What Is GRM in Real Estate Your Guide to Smart Investing

Learn what is GRM in real estate and how this simple metric helps you find profitable rental properties and make smarter investment decisions.

When you're sifting through potential real estate deals, you need a quick way to gauge if a property is even worth a closer look. That's where the Gross Rent Multiplier (GRM) comes in. It's a straightforward calculation that gives you a rough idea of how a property's price stacks up against the income it generates.

Think of it as a back-of-the-napkin test. In essence, the GRM tells you how many years it would take for the property's gross rent to pay for itself.

What Is the Gross Rent Multiplier in Real Estate

Imagine you're at the grocery store comparing two bags of apples. One is cheaper, but the other has more apples. To figure out the better deal, you’d probably check the price per pound. GRM works the same way for rental properties—it gives you a simple, standardized number to compare different investments, even if their prices and rents vary wildly.

It’s designed to be a first-pass filter. By focusing only on the purchase price and the total annual rent, GRM intentionally ignores the nitty-gritty details like property taxes, insurance, and maintenance costs. This simplicity is its biggest strength, allowing you to quickly spot properties that might be underpriced for their rental potential.

Understanding the Core Concept

At its heart, the GRM is all about the relationship between a property's price tag and its raw income-producing power. It's not a profitability metric, so it won't tell you how much cash you'll pocket each month. Instead, it’s a valuation tool.

Generally speaking, a lower GRM is better. It suggests you're paying less for every dollar of rent the property brings in, which could signal a more attractive investment opportunity.

