The Ultimate Guide to BRRRR Method Real Estate Investing

Discover how the BRRRR method real estate strategy works. This guide breaks down how to buy, rehab, rent, refinance, and repeat your way to a larger portfolio.

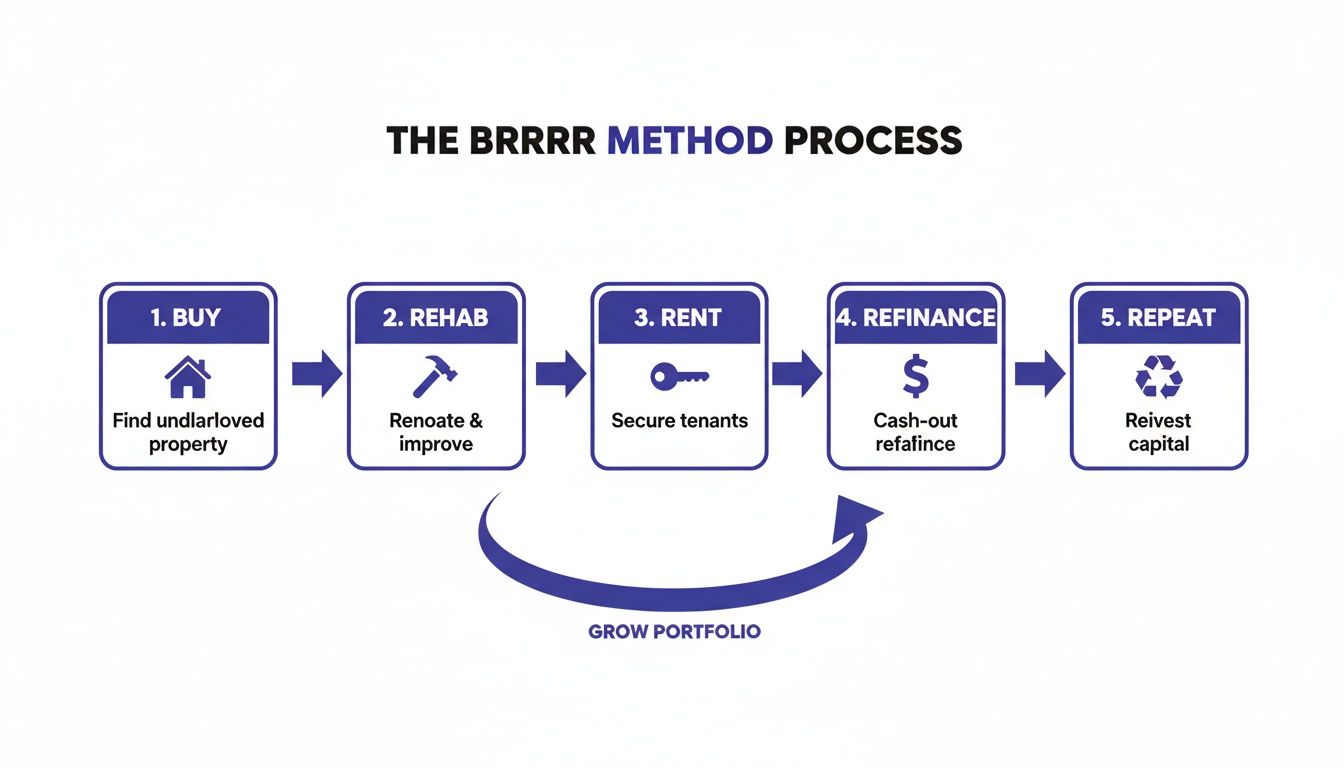

The BRRRR method in real estate is an incredible cycle for building a rental property portfolio. I've used it myself to scale much faster than I ever thought possible. The concept is simple: you Buy a property that needs work, Rehab it to force appreciation, Rent it out to a solid tenant, Refinance to pull your original investment back out, and then Repeat the whole process on the next deal.

Think of it as a system designed to use the same pot of money over and over again to buy multiple cash-flowing rentals.

A Blueprint for Rapid Portfolio Growth

At its heart, the BRRRR method is all about creating equity from thin air and then recycling your cash. It's a world away from the traditional real estate buy and hold strategy, where your down payment sits locked up in one property for years. With this approach, your initial investment becomes a powerful, reusable tool.

You're not just buying an asset off the shelf; you're actively creating its value.

