Creative Financing for Real Estate Unlocking Your Next Deal

Discover powerful creative financing for real estate strategies. Learn how seller financing, lease options, and subject-to deals can help you close more deals.

When a bank says "no," most real estate investors think the deal is dead. But that’s where the pros separate themselves from the amateurs. Creative financing is simply about solving problems—it's a way to buy property without running to a traditional lender for a mortgage.

Instead of a one-size-fits-all loan, you use strategies like seller financing or lease options to structure a deal that works for everyone involved. It’s particularly powerful when conventional loans are just out of reach.

Thinking Beyond the Bank: Your Guide to Creative Financing

Ever find a killer deal, only to realize you can't get a bank to fund it? It’s a common frustration, especially when interest rates spike or lenders get picky. This is precisely when creative financing stops being a "backup plan" and becomes your primary competitive edge. It’s not about finding sketchy loopholes; it's about mastering a set of proven tools for situations where a standard approach just won’t cut it.

Think of a conventional mortgage like a standard Phillips-head screwdriver—it works great for most screws, but it’s useless when you encounter something different. Creative financing is the rest of that specialized toolkit. These techniques unlock deals by solving problems for both you and the seller, creating win-win scenarios where a bank would just see a dead end.

What’s the Real Goal of Creative Financing?

At its heart, creative financing is about making a deal happen that otherwise couldn't.

For an investor, it could mean buying a property with very little cash out of pocket, locking in better terms than a bank is offering, or closing in a week instead of waiting the typical 30 to 60 days.

For a seller, it might be the key to selling a tough property quickly, generating a reliable monthly income stream, or avoiding hefty realtor commissions. The common denominator here is flexibility. These aren't rigid, off-the-shelf products; they're custom-built solutions. If you want to see how these stack up against the old-school methods, check out our deep dive on how to finance a rental property.

