even get in the door. Getting a handle on these numbers before you even talk to a lender is the single most important thing you can do.

Building Your Financial Foundation

Before you get lost in property listings and mortgage calculators, you need to get your own financial house in order. When a lender reviews your application for an investment loan, they're really just trying to answer one question: "How risky is this?" Your job is to look like the safest bet they've seen all day.

This goes way beyond just having a good credit score. They see your primary home payment as something you’ll always make. But an investment property? That's a business venture, and businesses can fail. To get comfortable, they're going to put your finances under a microscope.

Key Metrics Lenders Scrutinize

To get ready, start looking at your finances the way an underwriter will. This isn't just about getting approved; it's about locking in the best possible terms. A lower interest rate and better terms directly translate to higher cash flow and a better return on your investment down the road.

Here are the big three metrics you need to dial in:

- Debt-to-Income (DTI) Ratio: This is simply your total monthly debt payments divided by your gross monthly income. For investment properties, most lenders draw the line at 43%. A lower DTI shows them you can easily manage another mortgage payment, even if the property sits vacant for a month or two.

- Credit Score: You might be able to get a regular mortgage with a score in the 600s, but for an investment property, you really want to be aiming for 740 or higher. A killer score doesn't just help you get approved; it unlocks the best interest rates, which can save you a ton of money over the life of the loan.

- Cash Reserves: Lenders want to see you have a safety net. After closing, they'll want to verify you have enough cash to cover six to twelve months of PITI (principal, interest, taxes, and insurance) for every property you own—including the one you're buying.

Pro Tip: Lenders call this "liquid reserves" for a reason. The money needs to be accessible, so funds in your 401(k) or IRA won't count. It has to be in a checking, savings, or money market account.

Aligning Your Goals with Your Finances

The kind of investing you plan to do will also influence the kind of financing you can get. A lender looks at an application for a stable, long-term rental very differently than one for a quick fix-and-flip project. You need to know your strategy before you apply.

Are you trying to create steady monthly income from a turnkey rental? Or are you hunting for a deal you can force appreciation on with a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy? The loan you need, and the financial story you tell, will be completely different for each. An investor looking for long-term cash flow needs to show stable income, while a flipper might need to show a track record of successful projects. Getting clear on this first will point you toward the right loan from the start.

Figuring Out Your Financing Options

Once your financial house is in order, it's time to dive into the actual loan products. Getting a handle on the different types of mortgage loans is key, because what’s available for an investment property is a whole different ballgame than your standard home loan. Each one is built for a specific kind of investor and a particular strategy.

Picking the right financing isn't just about getting a "yes" from the bank. It's about structuring a deal that starts making you money from day one. Let's walk through the most common paths you'll encounter.

The Go-To Choice: Conventional Investment Loans

For most investors, especially when starting out, a conventional loan is the default option. These are the traditional mortgages from banks and credit unions that aren't backed by the government. Because the lender is taking on all the risk, they're a lot stricter than they would be for your own home.

You'll almost always need a down payment of at least 20%, and frankly, 25% is becoming the new normal as lenders get more cautious. The upside of that larger down payment is you get to skip Private Mortgage Insurance (PMI), which is a huge win for your monthly cash flow. Lenders will also want to see a solid credit score, typically 700 or higher, and those cash reserves we talked about earlier—usually six to twelve months' worth of payments.

The market for these loans is definitely humming. Global real estate transaction volumes hit a staggering $739 billion over the 12 months leading up to Q2 2025, which is a 19% jump from the previous year. This points to a healthy financing environment where good deals are getting funded.