The real magic trick happens during the refinance. Once the dust settles from the renovation and you have a paying tenant, the property should be worth a lot more than what you have into it. The goal is to get a new loan based on this higher After-Repair Value (ARV). This new loan pays off your original purchase and rehab financing, and ideally, puts all of your initial cash right back in your pocket.

This flowchart breaks down the five stages beautifully.

As you can see, each step flows right into the next, creating a repeatable cycle that can seriously build wealth if you do it right.

To get a clearer picture of how each stage fits into the bigger strategy, here’s a quick breakdown.

The Five Stages of The BRRRR Method At a Glance

| Stage | Primary Objective | Key Success Indicator |

|---|---|---|

| Buy | Acquire a distressed property significantly below its market value. | Purchase price is low enough to allow for rehab costs and instant equity. |

| Rehab | Force appreciation by renovating the property to modern standards. | The After-Repair Value (ARV) is substantially higher than total costs. |

| Rent | Secure a qualified tenant and establish a consistent rental income stream. | Rent covers mortgage, taxes, insurance, and expenses, with positive cash flow. |

| Refinance | Secure a new long-term loan based on the property's new, higher value. | A cash-out refinance allows you to pull out most, or all, of your initial capital. |

| Repeat | Use the recovered capital to fund the purchase of the next property. | Successfully starting the cycle over again with little to no new money out of pocket. |

This table really highlights the goal for each step. Master these, and you're well on your way.

Maximizing Your Capital

The true power here is how efficiently you can use your money. Let's run some quick numbers. Buying five houses worth $200,000 each with a conventional 20% down payment would tie up $200,000 of your cash ($40,000 x 5).

With the BRRRR strategy, you could potentially buy those same five properties using just the initial capital from the first deal. You just keep recycling it from one project to the next. This puts portfolio growth into hyperdrive compared to the slow-and-steady method of saving up for each down payment.

The BRRRR method is all about velocity—how fast you can put your capital back to work. When you get this right, your growth is no longer limited by how much you can save, but by how many great deals you can find.

This isn't a passive strategy, though. It demands a hands-on approach and a sharp understanding of local market values, renovation costs, and financing options. A big piece of the puzzle is also understanding the various tax advantages of rental property.

In the next sections, we'll get into the nitty-gritty and break down each stage with actionable advice to help you pull this off.

Finding and Analyzing a Profitable BRRRR Deal

The entire success of your BRRRR project hinges on this first, critical phase: buying the right property. This isn't just about snagging a cheap house. It's about finding an undervalued asset where you can force appreciation and strategically manufacture equity.

Frankly, the best BRRRR method real estate deals are rarely the ones sitting polished and pretty on the MLS. You have to dig a little deeper.

Your search strategy should be a two-pronged attack, covering both on-market listings and off-market opportunities. This dual approach is key to finding that diamond in the rough before everyone else does.

This image perfectly captures the cyclical nature of the BRRRR method, and it all starts with making a smart purchase.

Sourcing On-Market and Off-Market Deals

On-market deals are the ones everyone sees, publicly listed on the Multiple Listing Service (MLS). You can spot potential winners by looking for properties that have been on the market for a long time, are explicitly listed "as-is," or have descriptions that scream neglect—think "TLC needed" or "contractor special." These are often clues that you're dealing with a motivated seller.

Off-market deals, though, are where many seasoned investors truly make their money. These properties aren't publicly for sale, which means you have to be proactive to find them.

- Driving for Dollars: It sounds old-school, but it flat-out works. Drive through neighborhoods you want to invest in and look for visible signs of distress—overgrown lawns, peeling paint, boarded-up windows. Jot down the addresses and use public records to find the owner's contact info.

- Networking: Start building real relationships with wholesalers, real estate attorneys, contractors, and local property managers. These are the people who often hear about homeowners looking to sell quickly and quietly before anyone else.

- Direct Mail: A targeted direct mail campaign can be surprisingly effective. Sending letters to owners of distressed or inherited properties can generate great leads, but it requires consistency to pay off.

Once you have a potential property in your sights, the real work begins. It’s time to analyze the numbers and separate the true opportunities from the money pits.

The Foundation of Your Analysis: After-Repair Value

Before you even think about making an offer, you absolutely must know what the property will be worth after you’ve fixed it up. This is the After-Repair Value (ARV), and it is single-handedly the most important number in your entire BRRRR calculation. Getting this wrong can kill the project before it even starts.

To pin down an accurate ARV, you need to pull comparable sales, or "comps." The gold standard is finding at least three similar properties that have sold within the last six months, are located in the immediate vicinity, and closely match your target property's features—square footage, bed/bath count, and lot size.