The Simple GRM Formula

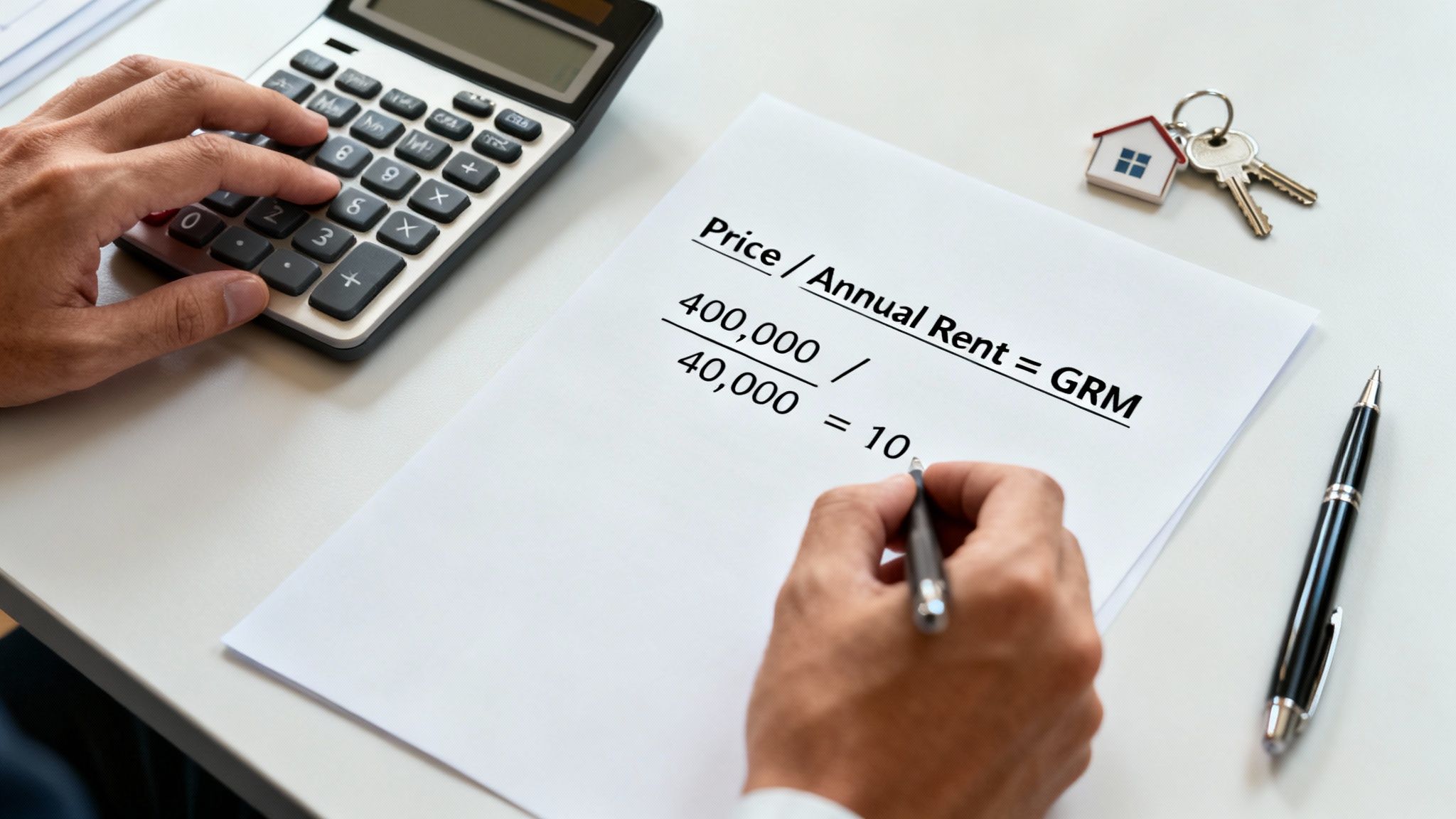

GRM = Property Price / Gross Annual Rental Income

This formula spits out a single, easy-to-digest number. Let's say you're a new investor looking at a duplex priced at $400,000 that brings in $40,000 in rent per year. Your GRM would be 10 ($400,000 / $40,000).

This means it would take 10 years of collecting the gross rent to equal the purchase price. When you're staring at a list of 20 different properties, being able to do this quick math helps you zero in on the one or two that truly deserve your time and deeper analysis. You can learn more about the fundamentals of GRM to build on this foundational concept.

It helps answer that all-important initial question: "For the rent this place can generate, is the price in the right ballpark?"

To help you get comfortable with the concept, here's a quick summary of what GRM is all about.

GRM At a Glance Key Concepts

| Aspect | Description | Why It Matters |

|---|---|---|

| What It Is | A valuation metric comparing property price to gross annual rent. | It provides a quick, standardized way to compare different rental properties. |

| The Goal | To quickly assess if a property's price is reasonable relative to its income. | Helps investors filter deals efficiently without getting bogged down in details. |

| Ideal Value | A lower GRM is generally considered more favorable. | Suggests a shorter payback period and potentially a better value investment. |

| Key Limitation | It ignores all operating expenses (taxes, insurance, repairs). | It is not a measure of profitability or cash flow, only a valuation shortcut. |

This table should give you a solid foundation. Remember, GRM is the starting line for your analysis, not the finish line.

A Step-by-Step Guide to Calculating GRM

One of the best things about the Gross Rent Multiplier is its beautiful simplicity. You don't need to fire up a complicated spreadsheet or have a degree in finance to get a quick read on a property. All it takes is two key pieces of information.

Let's walk through the process together. I find the best way to learn is with a real-world example, so let’s start with a classic investment: a single-family home.

The Single-Family Home Example

Picture this: you've found a single-family home for sale and you want to see if the price makes sense. Here’s how you’d calculate its GRM in two quick steps.

Gather Your Two Key Numbers

- Property Price: This is simply the asking price. Let's say the house is listed at $400,000.

- Gross Annual Rent: This is the total rent you'd collect in a year, before touching a single expense. If the property rents for $3,333 per month, you'll need the annual figure.

Do the Math

- First, get your annual rent: $3,333/month x 12 months = $40,000.

- Now, use the GRM formula: GRM = Property Price / Gross Annual Rent.

- Let's plug in our numbers: $400,000 / $40,000 = 10.

That’s it. The GRM for this home is 10. In simple terms, this means it would take ten years of gross rent to pay back the purchase price. Now you have a solid number you can use as a benchmark.

