A Practical Guide to DSCR Real Estate Investing

Unlock profitable deals with our guide to DSCR real estate. Learn what DSCR means, how lenders use it, and strategies to improve your property's cash flow.

When you get into dscr real estate, you quickly learn that one metric stands above the rest: the Debt Service Coverage Ratio. Think of it as a vital sign for your investment property. It's the one number that tells you—and more importantly, your lender—if the property can actually pay its own mortgage.

A higher DSCR isn't just a good sign; it points to a healthier, more durable investment.

Why DSCR Is Your Financial Safety Net

Picture your rental property as its own little business. The rent you collect is the revenue, and the biggest, most consistent expense is the mortgage. DSCR is simply a way to measure if that revenue is enough to cover the mortgage, with a cushion left over. It’s the property’s financial breathing room.

This isn’t just some number on a spreadsheet; it’s a very real tool for survival in the investing world. A solid DSCR acts as a buffer against the surprises that every landlord eventually faces.

- Sudden Vacancies: When a tenant moves out unexpectedly, that income surplus means you can still make the mortgage payment without having to raid your personal bank account.

- Unexpected Repairs: A water heater that gives up the ghost or a roof that starts leaking won't derail your investment if the property is already generating extra cash each month.

- Economic Downturns: In a soft market, you might have to lower the rent to attract or keep tenants. A good DSCR gives you the wiggle room to do that without going into the red.

The Lender's Point Of View

For a lender, DSCR is the primary yardstick for measuring risk on an income-property loan. They're looking past your personal credit score and focusing on the asset's ability to perform. A strong DSCR proves the investment itself is solid, which makes getting a loan much easier.

In fact, most lenders set a minimum DSCR, often around 1.25. This means they want to see the property bringing in 25% more income than what's needed for the debt payments. You can learn more about how this impacts your bottom line in our guide to what is cash flow in real estate.

A low DSCR is a red flag for a lender. It tells them even a small hiccup could put the loan at risk of default. A high DSCR, on the other hand, shows them a property with a strong income stream that can handle some financial stress.

At the end of the day, getting a handle on dscr real estate principles is essential for any serious investor. It’s the key to finding good deals, securing the best financing, and building a rental portfolio that can stand the test of time. For a broader look at the DSCR concept and how it applies to business loans in general, this What Is DSCR: A Simple Guide to Debt Service Coverage Ratio is a great resource.

Calculating DSCR for Your Investment Property

Knowing what DSCR is in theory is one thing, but running the numbers on a live deal is where the rubber really meets the road. The formula itself looks simple, but its power—and its accuracy—depends entirely on getting the two main components right.

The core formula is: DSCR = Net Operating Income (NOI) / Total Debt Service

Think of it as a quick financial health check for your property. Is the income it generates (the NOI) actually enough to cover its biggest bill (the mortgage)? Let's break down both sides of that equation.

Breaking Down Net Operating Income

First things first, you need to pin down the property's Net Operating Income (NOI). This number is your property's pure profit before you even think about the mortgage payment. It’s all the revenue the property brings in, minus all the necessary expenses to keep it running smoothly. To really get DSCR right, you have to have a solid handle on Net Operating Income (NOI).

Here’s how you get to your NOI, step-by-step:

- Figure Out Gross Potential Income: This is your best-case scenario—the total rent you’d collect if the property was 100% occupied all year long.

- Factor in Vacancy and Credit Loss: Let's be real, no property stays full forever. You need to subtract a realistic percentage for empty units or tenants who don't pay. A common estimate is 5-8%, but this can vary by market.

- Subtract All Operating Expenses: Now, deduct every cost associated with the day-to-day operation of the property. And just to be clear, this does not include the mortgage payment.

Key Takeaway: Getting your operating expenses right is absolutely critical. This list includes property taxes, insurance, any property management fees, routine maintenance, utilities (if you're paying them), and setting aside cash for big-ticket items down the road, like a new roof or HVAC system.