For instance, say you find a distressed house for $115,000 that needs $20,000 in repairs. If fully renovated, comparable homes in the area are consistently selling for $180,000, then your ARV is $180,000. This pits your total investment of $135,000 against that future value.

The goal of the BRRRR method isn't just to buy a rental. It’s to create so much equity through the rehab that the bank is willing to give you all your initial investment back during the refinance. This is impossible without a rock-solid ARV.

Applying the 70 Percent Rule

With a reliable ARV estimate in hand, you can use a crucial underwriting guideline: the 70% Rule. This is a quick and dirty rule of thumb that helps you determine your maximum allowable offer (MAO) on a property.

The formula is simple:

(ARV x 0.70) - Estimated Repair Costs = Maximum Allowable Offer

Let's plug in the numbers from our example:

- ARV = $180,000

- Estimated Repairs = $20,000

Here’s the math: ($180,000 x 0.70) - $20,000 = $126,000 - $20,000 = $106,000.

This calculation tells you that to make this deal work and protect your downside, you shouldn't pay a dime over $106,000 for the property. That 30% cushion is your buffer for holding costs, financing fees, unexpected issues, and—most importantly—your profit.

Manually crunching these numbers can involve a lot of spreadsheets and hours of research. For a deeper dive into the nitty-gritty, check out our complete guide on how to analyze a rental property. Thankfully, modern tools can do the heavy lifting. Platforms like Property Scout 360 can automate these calculations, pull comps, and project cash flow in minutes, letting you make confident, data-backed offers much faster.

Getting the Rehab Right: Smart and Profitable Renovations

This is where the magic happens. The rehab phase is the engine of the entire BRRRR method real estate strategy, the part where you actively force appreciation and turn a tired property into a performing asset. It's also the place where poorly managed budgets and timelines can sink your entire project.

Success here isn't about creating your dream home. It’s about making targeted, strategic upgrades that boost the property's future appraised value and its rent potential. Every single dollar has to pull its weight.

That means choosing durability and broad tenant appeal over your own personal taste. We're talking about vinyl plank flooring that can handle years of wear and tear, not delicate hardwood. We're focused on fresh, neutral paint and clean, functional kitchens and baths—not high-end finishes that a renter won't pay extra for and an appraiser won't give you full credit for.

Your Blueprint for Success: The Scope of Work

Before a single hammer swings, you need a detailed Scope of Work (SOW). This document is the constitution for your project. It meticulously lists out every task, material, and finish. A vague note like "update kitchen" is a one-way ticket to budget overruns and contractor disputes.

A solid SOW gets granular. For instance:

- Kitchen: Demo existing laminate countertops and backsplash. Install new Giallo Ornamental granite countertops. Install new Moen single-basin stainless steel sink and high-arc faucet (Model #7594). Prep, sand, and paint all existing cabinets with Sherwin-Williams ProClassic in "Pure White" (SW 7005), semi-gloss finish.

- Flooring: Tear out and dispose of all existing carpet and pad in the living room and three bedrooms. Install LifeProof Luxury Vinyl Plank flooring in "Sterling Oak" color throughout, including new quarter-round trim.

- Electrical: Replace all existing outlets and light switches with new white Leviton Decora-style fixtures. Supply and install two 52" Hunter ceiling fans (Model #53091) in the living room and master bedroom.

This level of detail is absolutely non-negotiable. It forces your contractors to bid on the exact same job, giving you a true apples-to-apples comparison. It also eliminates ambiguity and protects you from those dreaded "surprise" charges down the road. Building out a plan like this is crucial, and the discipline is similar to what's needed for other real estate projects. In fact, our definitive house flipping checklist offers a great framework you can easily adapt for a BRRRR rehab.

The quality of your Scope of Work is directly tied to the success of your rehab. A detailed SOW kills budget creep, holds your crew accountable, and becomes the foundation of a solid contract.

Finding and Managing Your Contractor

During the rehab, your contractor is the most critical member of your team. The right one makes the process feel effortless. The wrong one can quickly turn your investment into a financial and emotional nightmare. Never, ever go with the first or cheapest bid.

Your vetting process has to be thorough:

- Get Multiple Bids: Always get at least three detailed bids based on your identical, iron-clad SOW.

- Check References: Don't just get a list of names—call them. Ask specific questions: Did they stick to the budget? How did they handle problems? Were you happy with the quality? Would you hire them again?

- Verify Their Paperwork: A legitimate pro will have no issue showing you their license and proof of general liability insurance. This isn't just a formality; it protects you from massive liability if someone gets injured on your job site.