Applying GRM to a Duplex

The same logic works perfectly for small multi-family properties. The only real difference is adding up the rent from all the units. For a deeper dive into how rent and price play off each other, our guide on how to calculate rental property value is a great next step.

Let's run the numbers on a duplex with a purchase price of $550,000.

- Unit A brings in $2,200/month.

- Unit B brings in $2,300/month.

First, find your total monthly rent: $2,200 + $2,300 = $4,500.

Next, get the Gross Annual Rent: $4,500 x 12 = $54,000.

Finally, calculate the GRM: $550,000 / $54,000 = 10.18.

The duplex has a GRM of 10.18. Notice how close that is to the single-family home’s GRM of 10? This tells you that, relative to their gross incomes, their valuations are in the same ballpark.

Once you get the hang of this, you can screen dozens of potential deals in an afternoon, quickly pinpointing the ones that deserve a much closer look.

How to Make Sense of a GRM Number

Alright, you've calculated the GRM for a property. Now what? Getting the number is the easy part; knowing what it means is where smart investing begins.

A GRM of 10, for instance, isn't inherently good or bad. Its real value comes from comparison. Think of it like a single data point on a chart—pretty useless on its own. You need to see how it stacks up against the surrounding data to understand the story.

The basic principle is straightforward: a lower GRM is generally better. It means you're paying less for every dollar of gross rental income, which suggests you could recoup your investment faster. But here's the catch: what's considered "low" is completely dependent on the market. You have to compare apples to apples. A property's GRM only tells you something useful when you measure it against the average for similar properties in that specific neighborhood.

Why GRM Is All About Location, Location, Location

A property’s address is the biggest driver of its GRM. The local economy, housing demand, and job growth create wildly different investment environments from one city to the next.

Let's look at two classic examples:

- Scenario A: The Stable Midwest Town. You find a duplex with a GRM of 8. In a market with steady, predictable growth, this could be a fantastic find. It points to solid cash flow relative to the purchase price.

- Scenario B: The Booming Coastal City. You're looking at a similar duplex, but the GRM is 18. In a hot market like San Francisco or New York, this is common. Investors are willing to pay a premium because they're banking on significant appreciation, which naturally pushes GRMs sky-high.

This is exactly why you can't take a GRM benchmark from one market and apply it to another. If you did, you might pass on a great deal in a high-GRM city or, even worse, drastically overpay for a property in an area where much lower GRMs are standard.

Finding a Reliable GRM Benchmark

So, what is a good GRM for a rental property? The gold standard is always to pull recent sales data for comparable local properties. But if you're just starting your research, some general rules of thumb can help frame your expectations.

An analysis from J.P. Morgan suggests that for residential rentals, a GRM between 8 and 12 is a common range. Anything under 8 could signal a strong potential buy, particularly in growing suburban areas. Looking back at historical data, even when other metrics were all over the place, GRMs in stable markets have consistently hovered around 10-12. For a deeper dive, you can explore the full real estate analysis from J.P. Morgan.

The Bottom Line: Never look at a GRM in isolation. Always benchmark it against the local average for the same property type and condition. That’s how you spot a genuine opportunity and avoid a potential money pit.

Understanding GRM vs Cap Rate

When you're sizing up an investment property, two metrics will constantly pop up: Gross Rent Multiplier (GRM) and Capitalization Rate (Cap Rate). New investors often get these two confused, but they tell completely different stories about a property's potential.

Think of it like this: GRM is the first-glance impression, while Cap Rate is the deep-dive investigation.

GRM is your initial screening tool. It’s a fast, back-of-the-napkin calculation that answers a simple question: "How many years would it take for the gross rent to pay for the property?" It’s perfect for quickly sifting through a long list of potential deals because it intentionally ignores the nitty-gritty details of operating costs.

The Cap Rate, on the other hand, is where you get serious. It uses a property’s Net Operating Income (NOI)—the income left after you’ve paid for all the operating expenses like taxes, insurance, and maintenance. This makes it a far more accurate gauge of a property's actual, real-world profitability.

To use another analogy, GRM is like checking a car's sticker price. Cap Rate is like calculating its total cost of ownership, factoring in fuel, insurance, and repairs. Both are useful, but you wouldn't buy a car based on the sticker price alone.