Understanding Total Debt Service

The second piece of the puzzle, Total Debt Service, is much more straightforward. It’s simply the total amount of principal and interest you'll pay on your loan over a single year.

So, if your monthly mortgage payment (principal and interest) is $1,500, your annual debt service is $18,000 ($1,500 x 12). Easy as that.

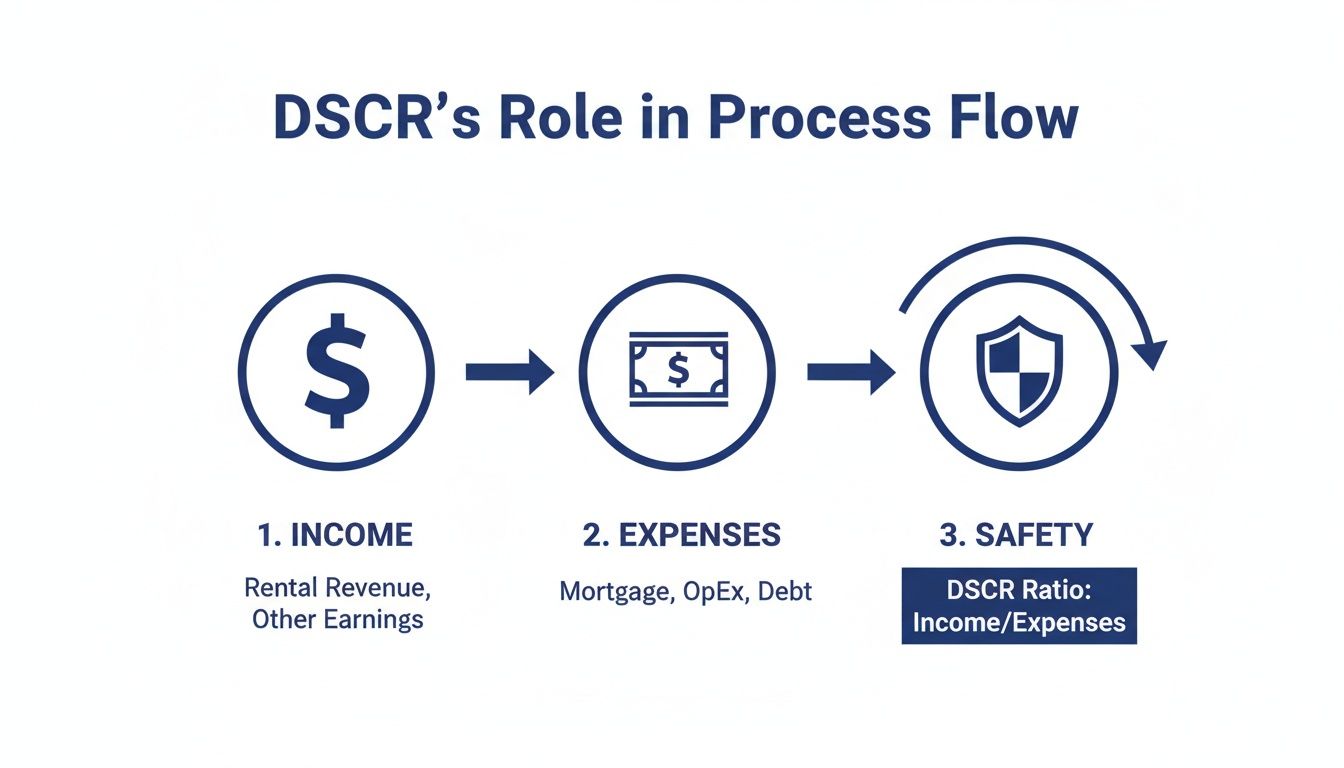

This flowchart really helps visualize how all the income and expenses flow together to create that all-important financial safety margin.

As the graphic shows, after you've covered all your operating costs, the income left over has to be enough to handle the debt and, ideally, leave you a buffer.