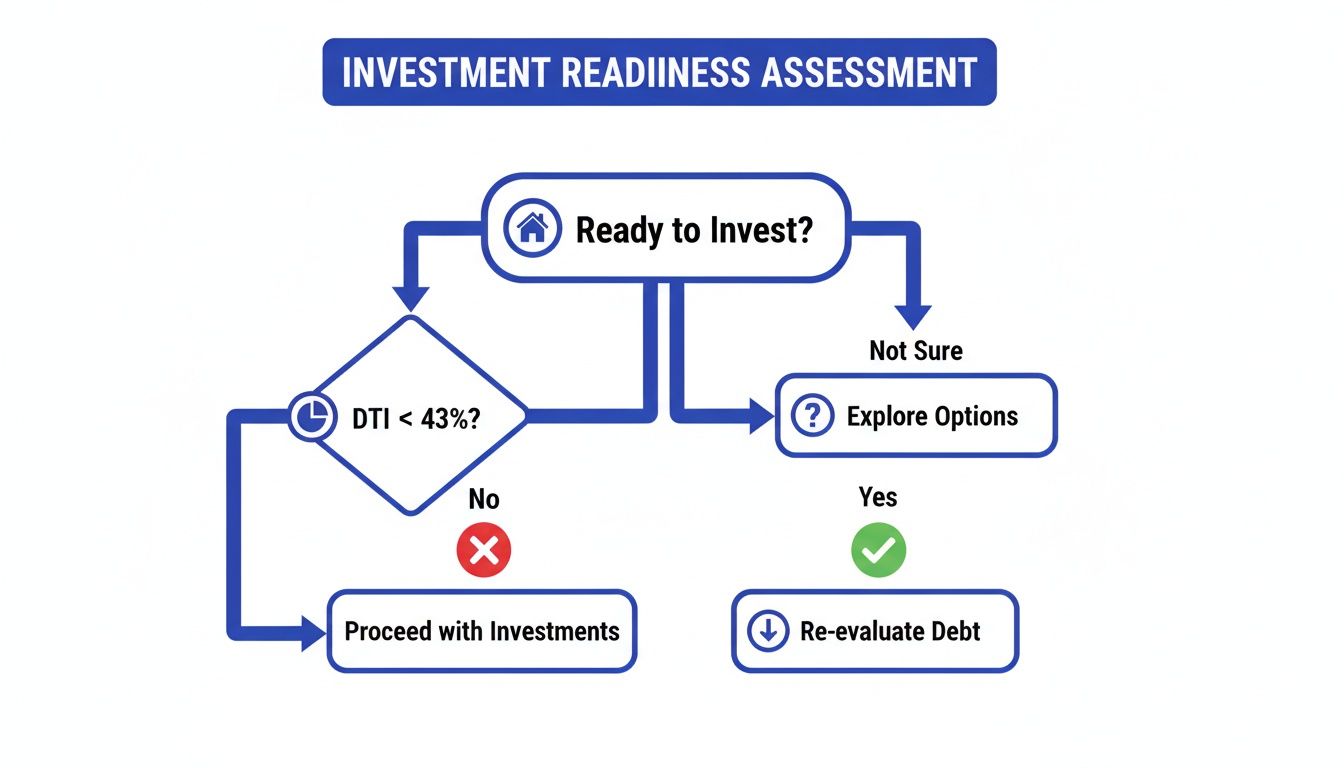

This quick flowchart can help you see if you’re on the right track for a conventional loan.

As the chart shows, a lender's first big checkpoint is your debt-to-income ratio. If you've got that under control, you're already in a much stronger position to get approved.

Getting Creative With Government-Backed Loans (And House Hacking)

While most government loans like FHA and VA are meant for primary homes, they open up a fantastic opportunity for new investors through a strategy called "house hacking."

The idea is simple: you buy a small multi-family property—like a duplex or fourplex—live in one of the units, and rent out the others.

Because you're living there, you can qualify for the amazing terms of these owner-occupant loans:

- FHA Loans: Let you buy a property with up to four units with as little as 3.5% down. The best part? You can use the projected rent from the other units to help you qualify.

- VA Loans: This is a game-changer for veterans and active service members. You can purchase a multi-family property with 0% down and no PMI. It’s one of the best deals in real estate, period.

The only real string attached is that you have to live in one of the units for at least a year. After that, you're free to move out and rent your former unit, turning the entire building into a cash-flowing machine. It's probably the single best way to start building a portfolio with very little money out of pocket.

Scaling Your Portfolio With Portfolio Loans

After you've acquired a few properties, juggling a bunch of separate mortgages starts to feel like a full-time job. That's where portfolio loans come in. With these, the lender isn't just looking at you; they're underwriting the health of your entire real estate business.

These loans are kept "in-house" by the lender, meaning they don't sell them off to big secondary market players like Fannie Mae. This gives them a ton of flexibility. They might approve you based on the income your properties generate, not just your personal DTI.

Portfolio loans are perfect for when you want to:

- Consolidate: Roll several mortgages into a single loan with one easy payment.

- Tap Into Equity: Pull cash out of multiple properties at once to fund your next deal.

- Finance Unconventional Properties: Get funding for a property that a conventional lender wouldn't touch.

These lenders often lean heavily on a metric called the Debt Service Coverage Ratio (DSCR), which is all about whether the property's income can cover its mortgage payments. If you're nearing this stage, you should definitely learn more about how DSCR loans work.