The Core Difference: Expenses

The bright, unmissable line between GRM and Cap Rate is how they handle operating expenses. It's a simple but profound distinction.

- GRM is calculated using Gross Annual Income. It completely ignores expenses.

- Cap Rate is calculated using Net Operating Income (NOI), which is gross income minus all operating expenses.

This is also GRM's biggest weakness. Critics rightly point out that ignoring expenses—which can easily eat up 30-40% of gross income—gives you an incomplete picture. But its power lies in speed. A 2023 Nareit analysis revealed that 68% of top-performing REITs targeted properties with a GRM under 10, which helped them secure an average total return of 10.2%. This shows just how effective GRM is as a first-pass filter.

For a more detailed look at how NOI is calculated and why it's so important, check out our complete guide on what the cap rate is in real estate.

When To Use Each Metric

Knowing which tool to pull out of your toolbox—and when—is what separates seasoned investors from rookies. GRM and Cap Rate aren't rivals; they're partners in your deal analysis process. You just need to use them at the right stage.

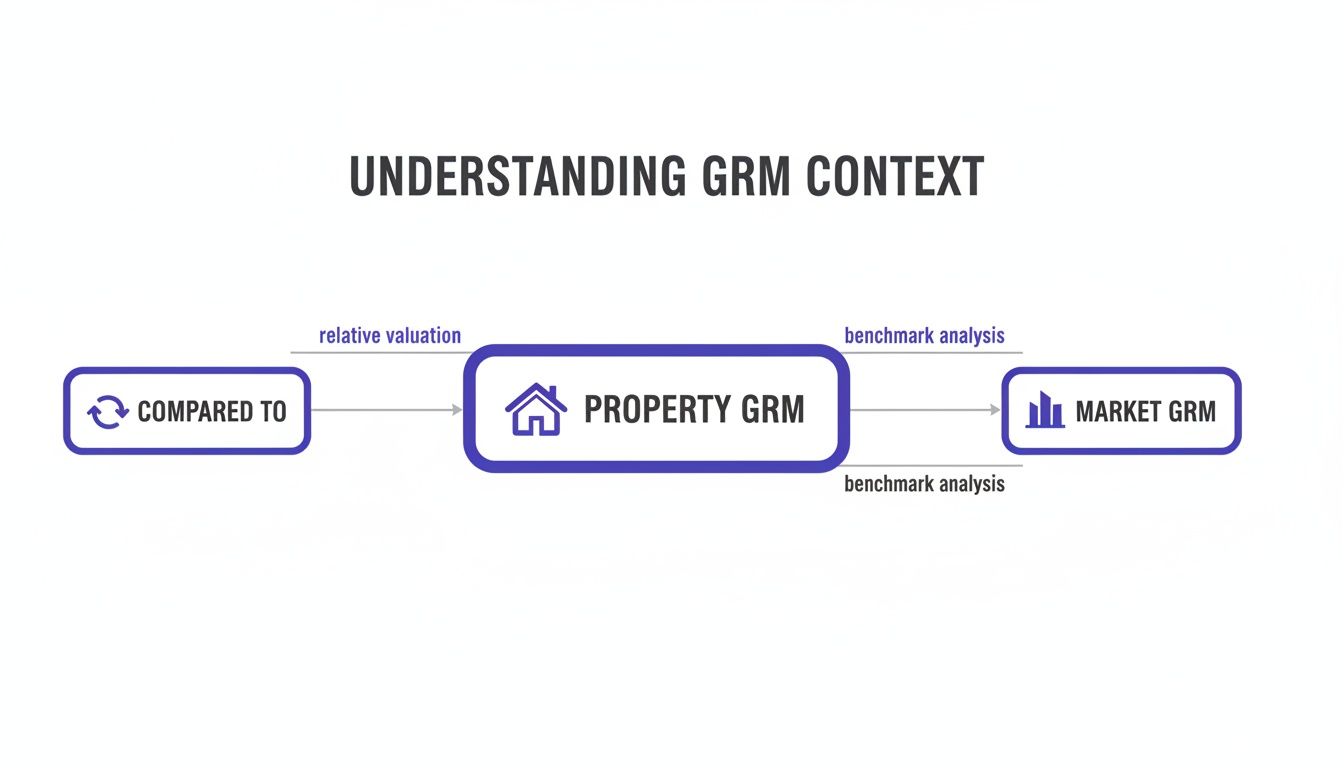

GRM is for broad strokes. It helps you compare a property against the rest of the market to see if it's even in the right ballpark, as this chart illustrates.