Once you’ve picked your contractor, put a clear payment schedule in writing, tying payments to specific, completed milestones. Never pay a huge amount of money upfront. A standard draw schedule might look like 10% at signing, with the next payments released only after key phases (like demolition, plumbing rough-in, or drywall) are finished and have passed your inspection.

Focus on Renovations That Add Real Value

When you're mapping out your budget, you have to be surgical. Put your money where it will give you the biggest bang for your buck with appraisers and prospective tenants. The goal is to maximize the property’s value, not to over-renovate it for the neighborhood.

Here’s a look at how a budget for a standard rental-grade rehab often breaks down, concentrating on the high-impact items:

| Category | Typical Cost Allocation | Key Focus Areas |

|---|---|---|

| Kitchen & Bath | 40% - 50% | New countertops, refinished cabinets, updated fixtures, modern appliances. |

| Flooring | 15% - 20% | Durable and waterproof materials like Luxury Vinyl Plank (LVP). |

| Paint (Interior & Exterior) | 10% - 15% | Neutral, bright colors to make spaces feel larger and boost curb appeal. |

| Fixtures & Hardware | 5% - 10% | Modern lighting, ceiling fans, doorknobs, and cabinet pulls. |

| Contingency Fund | 10% - 15% | Never skip this. This is for the surprises hiding behind the walls. |

This table shows you where the value is. Kitchens and bathrooms sell houses and rent apartments. By pouring your rehab budget into these key areas, you directly influence the After-Repair Value (ARV)—the number that matters most when it's time to refinance.

Securing Tenants And Mastering The Refinance

With the dust settled and the paint dry, your renovated property is no longer a construction site—it’s a cash-flowing asset in the making. This is where you pivot from creating value to capturing it. The next two steps, Rent and Refinance, are completely intertwined. Landing a great tenant gives you the proof of income a lender needs for the cash-out loan that makes the whole BRRRR method real estate cycle work.

Your newly rehabbed property should look incredible, but you still have to market it. High-quality photos are non-negotiable. They are your first impression online and can mean the difference between a flood of applications and radio silence. Get the property listed on the major rental platforms, and don't underestimate the power of a simple "For Rent" sign in the yard.

Placing The Right Tenant

The quality of your tenant can make or break your entire experience as a landlord. Rushing this step is a classic rookie mistake. A thorough, consistent screening process is your best defense against late payments, property damage, and the nightmare of eviction.

Your screening process should be identical for every single applicant to ensure you're compliant with fair housing laws. Here's what it must include:

- Credit Check: Look for a solid history of paying bills on time. The score itself is just one piece of the puzzle; the details are what really matter. A low score from old medical debt is a completely different story than recent, unpaid rent to a previous landlord.

- Background Check: This is crucial for verifying identity and screening for any relevant criminal history that could pose a risk.

- Income Verification: The gold standard is that a tenant's gross monthly income should be at least three times the monthly rent. Don't just take their word for it—always verify with recent pay stubs, offer letters, or other official documents.

- Rental History: Actually call their previous landlords. Ask the important questions: Did they pay on time, every time? Did they take good care of the property? Would you rent to them again? The last question is the most telling.

Once you’ve found your ideal tenant, get a lease signed and collect the security deposit. That signed lease isn't just a legal formality; it's the golden ticket you'll show your lender to prove the property is a stabilized, income-producing asset.

Navigating The Cash-Out Refinance

With a tenant in place and rent checks hitting your account, it's time to talk to a lender about the cash-out refinance. This is the moment that makes the "Repeat" phase possible. The goal is simple: get a new, long-term loan based on the property's After-Repair Value (ARV), not the low price you originally paid for it.

The refinance is your payday. It’s where you prove your investment thesis was correct, recoup your initial capital, and unlock the funds to do it all over again. A successful refinance is the ultimate validation of a well-executed BRRRR project.

Of course, lenders have specific hoops you need to jump through. Knowing what they're looking for ahead of time is the key to a smooth closing. A huge part of this is knowing exactly how to calculate property value so you can walk in confidently and maximize your equity pull.

Understanding Lender Requirements

Not all lenders get the BRRRR strategy. You need to find an investor-friendly bank or mortgage broker who understands what you’re doing. Big national banks can be rigid and bureaucratic, whereas smaller community banks and local credit unions are often much more flexible with investors.

Here are the main things they'll be looking at:

- Seasoning Period: This is a mandatory waiting period a lender requires before they'll even consider a refinance. It typically runs six to twelve months from your purchase date. This rule exists to prevent fraudulent flips and ensure the new value is legitimate.