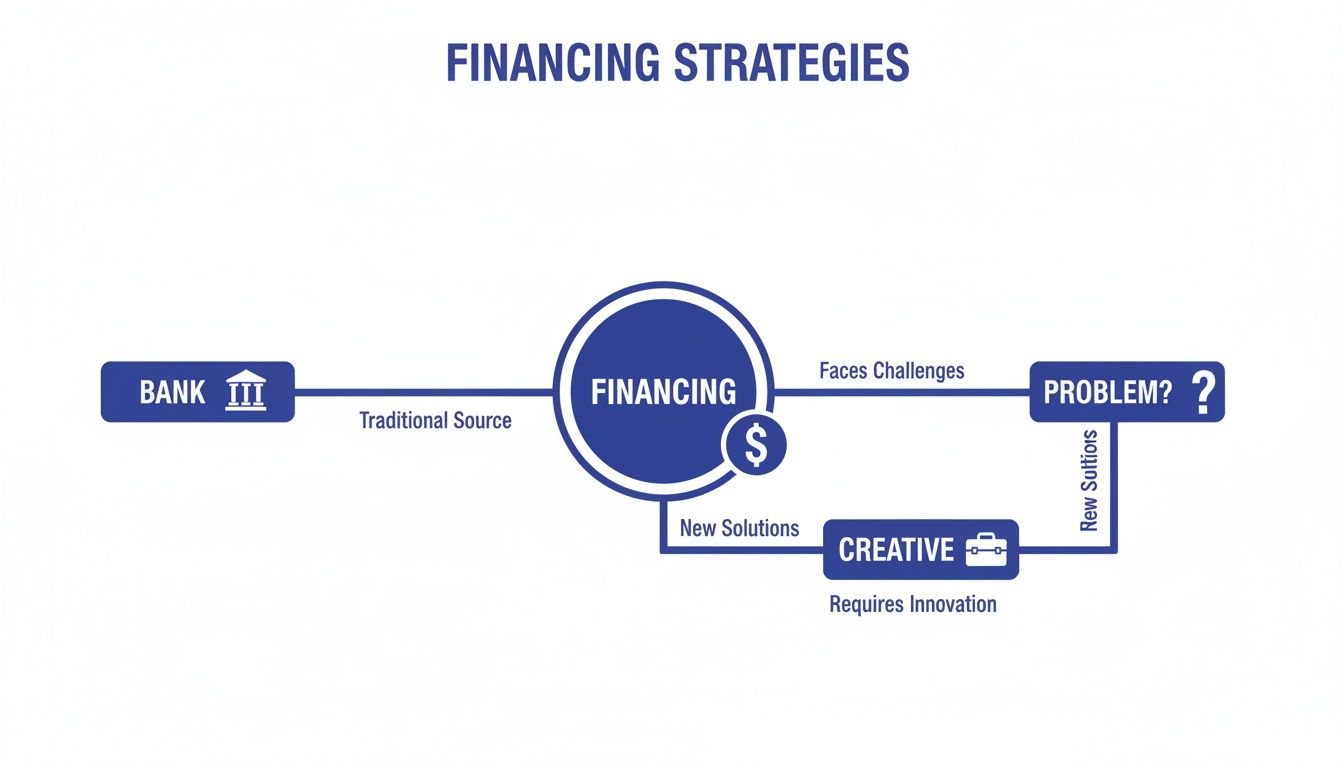

This diagram perfectly illustrates how creative strategies bridge the gap when traditional financing becomes a barrier.

As you can see, the creative "toolbox" is what allows savvy investors to navigate and overcome the most common hurdles in real estate.

To give you a quick overview, here are some of the most common tools in the creative financing toolbox and when you might use them.

Creative Financing Methods at a Glance

| Financing Method | Best For | Key Feature |

|---|---|---|

| Seller Financing | Motivated sellers; buyers with weak credit. | The seller acts as the bank, holding the note on the property. |

| Subject-To | Properties with existing low-interest mortgages. | The buyer takes over the seller's existing mortgage payments. |

| Lease Option | Buyers who need time to secure financing. | The buyer rents the property with the exclusive option to buy later. |

| Hard Money Loan | Short-term financing for fix-and-flips. | Fast funding based on the property's value, not borrower's credit. |

Each of these strategies opens up a new set of possibilities, but they all require a solid understanding of the numbers to work.

Turning Complex Scenarios into Clear Numbers

The biggest hang-up for most investors is getting comfortable with the math behind these deals. How does a seller-financed loan at 5% interest over 20 years really compare to a conventional 30-year mortgage? Guessing is not a strategy. This is where having the right tools becomes non-negotiable for making smart decisions.

Creative financing shifts the power from the lender to the individuals in the transaction. It’s about solving problems and creating value where none existed before.

Modern platforms like Property Scout 360 were built to demystify these complex scenarios. You can plug in different financing structures—seller financing, partnerships, you name it—and see exactly how they impact your bottom line before you even think about making an offer. This isn't just about getting a "yes"; it's about making sure the deal is actually a good one.

Mastering Seller Financing and Subject-To Deals

When the bank says no, some of the best creative financing strategies involve working directly with the property owner. Two of the most powerful tools in this playbook are seller financing and subject-to deals. Both let you sidestep the traditional bank approval process, but they operate in completely different ways.

Getting a handle on these techniques can open up a world of properties that are totally off-limits to investors stuck in a conventional loan mindset. It takes a different kind of negotiation and a keen eye for detail, but the payoff can be massive.

Seller Financing: The Owner Becomes Your Bank

Seller financing (or owner financing) is as straightforward as it sounds. Instead of borrowing from a bank, you borrow directly from the person selling you the house. You make your monthly payments to them, just like you would with a regular mortgage.

It's often a true win-win. As the buyer, you can snag a property with more flexible terms, maybe a smaller down payment, and fewer closing costs. The seller, on the other hand, gets to offload their property—often quicker and at a better price—while creating a steady income stream for themselves from the interest.

Think of it like this: the seller is just converting their home equity into a cash-flowing asset. They’re trading one big check for a reliable, long-term income, which can be incredibly attractive for sellers like retiring landlords or anyone who has owned the property for a long time. To see how the loan agreement is put together, you can learn more about what a seller note is and how it’s structured.