As you can see, a GRM figure is meaningless in a vacuum. Its value comes from comparing it to the local market average to spot potential outliers.

To help clarify the roles of these two key metrics, here’s a simple side-by-side comparison.

GRM vs Cap Rate a Head to Head Comparison

| Metric | Formula | Measures | Best For |

|---|---|---|---|

| GRM | Property Price / Gross Annual Rent | The relationship between price and gross income. | Quickly screening many properties in a similar market. |

| Cap Rate | Net Operating Income / Property Price | The unleveraged rate of return, or profitability. | Detailed analysis of a smaller list of serious contenders. |

Ultimately, the workflow is straightforward.

Key Takeaway: Start with GRM to quickly filter a large pool of properties and create your shortlist. Then, switch to Cap Rate and detailed expense analysis to zero in on the deals that are truly profitable.

Common Pitfalls of Relying on GRM Alone

While the Gross Rent Multiplier is a fantastic tool for quickly sorting through potential deals, treating it as the final word on an investment is a classic rookie mistake. Its greatest strength—its simplicity—is also its biggest blind spot. If you don't understand its limitations, you could end up making a costly decision based on an incomplete story.

The most glaring pitfall is that GRM completely ignores operating expenses. It's a top-line metric only, meaning it's blind to all the costs that can eat away at your profit and turn a promising property into a financial nightmare. This oversight can be absolutely devastating to your bottom line.

The Tale of Two Duplexes

Let's walk through a real-world scenario. Imagine two duplexes for sale on the same street, both priced at $500,000. Each property brings in $50,000 in gross annual rent, giving them both an identical—and seemingly attractive—GRM of 10. On the surface, they look like equally good deals.

But once you peek under the hood, the reality is starkly different:

- Duplex A is a cash cow. It's newer, has low property taxes, and features energy-efficient systems that keep annual operating expenses down to a manageable $15,000.

- Duplex B is a money pit. It’s an older building with a leaky roof, an ancient HVAC system, and happens to be in a district with sky-high property taxes. Its annual expenses total a staggering $35,000.

Even with the exact same GRM, Duplex A nets a healthy $35,000 per year. Duplex B? It only clears $15,000. One is a solid investment, while the other is barely worth the headache. This is exactly why GRM should only be your starting point. For the full picture, you have to run a complete rental property cash flow analysis to see where every dollar is actually going.

Other Traps to Watch Out For

Besides overlooking expenses, investors often stumble into a few other common traps when using GRM. Being aware of these can save you from misjudging a deal's true potential.

A big one is relying on unrealistic pro forma rents. Sellers often advertise a property based on its potential rent, not what it’s currently earning. Always, always verify the income with actual lease agreements. Don't let optimistic projections lead you to overpay.

Key Insight: A low GRM is only a good thing if it's based on real, verifiable income and the property's expenses are reasonable for the market. A fantastic GRM can easily hide a terrible investment.

Finally, failing to compare apples to apples will lead you astray. A GRM of 9 might sound great in isolation, but what if you discover that the local average for that specific property type is actually 7? Context is everything. Without it, the number is just a number.

Putting the Gross Rent Multiplier to Work for You

Alright, let's move from theory to action. It's one thing to know what the Gross Rent Multiplier is, but it's another thing entirely to use it to consistently find great deals. Think of the GRM as your high-speed filter—a tool that lets you sift through dozens, even hundreds, of listings to quickly flag the properties actually worth a closer look.

This simple step saves you an unbelievable amount of time. Instead of getting bogged down in detailed spreadsheets for every single property, you can instantly weed out the ones that are clearly overpriced. It's how you go from just browsing to seriously evaluating the right opportunities.