A Real-World Calculation Example

Alright, let's walk through an example with a single-family rental property to make this tangible.

- Monthly Rent: $2,500

- Monthly Operating Expenses (Taxes, Insurance, Maintenance): $600

- Monthly Mortgage Payment (Principal & Interest): $1,500

Step 1: Calculate Annual NOI

- Gross Annual Income: $2,500 x 12 = $30,000

- Vacancy Loss (at 5%): $30,000 x 0.05 = $1,500

- Effective Gross Income: $30,000 - $1,500 = $28,500

- Annual Operating Expenses: $600 x 12 = $7,200

- Final NOI: $28,500 - $7,200 = $21,300

Step 2: Calculate Annual Debt Service

- Annual Debt Service: $1,500 x 12 = $18,000

Step 3: Calculate the DSCR

- DSCR = $21,300 (NOI) / $18,000 (Debt Service) = 1.18

A DSCR of 1.18 tells you the property generates 18% more income than it needs to cover the mortgage. That’s your safety cushion, quantified.

While doing these calculations by hand is a great way to learn, a good rental property analyzer spreadsheet can automate the entire process, helping you avoid simple mistakes that could cost you big time.

What Lenders Look for in Your DSCR

As a real estate investor, you crunch the numbers to make sure a deal works for you. But to get a loan, you have to see things from the lender's side. For them, your Debt Service Coverage Ratio isn't just another number—it's the single most important gauge of risk for an investment property.

When a lender underwrites a loan, they aren't nearly as interested in your personal W-2 income as they are in the property's ability to stand on its own financial feet. Can it generate enough cash to pay its own bills, including their mortgage payment?

This intense focus on the asset is exactly why dscr real estate loans are so popular. These loans let investors scale their portfolios based on the performance of the properties themselves, not just their personal tax returns. A strong DSCR tells a lender that the investment is solid and can handle minor bumps in the road, like a short vacancy or a surprise repair, without missing a mortgage payment.

The Minimum Thresholds

While the exact numbers can vary, almost every lender has a hard-and-fast minimum DSCR they require. If your deal falls below this line, it’s often an automatic "no." On the flip side, comfortably exceeding it can open the door to much better loan terms.

The most common minimum DSCR you'll see is 1.20 or 1.25. What this means is the lender needs to see that the property brings in at least 20-25% more income than what's needed to cover its total annual debt payments. This extra cash serves as a crucial safety net for both you and the bank.

Think of it this way: a DSCR of 1.0 means the property is just breaking even on its debt. To a lender, that’s a tightrope walk without a net. Any little thing—a late rent check, a clogged pipe—could push the property into negative cash flow and put their loan at risk.

How Your DSCR Impacts Loan Terms

Your DSCR doesn't just decide whether you get the loan; it directly shapes the quality of the loan you're offered. A higher DSCR lowers the lender's perceived risk, which gives you more leverage at the negotiating table.

While DSCR is king, it's worth noting that for some commercial properties, lenders also look at metrics like debt yield. You can dive deeper into that topic in our guide explaining what is debt yield.

Here’s a quick look at how lenders typically interpret different DSCR levels and what that means for your financing.

Lender DSCR Thresholds and Loan Implications

This table breaks down how a lender might view your deal based on its DSCR.

| DSCR Ratio | Lender's Risk Assessment | Typical Loan Outcome |

|---|---|---|

| Below 1.15 | High Risk | The loan application is very likely to be denied. |

| 1.15 – 1.25 | Acceptable / Borderline | May get approved, but expect a higher interest rate or lower LTV. |

| 1.25 – 1.50 | Good / Low Risk | You have a strong chance of approval with standard, competitive terms. |

| Above 1.50 | Excellent / Very Low Risk | High likelihood of approval with the best possible interest rates and terms. |

As you can see, a stronger DSCR makes you a more attractive borrower. At the end of the day, walking into a bank with a deal that boasts a robust DSCR is the surest way to get their attention and secure the financing you need. It proves your investment isn't just a speculative bet but a well-vetted, income-producing asset ready to perform.