The real magic of seller financing happens at the negotiating table. Everything is up for grabs—the interest rate, the down payment, the length of the loan—giving you a unique chance to build a deal that fits your investment strategy like a glove.

Subject-To Deals: Taking Over an Existing Loan

Now, let’s switch gears to another powerhouse technique: buying a property "subject to" the existing financing. In a subject-to deal, you don't get a new loan at all. Instead, you take title to the property and just start making the payments on the seller's existing mortgage.

The original loan stays in the seller's name, but you're the one in control of the property and responsible for the monthly payments. This is an incredible strategy when interest rates are climbing because it lets you lock in the seller’s much lower rate from years ago.

This can be an absolute game-changer for your cash flow. Imagine taking over a mortgage with a 3% interest rate when current rates are pushing 7%. That difference in the monthly payment is huge and goes straight to your bottom line from day one.

Why on Earth Would a Seller Agree to This?

Sellers who go for subject-to deals are usually in a tight spot. They might be facing foreclosure, needing to move for a new job, or just desperate to get out from under the property without wrecking their credit. When you offer to take over their payments immediately, you become the perfect solution to their biggest problem. But this strategy demands careful homework.

- Verify Loan Details: You have to confirm the exact mortgage balance, interest rate, and payment amount, and make sure the loan is current. No surprises.

- Understand the Due-on-Sale Clause: Most mortgages contain a "due-on-sale" clause, which gives the lender the right to call the entire loan due if the property is sold. While lenders rarely enforce this if the payments keep coming on time, it's a real risk you need to be aware of.

- Ensure Proper Legal Documentation: When executing 'subject to' deals, it's essential to understand the implications of a warranty deed subject to debt to ensure proper transfer of ownership while the existing mortgage remains.

Both seller financing and subject-to deals are about turning someone else's problem into your opportunity. By understanding a seller's motivation and offering a creative solution, you can structure incredible deals and open doors that would otherwise be locked tight.

Using Lease Options and Wraparound Mortgages to Control Property

Beyond just having the seller act as the bank, other creative financing strategies can give you control over a property without a massive cash outlay. Two of the most powerful are lease options and wraparound mortgages. Each one offers a different angle for structuring a deal that works for both you and the seller, especially when a traditional bank loan just isn’t in the cards.

The core idea behind these methods is to control the asset now and formalize the purchase later. They buy you time, give you flexibility, and create a path to ownership that banks simply don't offer.

Test Driving a Property with Lease Options

A lease option, which you’ve probably heard called "rent-to-own," is one of the easiest creative financing concepts to grasp. Think of it as test-driving a car before you commit to buying it. You get to live in the property (or rent it out to a tenant) right away, which gives you valuable time to clean up your credit, save up a bigger down payment, or just wait for the market to shift in your favor before you pull the trigger on the purchase.

The whole strategy is built on three key pieces that fit together to make the deal work. Getting these right is crucial.

- The Lease Agreement: This is your basic rental contract, spelling out the monthly rent and how long the lease lasts. The crucial difference is that it’s directly tied to your right to purchase the property.

- The Option Fee: This is a non-refundable payment you give the seller upfront. What are you buying? The exclusive right to purchase that property at a set price later on. This fee is almost always credited toward your down payment when you decide to buy.

- The Purchase Price: Right from the start, you and the seller agree on a locked-in price. This is a huge advantage for you, as it protects you from rising home values if the market takes off during your lease period.

Here’s a simple example: You find a house valued at $300,000. You negotiate a two-year lease option with $1,500 per month in rent and a $10,000 option fee. The purchase price is locked in at $310,000. For the next two years, you control the property. At any point during that time, you can exercise your option to buy it for $310,000, and your $10,000 option fee gets applied to your down payment.

Structuring Deals with Wraparound Mortgages

A wraparound mortgage is a more advanced form of seller financing where the seller essentially creates a new, larger loan for you that "wraps" around their existing mortgage. Instead of you getting a new loan and paying off the seller's, you make one single payment to the seller. The seller then uses part of that money to pay their original mortgage and pockets the difference.