Set Your Own GRM Benchmark

The smartest way to start is by creating a personal rule of thumb. This isn't complicated; it's just a simple guideline that acts as the first hurdle any potential deal must clear. It’s your gatekeeper, making sure you only spend your valuable time on the most promising properties.

Here’s a simple way to build your rule:

- What’s your focus? Are you hunting for duplexes, single-family homes, or small apartment buildings?

- Where are you looking? Get specific. Name the city or even the neighborhood.

- What’s your number? Based on what you know about that market, pick a maximum GRM you're willing to accept.

For example, your personal benchmark might be something like: "I will only do a deep-dive analysis on duplexes in my target city with a GRM of 9 or less."

Having a clear, non-negotiable standard like this brings incredible focus and discipline to your search. For a more comprehensive guide to real estate investing and how metrics like GRM fit into a larger evaluation process, this article is a great resource.

Investor Takeaway: Using GRM as your first-pass filter is all about working smarter, not harder. It’s not the final word on a deal, but it’s the powerful first step that separates the real contenders from the pretenders, ensuring you save your energy for the deals that truly deserve it.

Once you have a shortlist of properties that pass your GRM test, then it's time to roll up your sleeves. From there, you can dig into the more detailed metrics we've talked about, like Cap Rate and cash-on-cash return, to really figure out if you've got a winner on your hands.

Frequently Asked Questions About GRM

Even after you've got the basics down, a few common questions about the Gross Rent Multiplier always seem to pop up. Let's tackle some of those lingering queries so you can use this metric with complete confidence.

Can GRM Be Used for Commercial Properties?

Technically, yes, but it's really not the right tool for the job. You could calculate a GRM for an office building or a retail strip, but seasoned commercial investors almost always lean on the Cap Rate instead.

The reason is simple: operating expenses in commercial real estate are all over the map. Think about the massive difference in expense structures between a triple net (NNN) lease, where the tenant pays for everything, and a gross lease. GRM's biggest blind spot—the fact that it ignores expenses—makes it unreliable for these more complex deals.

For residential properties up to four units, however, GRM is still a go-to screening tool.

Does a Negative GRM Exist?

Nope. In the real world, a negative GRM is impossible. The formula is just the property price divided by the gross annual rent, and both of those numbers have to be positive.

If a property had zero rental income, you wouldn't get a negative number; the formula would be undefined. It would just tell you what you already know: the property isn't producing income, so GRM isn't the right way to evaluate it.

A "good" GRM is highly subjective and varies by market, property type, and your specific investment strategy. Generally, a lower GRM suggests the property generates more income relative to its price, but always compare it to local averages.

How Does Financing Affect GRM?

It doesn't. At all. The GRM calculation is based on an all-cash purchase scenario, focusing purely on the relationship between the property's price and its potential income.

It completely ignores things like your down payment, interest rate, and mortgage payments. To see how your loan terms impact your actual profit, you'd turn to other metrics like Cash-on-Cash Return. Understanding how to use GRM is just one piece of the puzzle, which includes broader strategies to boost your investment's ROI.

Ready to stop guessing and start making data-driven investment decisions? Property Scout 360 eliminates the guesswork by providing instant calculations for GRM, Cap Rate, cash flow, and long-term ROI on any U.S. property. Find and analyze your next profitable rental in minutes, not weeks. Discover how Property Scout 360 can help you build your portfolio today.

About the Author

Related Articles

2026 Investor's Guide: Cost of Installing a Sewer Clean Out

Understand the cost of installing a sewer clean out for investment properties in 2026. Get expert advice on prices, ROI, & budgeting for flips. Plan smart!

15 Year vs 30 Year Mortgage: The Investor's Choice

Deciding between a 15 year vs 30 year mortgage for a rental property? Our guide analyzes cash flow, ROI, and equity to help you pick the best loan.

Real Estate Appraisal Software: Features & Limits

Discover what real estate appraisal software is, its core features, and limits. See how it differs from investment tools for profitable deals.