- Loan-to-Value (LTV): Lenders will only loan you a certain percentage of the new appraised value. For investment properties, this is typically 70-80% LTV. So, if your property appraises for $200,000 and the lender’s max LTV is 75%, your loan will be capped at $150,000.

- Debt-to-Income (DTI): The bank will dig into your personal finances to make sure you can comfortably cover all your existing debts plus the new mortgage payment.

- Credit Score: A strong personal credit score is non-negotiable for getting the best interest rates and loan terms.

This table gives you a snapshot of what to expect when you approach a lender for a BRRRR deal.

Typical Lender Requirements for a BRRRR Refinance

| Requirement | Typical Range/Rule | Why It Matters |

|---|---|---|

| Seasoning Period | 6-12 months | Prevents fraudulent flips and ensures the property's value is stable before the new loan. |

| Loan-to-Value (LTV) | 70-80% for investors | This determines the maximum loan amount you can receive based on the appraisal. |

| Credit Score | 680+ | A higher score gets you better interest rates and increases your chance of approval. |

| Appraisal | Based on ARV | The appraisal must support your projected value to make the cash-out refinance successful. |

Your job is to hand the lender—and more importantly, the appraiser—a bulletproof package. Give them a detailed breakdown of every single improvement you made, complete with before-and-after photos and a summary of your rehab costs. This helps them see the value you created with their own eyes, justifying the higher appraisal and making sure you can pull out every last dollar to go find the next deal.

Time to Do It All Again: Scaling Your Portfolio

This final step, "Repeat," is where the magic really happens with the BRRRR method. It's the engine that turns a single successful project into a full-blown rental portfolio. Once you've pulled your cash back out from a refinance, you're armed and ready to hunt for the next deal. This is how you build real momentum.

Let's put some real numbers to it so you can see how this capital recycling plays out.

Say you find a tired-looking property that needs some love. Here's how the initial investment breaks down:

- Purchase Price: $120,000

- Rehab Costs: $30,000

- Holding & Closing Costs: $10,000

- Total Cash Out of Pocket: $160,000

You execute your renovation plan, get a great tenant in place, and the bank sends out an appraiser. The new valuation comes in at a solid $220,000. Your lender, who understands what you're doing, agrees to a cash-out refinance at 75% of this new value.

The math is simple: $220,000 (After Repair Value) x 0.75 (Loan-to-Value) = $165,000.

That new loan of $165,000 completely pays back your $160,000 investment. You even get a check for $5,000 at closing. Now, you own a cash-flowing rental with a built-in equity cushion, and—most importantly—you have all of your original capital back, ready to pounce on the next opportunity. That's the powerful cycle that lets savvy investors grow their holdings exponentially.

From a Single Deal to a Scalable System

Pulling off one BRRRR is a huge win. But doing it five or ten times? That requires a total mindset shift. You have to stop thinking like a project-based investor and start acting like a business owner. Scaling isn't just about finding the cash; it's about building the systems and the team to handle the volume without you burning out.

You simply can't do it all yourself. As you grow, your job changes from doing the work to managing the people who do the work. This means finding your "power team."

Here’s who you need in your corner:

- An Investor-Focused Agent: Not just any agent. You need someone who lives and breathes investment properties and knows how to find the ugly houses before they hit the market.

- Your Go-To Contractor: A reliable, licensed pro you can count on. Once you find someone who delivers quality work on time and on budget, hold onto them for dear life.

- A Savvy Lender: This is critical. You need a loan officer or mortgage broker who gets the BRRRR strategy and won't give you a blank stare when you mention "cash-out refinance."

- A Great Property Manager: You might self-manage your first few, but you need to have a relationship with a good PM. They are your key to scaling beyond what you can handle on your own.

Building these relationships is an investment. Find good people, treat them like partners, pay them on time, and keep them busy. They will become your single greatest asset.

The secret to scaling with BRRRR isn't just hunting for deals; it's building a well-oiled machine. The goal is a repeatable process, powered by a trusted team, that churns out performing rental properties one after another.

Systematize Everything for Smooth Growth

With your team in place, it's time to standardize your operations. You shouldn't be starting from scratch with every property. Checklists, templates, and documented procedures for each stage of the process will save you an incredible amount of time and prevent costly mistakes.

Think about creating standard documents for your core activities:

- Deal Analysis Checklist: A simple, non-negotiable checklist you run through for every potential deal. This ensures you never forget a critical due diligence item.