This is a brilliant strategy when a seller has an old loan with a fantastic low-interest rate. They get to earn a "spread" on the interest rate difference, and you get into a property without having to qualify for a brand-new bank loan.

A wraparound mortgage allows an investor to benefit from the seller's low-interest loan, creating an immediate cash flow arbitrage opportunity that is invisible in traditional transactions.

Let's look at how the numbers work on a "wrap."

| Financial Component | Seller's Existing Loan | Buyer's New "Wrap" Loan |

|---|---|---|

| Loan Balance | $150,000 | $250,000 |

| Interest Rate | 3.5% | 6.0% |

| Monthly P&I | ~$674 | ~$1,500 |

In this scenario, your new payment to the seller is $1,500 a month. The seller turns around and pays their original $674 mortgage payment, leaving them with $826 in positive cash flow every single month. You get the property with $50,000 in seller financing, and the seller creates a brand-new income stream. It’s a slick solution, but it absolutely requires solid legal paperwork to make sure all payments are handled correctly and everyone is protected.

Tapping into Private and Hard Money for Lightning-Fast Capital

When a fantastic deal hits the market, you don't have weeks to wait for a bank to approve your loan. The ability to close fast is a massive advantage, and that's where private capital comes in. For savvy investors, the two most powerful tools for securing quick funding are private money and hard money loans.

While people often use the terms interchangeably, they aren't the same thing. Think of them as two different kinds of financial partners. One is all about relationships, while the other is a pure business transaction focused squarely on the property.

Private Money: The Power of Your Network

Private money is exactly what it sounds like—funding from private individuals. These are people in your personal or professional circle, like friends, family, colleagues, or other investors who want their capital working in real estate without swinging a hammer themselves.

The entire deal is built on relationships. Because of that personal connection, the terms can be incredibly flexible. You might negotiate a lower interest rate, avoid paying points, or create a custom repayment plan that fits your project's timeline. The lender's decision is based on their trust in you, not just a rigid checklist.

Hard Money: Asset-Based Lending for Pure Speed

Hard money comes from professional lending companies that specialize in short-term, asset-backed loans. These lenders couldn't care less about your credit score or debt-to-income ratio. Their one and only focus is the value of the property you're buying.

This makes hard money the fuel for house flippers and investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy. Lenders will often fund the deal based on the property's After Repair Value (ARV). That means they’ll give you the money for the purchase and sometimes even the renovation costs, because they know the finished project will be a solid asset.

The biggest edge you get with private and hard money is speed. To truly make this work for you, it's worth understanding Why Cash Buyers Can Close Faster—it will help you craft offers that sellers can't refuse.

Understanding the Terms and Costs

Of course, this speed and flexibility don't come for free. Both private and hard money loans have higher costs than a conventional mortgage. Here’s what you should expect to see:

- Interest Rates: Be prepared for rates anywhere from 8% to 15%, sometimes even higher, depending on the lender and the deal's risk profile.

- Points: Lenders charge upfront fees called "points," which are a percentage of the loan amount. On a hard money loan, seeing 2 to 5 points is standard.

- Loan Term: These aren't 30-year loans. They are short-term financing, usually for six months to two years, meant to be paid back once you sell the property or refinance into a traditional mortgage.

Right now, the private credit market is booming. Alternative debt sources like private credit now account for 24% of U.S. commercial real estate lending, a huge jump from the 10-year average of just 14%. As traditional banks get more cautious, this shift is opening up more opportunities than ever for investors who need fast, flexible capital. This trend alone shows why getting a handle on creative financing is no longer optional—it's essential.

How to Analyze Creative Financing Deals Like a Pro

Knowing the different creative financing strategies is one thing. Actually closing a deal with confidence? That comes down to running the numbers, and running them right. Theory doesn't pay the bills, but data-driven decisions absolutely build wealth. This is where you graduate from concepts to concrete analysis, turning a potential opportunity into a predictable, profitable asset.