Comparing Common Investment Property Loans

To make sense of it all, here’s a quick side-by-side look at how these loan types stack up.

| Loan Type | Typical Down Payment | Credit Score Requirement | Best For |

|---|---|---|---|

| Conventional | 20%–25% | 700+ | First-time investors with strong credit and savings. |

| FHA (House Hack) | 3.5% | 620+ | New investors buying a 2-4 unit property to live in. |

| VA (House Hack) | 0% | 620+ | Eligible veterans buying a 2-4 unit property to live in. |

| Portfolio | Varies (often 25%+) | Varies (property-focused) | Experienced investors scaling from 4+ properties. |

Choosing the right loan is a strategic decision that depends on where you are in your investing journey—from your very first duplex to managing a growing portfolio.

Running the Numbers on a Potential Deal

This is where the rubber meets the road. If you’re not willing to do the math, you’re just gambling. Once you have your personal finances sorted out and have an idea of what kind of loan you’re going for, it's time to analyze an actual property. Honestly, learning to run the numbers is the one skill that separates investors who build wealth from those who buy themselves a very expensive headache.

Your financing isn’t just a loan; it’s the engine of your entire investment. The interest rate, loan term, and down payment you lock in will dictate your profitability every single month. Let's dig into how the mortgage connects directly to a property's real-world performance.

The Core Metrics Every Investor Lives By

Before you can confidently say "yes" to a deal, you need to get intimate with a few key numbers. These calculations tell the true story of a property, stripping away the nice photos and sales pitches.

- Monthly Cash Flow: This is the big one. It's the cash left over after you've collected all the rent and paid every single bill associated with the property. Positive cash flow means the property is putting money in your pocket. Negative means it's taking money out. Simple as that.

- Cash-on-Cash (CoC) Return: This metric answers the question, "How hard is my initial investment working for me?" It measures your annual pre-tax cash flow against the total cash you put into the deal. A lot of seasoned investors won’t touch a deal with a CoC return under 8-12%.

- Capitalization (Cap) Rate: Think of the cap rate as a way to compare the raw earning potential of different properties, almost like comparing a car’s horsepower. It measures the property’s return as if you paid all cash, taking your specific financing out of the equation.

When you're digging into the numbers, don't be afraid to use tools built for the job. A good Veteran Rental DSCR Calculator can be invaluable for quickly seeing if a property’s income can actually support the mortgage payments, which is a critical piece of the puzzle.

A Real-World Financing Scenario

Let’s get practical. Say you've found a single-family home for $300,000. It’s in a decent area, and your research shows you can likely get $2,400 a month in rent. You're planning to put down 20% ($60,000) and you’ve been quoted a 6.5% interest rate.

First things first, you have to account for all the expenses, not just the mortgage. A great rule of thumb for this is the 50% Rule, which assumes that about half your rental income will be eaten up by operating expenses (think repairs, vacancies, taxes, insurance, management—everything except the loan).

- Gross Monthly Income: $2,400

- Estimated Monthly Expenses (50%): $1,200

- Net Operating Income (NOI): That leaves you with $1,200 per month, or $14,400 per year.

Now, let's look at how the loan term impacts your bottom line.

| Metric | 30-Year Fixed Loan | 15-Year Fixed Loan |

|---|---|---|

| Loan Amount | $240,000 | $240,000 |

| Principal & Interest | ~$1,517/month | ~$2,088/month |

| Net Operating Income | $1,200/month | $1,200/month |

| Monthly Cash Flow | -$317/month | -$888/month |

| Cash-on-Cash Return | Negative | Negative |

The numbers don't lie. With a standard 30-year loan, you’re losing money every single month. Going with a 15-year term to build equity faster just digs a deeper hole. This simple calculation is a massive red flag. It’s a clear sign to walk away from this deal unless something changes dramatically, like a lower purchase price or higher rent.

Key Takeaway: Never fall in love with a property—fall in love with a deal. The numbers have to work, period. Your financing terms can single-handedly make or break a deal, so modeling different scenarios before you even think about making an offer is an absolute must.

Optimizing Your Returns by Tweaking the Financing

So, what if we played with the numbers? Let's say you decide to put more skin in the game with a 25% down payment ($75,000). That drops your loan amount to $225,000. On that same 30-year loan, your new mortgage payment is around $1,422. This would cut your monthly loss to -$222. Better, but still not a winner.

This is exactly why you run multiple scenarios. You can see how tweaking the down payment, negotiating the interest rate, or changing the loan term directly impacts your cash flow. The goal is always to find that sweet spot that gives you healthy monthly income while still setting you up for appreciation down the road.