- Scope of Work Template: Create a master SOW for your ideal rental. List your preferred paint colors, LVP flooring model, standard light fixtures, and so on. This makes getting bids from contractors a breeze.

- Tenant Screening Rules: Write down your criteria—minimum credit score, income-to-rent ratio, background check requirements—and apply them consistently to every single applicant.

- Refinance Package: For each project, create a digital folder where you immediately save the purchase contract, rehab receipts, before-and-after photos, and the signed lease. When the lender asks for documents, you're ready.

These systems become the scaffolding that supports your growing business. They allow you to delegate with confidence and free you up to focus on the highest-value task: finding the next deal.

Using Technology to Keep It All Straight

Managing one or two properties on a spreadsheet is manageable. But at five, ten, or more? It becomes a liability. Trying to track multiple loan balances, rent payments, lease expirations, and maintenance calls manually is a recipe for disaster.

This is where a dedicated platform like Property Scout 360 can be a total game-changer. It helps you graduate from simply analyzing deals to actively managing your entire portfolio. You can see the real-time financial health of every property, watch your equity grow, and spot opportunities for your next strategic move.

Instead of being buried in paperwork, you can see your whole real estate empire on a single dashboard. This frees up your most valuable resource—your time—so you can get back out there and repeat the process that drives real growth.

Common Questions About the BRRRR Method

Even with a detailed guide, diving into your first BRRRR method real estate deal can be nerve-wracking. It’s completely normal to have questions about the risks and how it all works in the real world.

Let's break down some of the most common hurdles and concerns that new investors run into. Knowing what to expect is half the battle.

What Are The Biggest Risks of the BRRRR Method?

This strategy is a powerhouse for building a portfolio, but it's not foolproof. The three biggest things that can trip you up are blowing your renovation budget, getting a low appraisal, and having the property sit vacant for too long.

Any one of these can stall your project and lock up your precious capital. The key is to plan for them.

I never make an offer without getting detailed, written bids from multiple contractors first. I also run my After-Repair Value (ARV) numbers on the conservative side and always bake in a 10-15% contingency fund for surprise costs. Trust me, they always pop up. A healthy cash reserve is your best friend when you're paying the bills on an empty property.

How Much Money Do I Realistically Need to Start?

This answer changes a lot depending on your market, but you should probably have between $50,000 and $100,000 liquid and ready to go. This isn't just for the down payment, which is usually funded with a hard money or private loan anyway.

That initial capital has to stretch a lot further. It needs to cover:

- The entire renovation: Lenders typically expect you to fund the rehab yourself before they'll refinance the property based on its new value.

- Holding costs: Think loan payments, insurance, taxes, and utilities for the whole project timeline. This can easily be six months or more.

- Closing costs (twice): You'll pay them when you buy the property and again when you do the cash-out refinance.

The whole point of the BRRRR method is to recycle your cash, but you can't start the cycle without a decent-sized tank of fuel. Being under-capitalized is probably the fastest way to see a deal go sideways.

What Happens If the Appraisal Comes in Low?

A low appraisal is every BRRRR investor's nightmare. It’s the one thing that can stop you from pulling all of your cash back out of the deal. If the appraiser's number doesn't hit your target ARV, the bank will lend you less money on the refinance.

First off, don't panic. You have options. You can formally challenge the appraisal by providing the appraiser with a list of better comparable sales they might have overlooked. If that’s a dead end, you could simply wait a few months. A little market appreciation might be all you need to try refinancing again with a different lender.

The worst-case scenario? You leave some of your original investment in the property. It stings because it lowers your immediate return on investment, but you still end up with a great, cash-flowing rental property in your portfolio. It just slows down your next deal.

Can I Use an FHA or VA Loan for This?

In short, it's incredibly difficult and I wouldn't recommend it. FHA and VA loans are designed for people who plan to live in the home, not for investors flipping or renting a property. They have really strict standards for the property's condition, and most houses that are good BRRRR candidates wouldn't even come close to qualifying.

Plus, these government-backed loans have rules against doing a large cash-out refinance for investment purposes right after you buy. The BRRRR method real estate strategy is built for commercial-style financing—think hard money loans, private capital, or specific investment property loans. Finding a lender who actually understands your strategy is absolutely critical.

Ready to stop guessing and start analyzing deals with confidence? Property Scout 360 gives you the tools to instantly calculate ARV, project cash flow, and find profitable BRRRR deals in minutes, not hours. See how it works at https://propertyscout360.com.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.