Guesswork is the single biggest enemy of a successful real estate investor. You have to be able to model different scenarios, compare outcomes side-by-side, and see exactly how a creative structure will affect your cash flow and long-term returns. This whole process isn't about spreadsheets; it's about removing emotion and replacing it with clarity, so you can negotiate from a position of undeniable strength.

Modeling Your First Creative Deal Step-by-Step

Let's walk through a real-world scenario to see how this plays out.

Imagine you've found a motivated seller with a duplex listed for $350,000. They've owned it for years, are tired of being a landlord, and are surprisingly open to seller financing to create a steady income stream for themselves.

Here are the terms they've proposed:

- Down Payment: 10% ($35,000)

- Interest Rate: 5.5% (a whole lot better than current bank rates)

- Amortization Period: 30 years

- Loan Term: A 7-year balloon payment

Instead of wrestling with a clunky spreadsheet, you can plug this entire scenario into a tool like Property Scout 360 in just a few minutes. The platform is built to handle these custom loan terms, letting you input the seller's proposal directly to see the financial impact instantly.

The ability to quickly model custom financing is what separates professional investors from amateurs. It allows you to evaluate opportunities that others can't even begin to analyze, giving you a significant competitive advantage.

Once you enter the seller-financed terms, the software immediately crunches the numbers and gives you the vital signs of the deal's health. You’ll see your projected monthly cash flow, your cash-on-cash return, and your long-term ROI—all based on this specific creative structure. This is the essential first step in any real analysis. If you're new to this, you can learn more about the fundamentals in our guide on how to analyze any real estate investment.

Comparing Creative vs. Conventional Financing

Now for the fun part. The real power comes from comparing this creative scenario against a traditional bank loan. With just a few more clicks in Property Scout 360, you can run a parallel analysis using a conventional 30-year mortgage with a 20% down payment and the current market interest rate of, say, 7.25%.

The difference becomes crystal clear, fast.

The seller-financed deal not only requires less cash out of your pocket ($35,000 vs. $70,000) but also gives you a lower monthly payment thanks to that sweet interest rate. That difference flows directly into your bank account as higher monthly cash flow, juicing your immediate returns and making the property perform better from day one.

Side-by-Side Comparison:

| Metric | Seller Financing (5.5% Rate) | Conventional Loan (7.25% Rate) |

|---|---|---|

| Down Payment | $35,000 | $70,000 |

| Monthly P&I | ~$1,788 | ~$1,900 |

| Projected Cash Flow | +$412/month | +$200/month |

| Cash-on-Cash Return | 14.1% | 3.4% |

This data-driven comparison removes every bit of guesswork. You can clearly see that the creative financing option more than quadruples your initial cash-on-cash return, turning a decent deal into an absolute home run. This is how you turn complex "what-if" questions into a simple, data-backed decision that gives you the confidence to pull the trigger.

The broader financial landscape is also shifting to favor these kinds of strategies. Private credit's massive growth is reshaping real estate, with global project finance lending expected to shatter records at over $500 billion in 2025, while North American volumes have already soared 41% year-over-year. This shift is happening as traditional equity gets tight, but debt is still flowing. For smart investors, this means learning how to blend private credit with other loan types in tools like Property Scout 360 is essential for creating truly accurate ROI forecasts. You can get more insights on this capital cost outlook on projectfinance.law.

Managing Risks in Non-Traditional Real Estate Deals

Creative financing can unlock doors that conventional loans keep shut, but let's be clear: it comes with its own set of risks. These aren't the kind you'll find in a standard bank deal, and overlooking them can turn a brilliant opportunity into a costly mess.

The trick isn't to run from these strategies, but to walk in with your eyes wide open and a solid plan to manage the risks.

Think of it like this: a traditional mortgage has guardrails already built in by the lender. When you're the one structuring the deal, you have to build those guardrails yourself. That means your due diligence needs to be flawless and your legal agreements have to be airtight. This isn't just a recommendation; it's your financial lifeline.

Every single non-traditional agreement—whether it’s a seller-financed note, a "subject-to" purchase, or a lease option—needs to be drawn up by a real estate attorney who gets this stuff. Trust me, a generic template you find online is a lawsuit waiting to happen. A good attorney makes sure every detail is crystal clear, legally binding, and actually protects you.