For a much deeper look at this process, check out our guide on using a rental property analyzer spreadsheet to model your own deals from the ground up.

Thinking Outside the Bank: Creative Financing Strategies

While a conventional mortgage is the workhorse of real estate investing, some of the best deals I've seen were snagged by investors who knew how to get creative with their financing. When you move beyond the big banks, you open up a whole world of opportunities that others simply can't touch.

These alternative methods aren't your everyday tools, but having them in your back pocket means you can pounce when a unique property or situation comes along.

Hard Money Loans: When Speed is Everything

Ever find a diamond-in-the-rough property that needs a ton of work? It's a perfect flip, but you know a traditional lender would laugh you out of the office. This is exactly where hard money loans come into play.

Hard money lenders are private outfits that fund short-term loans based on the asset itself—specifically, its potential After-Repair Value (ARV). They're far less concerned with your W-2s and credit score and much more interested in the deal's viability.

Here’s why they’re a go-to for savvy investors:

- Lightning-Fast Closings: We're talking days, not the 30-45 day crawl of a conventional loan. This speed lets you compete head-to-head with all-cash offers.

- Deal-Based Underwriting: Because the loan is secured by the property's future value, they'll fund projects that banks would never approve, like a full gut renovation.

Of course, there's a trade-off. Speed and flexibility come at a price. Expect much higher interest rates, often in the 8-15% range, and very short terms, typically just six to 24 months. Think of a hard money loan as a specialized tool: it’s for getting in, executing the renovation, and getting out—either by selling or refinancing into a more stable, long-term loan.

Seller Financing: Crafting a Win-Win Deal

What if you could cut out the bank entirely? With seller financing, that's exactly what you do. In this setup, the property owner becomes your lender, and you make payments directly to them.

This strategy is perfect when you find a seller who owns their property free and clear or has a lot of equity. They’re often motivated by the idea of creating a steady income stream for themselves in retirement and may even get a better final price.

For you as the buyer, the advantages are massive. You can often negotiate flexible terms like a smaller down payment, a better interest rate, or even interest-only periods. Plus, closing costs are usually a fraction of a bank-financed deal. It's a powerful way to lock down a property when you don't fit into the rigid box of conventional lending. If this sounds interesting, it's crucial to understand how a seller note is structured to make sure the agreement is solid for everyone involved.

A Classic Scenario: I once saw an investor find a tired landlord ready to retire. The property was in good shape but dated. The investor proposed a fair price with 10% down and a 5-year balloon payment, paying the seller monthly. The seller locked in a reliable income without the landlord headaches, and the investor acquired a fantastic asset without ever talking to a loan officer.

Using Your Home Equity as a Launchpad

If you're a homeowner with a good chunk of equity, a Home Equity Line of Credit (HELOC) might be the most powerful financing tool you have. A HELOC is essentially a credit card secured by your house—a revolving line of credit you can tap into as needed, only paying interest on what you actually borrow.

This makes a HELOC an incredible source for a down payment. You could pull $50,000 from your HELOC to cover the 20% down on a new rental property, then get a standard mortgage for the other 80%. Just like that, you've acquired a new asset while keeping your cash reserves full for any unexpected repairs.

The key here is to be smart and disciplined. You are leveraging your own home, so you need to be absolutely certain the investment property will generate positive cash flow to cover its own mortgage and help you pay back the HELOC. The goal is to use it as a short-term bridge to acquire a cash-flowing property, not as a permanent loan.

Getting Your Loan Application Ready for Prime Time

Alright, you've got a great property in your sights and a solid idea of how you want to finance it. Now for the part where the rubber meets the road: proving to the lender that you're an investor they can bet on. A clean, well-organized loan application does more than just speed up the process—it screams professionalism and can genuinely impact the terms you're offered.

Think of it this way: your application tells the story of your financial life. Your job is to make that story so clear and compelling that the underwriter has zero questions. Every document should be legible, every number should tie out, and any potential oddities should be explained before they even have a chance to ask.

Get Your Paperwork in Order

In an underwriter's world, if it isn't documented, it didn't happen. The very first thing you should do is create a digital folder and start gathering all the financial paperwork they'll inevitably ask for. Having this ready from day one shows your loan officer you're serious and organized, which sets a great tone for the entire relationship.

Here's a pretty standard list of what you'll need to pull together:

- Income Verification: Typically, this means your last two years of W-2s and your most recent pay stubs covering a 30-day period.