Actionable Strategies to Improve Your Property's DSCR

Don't panic if a property you're analyzing has a low DSCR. It's not necessarily a deal-breaker. Instead, see it for what it is: a sign that there's room for improvement and a chance to get creative.

Whether you're underwriting a new purchase or trying to get more out of a property you already own, improving your dscr real estate ratio boils down to pulling two main levers. The entire game is about the formula: NOI divided by Debt Service. To make that number bigger, you can either grow the top number (NOI) or shrink the bottom one (Debt Service).

Let's break down how to attack both sides of the equation.

Boosting Your Net Operating Income

This is where your skills as an operator really shine. Pumping up your Net Operating Income is the most fundamental way to improve a property's financial health and its DSCR. It’s a two-pronged attack: bring in more cash and spend less of it, all without letting the property's quality slip.

1. Increase Rental Income

The simplest way to a higher NOI is to charge more rent. This doesn't mean slapping a 20% increase on everyone and hoping for the best. It means making smart, strategic adjustments backed by solid data. Run the comps in your area to see what similar properties are getting. Are you leaving money on the table?

You can also earn the right to charge more by making value-add improvements tenants are happy to pay for. Think about things like:

- Swapping out old kitchen appliances and laminate countertops for stainless steel and granite.

- Adding in-unit washers and dryers—a huge convenience factor.

- Installing modern amenities like smart thermostats or offering reserved parking spots.

2. Reduce Operating Expenses

The other side of the NOI coin is trimming the fat. It’s amazing what you can find when you actually audit a property's expenses line by line. You can often find significant savings by challenging your property tax assessment, getting new insurance quotes every single year, or making one-time investments in energy efficiency. Swapping out old light fixtures for LEDs or installing low-flow toilets can noticeably reduce your utility bills over time.

A small, $100 monthly reduction in operating expenses adds $1,200 directly to your annual NOI. This single change can be enough to push a borderline deal into a lender's acceptable DSCR range.

Optimizing Your Debt Service

While boosting NOI is all about hands-on property management, tweaking your debt service is a purely financial play that can have just as big of an impact on your DSCR. The mission here is simple: make your total annual mortgage payments smaller.

Here are a few ways to get it done:

- Refinance for a Lower Interest Rate: This is the most obvious move. If rates have dropped since you got your original loan, a refinance can slash your monthly payment and, by extension, your total annual debt service.

- Extend the Loan Term: Stretching your loan from a 15-year to a 30-year amortization schedule will immediately lower your monthly payments. Yes, you’ll pay more in interest over the long haul, but it frees up cash flow and gives your DSCR a healthy boost right now.

- Increase Your Down Payment: When buying a new property, putting more cash down reduces the amount you have to borrow. A smaller loan automatically means smaller payments, which sets up your DSCR for success from the very beginning.

By mixing and matching these income-boosting and debt-reducing strategies, you can take a deal with a shaky DSCR and turn it into a solid, bankable asset. This is what separates savvy dscr real estate investors from the rest of the pack.

How DSCR Fits with Other Key Real Estate Metrics

Relying only on DSCR is like a doctor checking just your blood pressure—it's a critical vital sign, but it doesn't tell the whole story. A smart real estate investor never looks at one number in a vacuum. You need a full toolkit of metrics to properly diagnose a deal from every angle.

Think of it as a complete financial check-up for your potential investment. Each metric asks a different, essential question about the property's performance and how it aligns with your goals.

To make a truly solid decision, DSCR needs to be analyzed right alongside two other heavy hitters: the Capitalization Rate (Cap Rate) and the Cash-on-Cash Return.

Cap Rate: Your Market Thermometer

The Cap Rate is your first, fastest diagnostic tool. It gives you a snapshot of a property’s potential return as if you bought it with all cash. The formula is straightforward: NOI / Property Price.