Navigating the Due-on-Sale Clause

One of the biggest boogeymen in creative financing, especially with "subject-to" deals, is the due-on-sale clause. This is a standard piece of language in most mortgage contracts that gives the original lender the right (but not the requirement) to call the entire loan due if the property changes hands.

Now, in practice, lenders rarely trigger this clause as long as the mortgage payments keep coming in like clockwork. But the risk is never zero. If the bank decides to accelerate the loan, you’d be on the hook to pay it off immediately or face foreclosure.

Your best defense is a bulletproof exit plan from day one. That might mean having enough cash on hand to pay off the loan or being in a position to quickly refinance the property into your own name if the lender ever makes that call.

An Essential Risk Management Checklist

Beyond the due-on-sale clause, a smart investor's risk management plan covers several other bases. Before you even think about closing a creative deal, make sure you can tick off these boxes:

- Professional Legal Review: I can't say this enough. Get a real estate attorney who specializes in creative financing to either draft or review all documents. This is the single most important thing you will do.

- Clear Title and Insurance: Always, always get a title search and buy a title insurance policy. This protects you from nasty surprises like old liens or someone else claiming they own the property.

- Transparent Tax Implications: You need to understand the tax situation for both you and the seller. A quick chat with a tax professional can prevent huge headaches for everyone involved later on.

- Third-Party Servicing: For any deal involving seller financing, think about using a third-party loan servicing company. They act as a neutral middleman, collecting payments and keeping perfect records. It keeps things professional and prevents any "he said, she said" disputes.

By taking these steps, you can confidently use these powerful strategies to grow your portfolio, knowing your assets are protected and your deals are built to last.

Your Top Creative Financing Questions, Answered

Diving into the world of creative real estate financing can feel like learning a new language, and it's natural to have questions. Let's tackle some of the most common ones that come up when investors start moving beyond traditional bank loans.

Is This Stuff Just for People With Bad Credit?

Not at all. That's one of the biggest misconceptions out there. While it's true some creative techniques can be a lifeline for buyers with credit hurdles, seasoned investors with stellar credit use these strategies all the time to get a leg up.

Think about it: why wouldn't you use seller financing if it meant snagging a lower interest rate than the bank was offering? Or why wouldn't you take over a loan "subject-to" if it meant inheriting an incredible 2.75% interest rate from a few years ago? The real power of creative financing is in its flexibility—it’s about engineering the best possible deal for a specific property and situation, regardless of your credit score.

What’s the Catch With "Subject-To" Deals?

The main thing you have to watch out for is the "due-on-sale" clause. This is a standard piece of language in nearly every mortgage agreement that gives the seller's original lender the right to call the entire loan due the moment the property changes hands.

While lenders don't always pull this trigger—they're often happy as long as the payments keep coming in on time—the risk is never zero. You absolutely must have a backup plan, like being able to refinance the property into your own name, just in case the lender decides to enforce the clause.

How Do I Even Find Sellers Open to These Ideas?

You're looking for one thing: motivation. A seller who needs to close fast, is tired of being a landlord, or has a property that's been sitting on the market for months is far more likely to listen than someone with multiple cash offers.

Here are the people and situations to look for:

- Owners who have paid off their mortgage completely (free-and-clear).

- For Sale By Owner (FSBO) listings, since these sellers are already bypassing the traditional system.

- Properties that have been stale on the market for a long time.

- Retiring landlords who might actually prefer a reliable monthly check over a massive tax bill from a lump-sum payment.

The trick is to stop talking and start listening. Ask what the seller truly wants to achieve with the sale. If their goal is a steady, predictable income stream, you’ve likely found the perfect candidate for a creative deal.

Ready to stop guessing and start analyzing deals with confidence? Property Scout 360 allows you to model complex creative financing scenarios in minutes, comparing them side-by-side with traditional loans to find the most profitable path forward. Discover how Property Scout 360 can transform your investing strategy today.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.