- Tax Returns: Plan on providing your full federal tax returns for the past two years, including all schedules. Don't leave anything out.

- Bank Statements: Lenders will want to see at least two months of statements for every single one of your accounts—checking, savings, and investment. Make sure you include all the pages, even the blank ones.

- Asset Statements: This is where you show your reserves and net worth. Pull recent statements from your brokerage accounts, 401(k)s, IRAs, and any other investment vehicles.

- Personal ID: A clear copy of your driver’s license and Social Security card is always required.

- Your Current Real Estate: If you're already an owner, have the latest mortgage statements, property tax bills, and homeowners insurance declaration pages for each property handy.

Dealing with Underwriting's Curveballs

Look, nobody's financial picture is perfect, and lenders know that. A few complexities are expected. The real test is how you explain them. The key here is to be proactive. Getting ahead of potential questions is how you avoid those frantic, last-minute scrambles that can put your entire deal at risk.

The two things that almost always raise an eyebrow are large, random-looking deposits and any dings on your credit report. Don't sit back and wait for the underwriter to flag them. Get out in front of it with a Letter of Explanation (LOX).

A LOX is just a simple, signed letter that clarifies a financial event. That’s it.

My Two Cents: Keep your Letter of Explanation short, sweet, and to the point. State the facts, give a simple reason, and confirm the issue is resolved. For that big deposit, you might write, "On May 15th, I deposited $10,000 into my checking account. This was from the private sale of my 2022 Honda CR-V. I've attached a copy of the bill of sale for your reference."

When you address these things upfront, you're building trust and showing you've got nothing to hide. It tells the lender you're a responsible borrower who has their financial house in order. Honestly, a well-prepared application file is one of your best assets when financing an investment property, turning what could be a headache into a smooth and predictable path to the closing table.

From Pre-Approval to Closing Day: The Final Lap

Getting that pre-approval letter feels like a major win, and it is! But don't pop the champagne just yet. The sprint from getting your offer accepted to finally getting the keys is where the real work happens. This final stretch is packed with checkpoints that can either solidify your deal or send it sideways. Staying organized and ahead of the game is everything here.

Think of your pre-approval as your entry ticket. It proves to sellers you’re not just a window shopper; you're a serious buyer with the financial muscle to see the deal through. In a hot market, submitting an offer without a solid pre-approval is like showing up to a gunfight with a knife. It's your single most powerful piece of leverage before you've even made an offer.

Clearing the Appraisal and Inspection Hurdles

Once your offer is accepted, the clock starts ticking. Fast. Two of the biggest milestones you’ll hit next are the property appraisal and the home inspection. People often confuse them, but they serve two very different—and equally critical—purposes.

The Appraisal: This is all about the lender's peace of mind. An independent appraiser determines the property's fair market value. Why? The bank needs to be sure they aren't lending you more money than the asset is actually worth. If the appraisal comes in low, you're looking at a negotiation with the seller, bringing more cash to the table, or potentially walking away.

The Inspection: This one is all for you. A professional inspector will comb through the property, from the shingles on the roof to the cracks in the foundation. This is your chance to uncover hidden nightmares that could turn into budget-busting repairs later. A bad inspection report isn't necessarily a dead end; it’s ammunition for negotiating repairs or a price cut.

A low appraisal isn't an automatic deal-killer, but it forces a conversation. A rough inspection report gives you the power to renegotiate or walk away with your earnest money.

The Closing Process: Signing on the Dotted Line

While you're dealing with inspections and appraisals, your lender's underwriting team is in the background, scrutinizing every last detail of your file. Once they give the final sign-off, you'll get the magic words: "clear to close."

Now you're in the home stretch. At least three business days before your closing date, you'll receive a critical document called the Closing Disclosure (CD).

Pay attention here: this document is the final, official breakdown of your loan and all associated costs. Go through every single line item on that CD. Compare it to the Loan Estimate you received at the beginning to make sure there are no last-minute surprises. Check the loan amount, interest rate, closing costs, and the final "cash-to-close" figure.

The closing itself is the grand finale. You’ll sit down with a closing agent or attorney and sign a stack of documents that feels a mile high. The two most important ones are the Promissory Note (your formal IOU to the lender) and the Deed of Trust (the document that secures the property as collateral).

Once the ink is dry and the funds have been wired, the keys are yours. Congratulations—you’ve officially financed your first (or next) investment property.

Ready to stop guessing and start analyzing deals with confidence? Property Scout 360 gives you the tools to run the numbers on any U.S. property in seconds. Find your next investment and calculate its true potential at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.