This number is perfect for comparing different properties in the same market. It’s like taking a quick temperature reading to see how hot an investment is relative to its neighbors. A high cap rate might point to a higher return, but it can also signal higher risk. A low cap rate usually suggests a safer, more stable property in a prime location. It’s all about the market’s perception of value.

Cash-on-Cash Return: Your Personal ROI

While Cap Rate completely ignores financing, Cash-on-Cash Return puts it front and center. This metric answers the most personal question every investor asks: "How hard is my own money actually working for me?"

You calculate it by dividing your annual pre-tax cash flow by the total cash you invested out-of-pocket (your down payment, closing costs, and initial repair funds). This percentage shows the direct return on the money you actually pulled from your bank account. It’s why two properties with identical prices and DSCRs can have wildly different cash-on-cash returns, all because of how the deal is financed.

The Full Diagnosis:

- Cap Rate checks the deal’s health against the market.

- Cash-on-Cash Return checks its health for your personal wallet.

- DSCR checks its ability to handle the stress of debt.

Using these three metrics together gives you a complete, 360-degree view. A property might have a fantastic DSCR, but a low Cap Rate and a weak Cash-on-Cash Return could mean you're overpaying. Another deal might boast a stellar Cap Rate, but if the DSCR is below 1.20, good luck getting a lender to say yes.

A complete analysis using all three isn't just a good idea—it's non-negotiable for smart investing.

Diving Deeper: Your DSCR Questions Answered

As you start working with DSCR, a few questions always seem to come up. Let's tackle the most common ones so you can analyze your next deal with total confidence.

What’s a Good DSCR for a Rental Property?

If you're looking for a benchmark, 1.25 is the magic number for most lenders. Think of it as the industry standard. A 1.25 DSCR tells the bank that your property generates 25% more income than it needs to pay its mortgage and other debts. That extra cash flow acts as a crucial safety net.

Of course, this isn't set in stone. The "right" DSCR really depends on the deal. A lender might be perfectly fine with a slightly lower ratio on a brand new, Class A apartment building in a booming neighborhood. On the other hand, for an older property with more potential risks, they'll want to see a healthier cushion—maybe 1.35 or even higher.

Do Lenders Look at Anything Besides DSCR?

You bet they do. While DSCR is the main event for investment property loans, lenders are still looking at the whole picture to make sure you're a solid borrower.

They’ll also want to see:

- Loan-to-Value (LTV): Lenders need to know you have some skin in the game. You'll typically need to put down at least 20-25%, which keeps your LTV in that 75-80% range.

- Credit Score: It's not the deal-breaker it can be with a primary home mortgage, but a good credit score definitely helps build the lender's confidence.

- Experience: Have you managed rentals before? A proven track record shows you know how to handle the inevitable challenges of being a landlord.

- Cash Reserves: Lenders sleep better at night knowing you have enough cash on hand to cover several months of mortgage payments if the property sits vacant for a bit.

How Do Variable Expenses Affect DSCR Calculations?

This is a huge one, and it trips up a lot of new investors. When you're calculating your Net Operating Income (NOI), you have to be brutally honest about your variable expenses—things like maintenance, unexpected repairs, and saving for big-ticket items (we call this CapEx).

Lenders have seen it all, and they have their own standards. If your projections look a little too rosy, they'll adjust them.

Let's say you budget 5% of your gross rent for maintenance. The lender might look at the age of the property and the local market and say, "Our standard for a property like this is 8%." They'll use their number, not yours, which will lower your NOI and, in turn, your DSCR. The lesson? Always be conservative with your expense estimates.

Tired of running these numbers by hand? Property Scout 360 takes the guesswork out of the equation. It instantly calculates DSCR, cash flow, and ROI, giving you the clarity you need to grow your portfolio with confidence. See how Property Scout 360 can transform your real estate investing.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.